Ocado Group plc – Annual report – 3 December 2023

Industry: retail; distribution

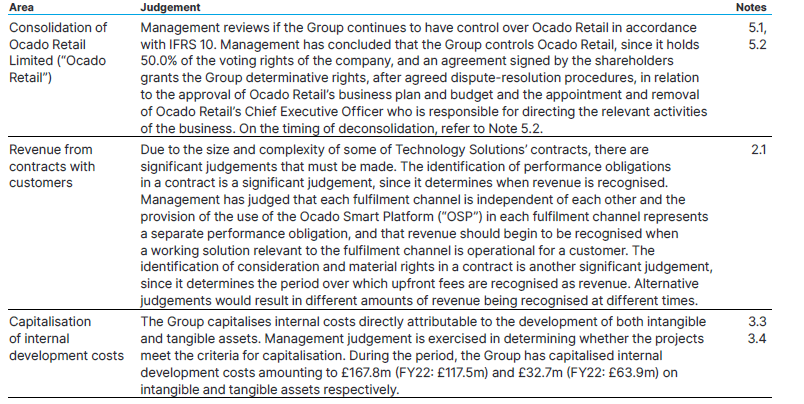

1.4 Critical accounting judgements and key sources of estimation uncertainty

The preparation of the Group’s financial statements requires the use of certain judgements, estimates and assumptions that affect the reported amounts of assets, liabilities, income and expenses. Judgements and estimates are evaluated regularly, and represent management’s best estimates based on historical experience and other factors, including expectations of future events that are believed to be reasonable under the circumstances. However, events or actions may mean that actual results ultimately differ from those estimates, and the differences may be material.

Critical accounting judgements

Critical accounting judgements are those that the Group has made in the process of applying the Group’s accounting policies and that have the most significant effect on the amounts recognised in the financial statements.

Key estimation uncertainties

Key areas of estimation uncertainty are the key assumptions concerning the future and other data points at the reporting date that may have a significant risk of causing a material adjustment to the carrying amounts of assets and liabilities within the next period.

Section 2 – Results for the period (extract)

2.1 Revenue

Accounting policies

Revenue represents the transaction prices to which the Group expects to be entitled in return for delivering goods or services to its customers. The amount of revenue recognised in any period is based on a judgement of when the customer is able to benefit from the goods or services provided, and an assessment of the progress made towards completely satisfying each performance obligation. The following provides information about the nature and timing of the satisfaction of performance obligations in contracts with customers and the related revenue recognition policies for each of the by reportable segments. For information about reportable segments, see Note 2.2.

Retail segment

Revenue from online grocery orders

Revenue from online grocery orders is recognised at a point in time when the customer obtains control of the goods. For deliveries performed by the Group this usually occurs when the goods are delivered to and have been accepted at the customer’s home. For goods that are delivered by third-party couriers, revenue is recognised when the items have been transferred to the third party for onward delivery to the customer. In both instances, there is a single performance obligation, which is the delivery of goods, and the total transaction price is allocated to the performance obligation.

Revenue from online grocery orders is presented net of returns, relevant marketing vouchers and offers, and value added taxes. Relevant vouchers and offers include money-off coupons, conditional spend vouchers and offers such as buy three for the price of two. At the end of each reporting period, management reviews and adjusts the transaction price for elements of variable consideration such as expected refunds or expected voucher redemptions.

Revenue from Ocado Smart Pass

Ocado Smart Pass, the Group’s discounted pre-pay membership scheme, is a separate contract with a customer and has a separate single performance obligation which is to provide delivery services for an agreed period of time. The Group applies the practical expedient allowed under IFRS 15 “Revenue from Contracts with Customers” to apply the standard requirements to a portfolio of contracts, rather than individual contracts, as it believes the characteristics of each sale are similar, and that doing so does not materially affect the financial statements.

Revenue from Ocado Smart Pass is recognised over the duration of the membership on a time-elapsed, straight-line basis.

Logistics segment

Revenues in the Logistics segment relate to the operation of automated warehouses and provision of associated supply chain and delivery services to our UK Partners, Wm Morrison Supermarkets Limited (“Morrisons”) and Ocado Retail.

Revenue is earned from cost recharges, which are the recharge of variable and fixed costs incurred to provide fulfilment and delivery services. Additionally, a management fee is earned on the rechargeable costs. The business also generates revenue from capital recharges relating to certain material handling equipment (“MHE”) assets used to provide logistics services to Ocado Retail which are eliminated on consolidation of the Group.

There is a single performance obligation, which is the provision of fulfilment and delivery services, and the total transaction price is allocated to the performance obligation.

Revenue is recognised as the services are provided to the UK Partners.

Technology Solutions segment

Revenues in the Technology Solutions segment relate to provision of the Ocado Smart Platform (“OSP”) as a managed service to the Group’s grocery retail Partners.

Identification of performance obligations

Each contract is considered on a case-by-case basis. A typical Ocado Solutions contract has a single performance obligation: “to enable the client to access the Ocado Smart Platform (“OSP”) end-to-end online grocery platform from the go-live date, with an agreed physical capacity, from a CFC for example, for the use of its retail brands”. The ability to derive independent benefit is a key determinant. For example, there are several critical contractual milestones that occur before the service is operational, such as the design of the CFC for the customer or preparation of the OSP. However, management has concluded that the customer is not able to derive any benefit from these individual elements until the service is operational and they are able to fulfil an order. Depending on the individual customer, fulfilment of an order may include the delivery of goods to the final consumer, and this would make up part of the obligation.

Consequently, designing the CFC or building the customer OSP is not a separate performance obligation and no revenue can be assigned to satisfying these aspects of the contract. Some contracts, however, have multiple components, for example the addition of in-store fulfilment (“ISF”) services or additional CFCs, which lead to additional distinct performance obligations. In these situations, management uses its judgement to determine whether there are separable performance obligations from which the customer is able to benefit independently.

Determining transaction prices

At the inception of a contract, the total transaction price is estimated, being the amount to which the Group expects to be entitled over the expected duration of the contract, based on the rights it has under the present contract. Such expected amounts are only included to the extent that it is highly probable that no revenue reversal will occur.

Typically, contracts include both upfront fees, paid by the customer in the period prior to the solution going live, and subsequent annual amounts that are either recurring or variable. The upfront fees are one-off payments and are included in the transaction price and recognised over the expected customer life.

Expected customer life is a key judgement as it affects the amount of deferred upfront fees that are released as revenue each period, and the factors considered in reaching the judgement on expected customer life include the nature of the performance obligation, the scale of current and future planned investment, performance against contractual service-level agreements (“SLAs”), the evolving technology and competitive landscape. The judgements made for contract duration may be different to those judgements for expected customer life.

Variable amounts are annual fees whereby typically the variability relates to the volume of sales transactions processed or variable costs associated with providing the service to the customer. It has been determined that these variable amounts should be recognised in the period in which they arise, because they relate to the services provided in that period.

Taken together, it is considered that the above approach represents a suitably conservative view of future estimated revenue in the disclosures of unsatisfied performance obligations as required by IFRS 15.

For each contract an assessment has been made by the Group as to whether there is a significant finance benefit arising from the timing of payments required from the customer. Judgement is required to choose an appropriate interest rate used in the assessment and to set a reasonable threshold for determining whether any finance benefit is significant.

Allocation of transaction prices to performance obligations

Single component contracts have a single performance obligation and the whole transaction price is assigned to that single deliverable. Multiple component contracts will have more than one obligation, each with its own contract duration as adjudged by management. Each contract clearly states the fees relating to each component. This provides management with a basis for allocation of the calculated transaction price to each performance obligation based on the standalone selling price.

Revenue recognition

For each performance obligation and its allocated transaction price, revenue is recognised from the point at which the customer starts to benefit from the services, and over the period the services are provided.

The nature of the services provided, that is the ability to fulfil online grocery orders, represents equal value to the customer every day that the service is provided. This uniformity of value to the customer over time has led the Group to decide that the most appropriate way of measuring the satisfaction of obligations is by using a straight-line, time-elapsed basis. IFRS 15 defines this as an “output method”, which recognises revenue by reference to the value to the customer.

Judgement is applied in relation to contract and customer lives, as typically contracts have no end date. Depending on the expected customer life, the amount and timing of revenue recognised may be different in different accounting periods. As the Solutions contracts with the international Partners are in the early stages of operation, the Directors have limited relevant historical information on which to base their assumptions on expected customer life. Therefore, in making their judgements, the Directors have considered qualitative and quantitative reasonable and supportable information such as market evidence and certain clauses contained within Solutions contracts.

Contract modifications

The Group’s contracts may be amended for changes to specifications and requirements. Contract modifications exist when the amendment creates new, or changes existing, enforceable rights and obligations. The effect of a contract modification on the transaction price and the Group’s measure of progress for the performance obligation to which it relates is recognised as an adjustment to revenue in one of the following ways:

a. Prospectively as an additional separate contract.

b. Prospectively as a termination of the existing contract and creation of a new contract.

c. As part of the original contract using a cumulative catch-up.

d. As a combination of b and c.

For contracts for which the Group has decided there is a series of distinct goods and services that are substantially the same and have the same pattern of transfer where revenue is recognised over time, the modification will always be treated under a or b.

Judgement is applied in relation to the accounting for such modifications where the final terms or legal contracts have not been agreed prior to the reporting date, since management needs to determine if a modification has been approved and, if so, whether it creates new, or changes existing, enforceable rights and obligations of the parties. Depending upon the outcome of such negotiations, the timing and amount of revenue recognised may be different in different accounting periods. Modification and amendments to contracts are undertaken via an agreed formal process. For example, if a change in scope has been approved but the corresponding change in price is still being negotiated, management uses its judgement to estimate the change to the total transaction price. Importantly, any variable consideration is only recognised to the extent that it is highly probable that no revenue reversal will occur.

Contract-related assets and liabilities

As a result of the contracts into which the Group enters with its customers, a number of different assets and liabilities are recognised on the Consolidated Balance Sheet. These include contract assets and liabilities.

Contract assets and liabilities

The Group’s contracts with customers include a diverse range of payment schedules, depending upon the nature and type of goods and services being provided. The Group often agrees payment schedules at the inception of long-term contracts under which it receives payments throughout the terms of the contracts. These payment schedules may include performance-based payments or progress payments as well as regular monthly or quarterly payments for ongoing service delivery. Payments for transactional goods and services may be made at the delivery dates, in arrears or through part-payments in advance. Where cumulative payments made (or when the Group has an unconditional right to payment) at the reporting date are greater than the cumulative revenues recognised, the Group recognises the differences as contract liabilities. Where cumulative payments made at the reporting date are less than the cumulative revenues recognised, and the Group has an unconditional right to payment, the Group recognises the differences as contract assets or accrued income.

For the summary of revenue recognised by segment, refer to Note 2.2.

Below is a summary of timing of revenue recognition:

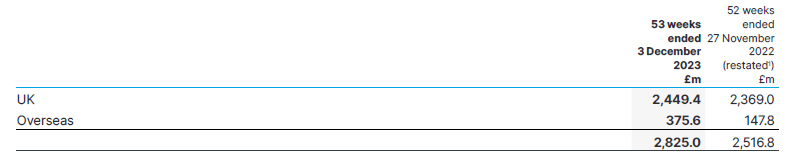

Revenue split by geographical area:

1. Refer to Note 1.2 for details.

No individual overseas region or country contributed more than 10% of total revenue.

Contract balances

Contract liabilities

The contract liabilities relate primarily to consideration received from Solutions customers in advance, for which revenue is recognised as the performance obligation is satisfied. The movement in contract liabilities during the current and prior period is:

£28.6m (FY22: £24.7m) of revenue recognised during the period was included in contract liabilities at the beginning of the period and £4.4m relates to revenue recognised from acquisition in the year (FY22: £nil).

Future transaction price

As well as the amounts currently held as contract liabilities, the Group anticipates receiving £172.2m (FY22: £152.4m) over the next four years in respect of upfront fees that are contracted but not yet due. These amounts represent the aggregate amount of contracted transaction price allocated to the committed performance obligations that are unsatisfied or partially satisfied as at the period end. The amounts received and to be received in respect of these performance obligations will be recognised in revenue from the go-live date over the estimated customer life. The total transaction price that the Group will earn over the estimated customer life also includes ongoing fees. These fees have been excluded from the disclosure as the Group has taken the practical expedient under IFRS 15.121(b) for revenues recognised in line with the invoicing.