Diageo plc – Annual report – 30 June 2025

Industry: food and drink

19. Contingent liabilities and legal proceedings (extract)

(f) Tax

The international tax environment has seen increased scrutiny and rapid change over recent years bringing with it greater uncertainty for multinationals. Against this backdrop, Diageo has been monitoring developments and continues to engage transparently with the tax authorities in the countries where it operates to ensure that the group manages its arrangements on a sustainable basis.

The group operates in a large number of markets with complex tax and legislative regimes that are open to subjective interpretation. In the context of these operations, it is possible that tax exposures which have not yet materialised (including those which could arise as part of tax assessments) may result in losses to the group. Where the potential tax exposures are known to us and may lead to a possible material outflow, the group assesses the disclosure of such matters as contingent liabilities, taking into account both assessed and unassessed amounts (if any), their size and nature, relevant regulatory requirements and potential prejudice of the future resolution or assessment thereof.

Diageo has a large number of ongoing tax cases in Brazil and India, for which contingent liabilities are disclosed on the basis of the current known possible exposure from tax assessment values. While not all of these cases are individually significant, the current aggregate known possible exposure from tax assessment values is up to approximately $906 million for Brazil and up to approximately $90 million for India. The group believes that the likelihood that the tax authorities will ultimately prevail is lower than probable but higher than remote. Due to the fiscal environment in Brazil and in India, the possibility of further tax assessments related to the same matters cannot be ruled out and the judicial processes may take extended periods to conclude. Based on its current assessment, Diageo believes that no provision is required in respect of these issues.

Payments were made under protest in India in respect of the periods 1 April 2006 to 31 January 2025 in relation to tax assessments where the risk is considered to be remote or possible. These payments have to be made in order to be able to challenge the assessments and as such have been recognised as a receivable in the group’s balance sheet. The total amount of payments under protest recognised as a receivable as at30 June 2025 is $120 million (corporate tax payments of $108 million and indirect tax payments of $12 million).

7. Taxation (extract 1)

Accounting policies

Current tax is based on taxable profit for the year. Taxable profit is different from accounting profit due to temporary differences between accounting and tax treatments, and due to items that are never taxable or tax deductible. Tax treatments are not recognised unless it is probable that a tax authority will accept the treatment. Once considered to be probable, tax treatments are reviewed each year to assess whether a provision should be taken against full recognition of the treatment on the basis of potential settlement through negotiation and/or litigation with the relevant tax authorities. Tax provisions are included in current liabilities. Penalties and interest on tax liabilities are included in operating profit and finance charges, respectively.

Full provision for deferred tax is made for temporary differences between the carrying value of assets and liabilities for financial reporting purposes and their value for tax purposes, except for deferred tax provision arising on goodwill from business combinations. The amount of deferred tax reflects the expected recoverable amount and is based on the expected manner of recovery or settlement of the carrying amount of assets and liabilities, using the basis of taxation enacted or substantively enacted by the balance sheet date. Deferred tax assets are not recognised where it is more likely than not that the assets will not be realised in the future. No deferred tax liability is provided in respect of any future remittance of earnings of foreign subsidiaries where the group is able to control the remittance of earnings and it is probable that such earnings will not be remitted in the foreseeable future, or where no liability would arise on the remittance.

Critical accounting estimates and judgements

The group is required to estimate the corporate tax in each of the jurisdictions in which it operates. Management is required to estimate the amount that should be recognised as a tax liability or tax asset in many countries which are subject to tax audits which by their nature are often complex and can take several years to resolve; current tax balances are based on such estimations. Tax provisions are based on management’s judgement and interpretation of country specific tax law and the likelihood of settlement. However, the actual tax liabilities could differ from the provision and in such event the group would be required to make an adjustment in a subsequent period which could have a material impact on the group’s profit for the year.

The evaluation of deferred tax asset recoverability requires estimates to be made regarding the availability of future taxable income. For brands with an indefinite life, management’s intention is to recover the book value through a potential sale in the future, and therefore the deferred tax on the brand value is generally recognised using the appropriate country capital gains tax rate. To the extent brands with an indefinite life have been impaired, management considers this to be an indication of recovery through use and in such a case deferred tax on the brand value is recognised using the appropriate country corporate income tax rate.

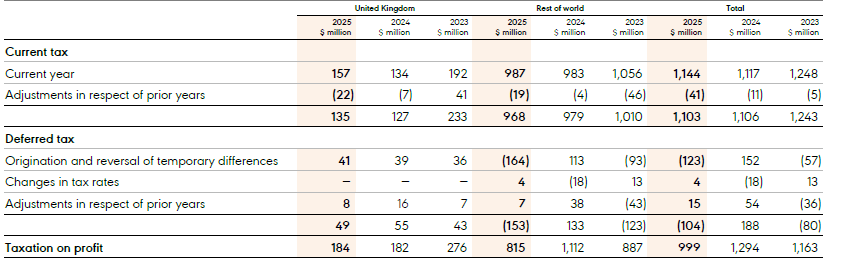

(a) Analysis of taxation charge for the year

(b) Exceptional tax charges/(credits)

The taxation charge includes the following exceptional items:

(1) In the year ended 30 June 2025, impairment charges recognised within exceptional operating items resulted in exceptional tax credits of $30 million in respect of Distill Ventures, $55 million in respect of the Aviation American Gin brand and tangible fixed assets, $40 million in respect of various US brands, tangible fixed assets and inventory and $13 million in respect of the Bell’s whisky brand. In the year ended 30 June 2024, an exceptional tax charge of $95 million was recognised in relation to the reversal of the Shui Jing Fang brand impairment charge, partially offset by an exceptional tax credit of $19 million in respect of the impairment of the Chase brand and the related tangible fixed assets and an exceptional tax credit of $13 million on brand impairments in the US ready-to-drink portfolio. In the year ended 30 June 2023, an exceptional tax credit of $154 million was recognised mainly in respect of the impairment of the McDowell’s brand.

(2) In the year ended 30 June 2025, an exceptional tax credit of $46 million was recognised in respect of restructuring programmes.

(3) In the year ended 30 June 2025, an exceptional tax credit of $36 million was recognised in respect of the transformation of the distribution model in France as the company agreed with LVMH to exit from their joint operation and to terminate the existing distribution agreements for Diageo brands.

(4) In the year ended 30 June 2025, an exceptional tax credit of $12 million was recognised in respect of various dispute and litigation matters in North America and Europe, including certain costs and expenses associated therewith. In the year ended 30 June 2024, an exceptional tax credit of $23 million was recorded in relation to various dispute and litigation matters in North America, including certain costs and expenses associated therewith.

(5) In the year ended 30 June 2023, the exceptional net tax charge of $37 million mainly comprised a tax charge of $52 million in respect of the sale of Guinness Cameroun S.A., partially offset by a tax credit of $11 million in respect of the sale of certain USL businesses.

(6) In the year ended 30 June 2025, an exceptional tax charge of $15 million was recognised in relation to the capitalisation of borrowing costs on the purchase of property, plant, equipment and computer software in the prior year.

(7) In the year ended 30 June 2023, an exceptional tax credit of $68 million was recognised in respect of the deductibility of fees paid to Diageo plc for guaranteeing externally issued debt of US group entities. Following engagement with the tax authorities, guarantee fees for the periods ended 30 June 2012 to 30 June 2022 are fully deductible.

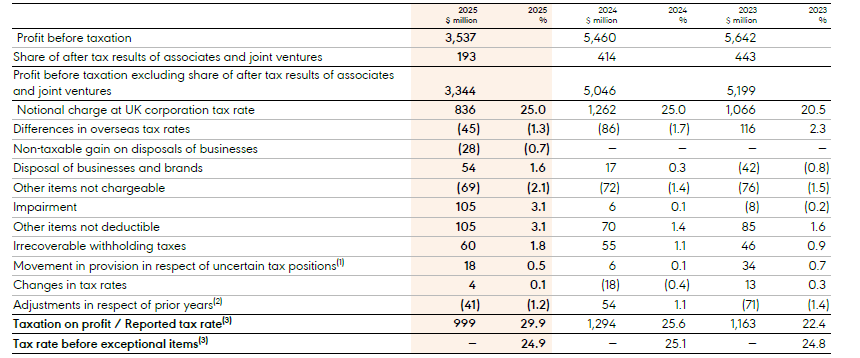

(c) Taxation rate reconciliation and factors that may affect future tax charges

(1) Movement in provision in respect of uncertain tax positions includes both current and prior year uncertain tax position movements.

(2) Excludes prior year movement in provisions. Included in the year ended 30 June 2023 was an exceptional tax credit of $68 million in respect of the deductibility of fees paid to Diageo plc for guaranteeing externally issued debt of its US group entities.

(3) Definitions of reported tax rate and tax rate before exceptional items have been revised to exclude the share of after tax results of associates and joint ventures from profit before taxation, as this represents post-tax profit, hence is considered as a non-essential factor of the calculation. The presentation of the reported tax rate and the tax rate before exceptional items for the years ended 30 June 2023 and 30 June 2024 has been aligned to the new definition.

The table above reconciles the notional taxation charge calculated at the UK tax rate, to the actual total tax charge. As a group operating in multiple countries, the actual tax rates applicable to profits in those countries are different from the UK tax rate. The impact is shown in the table above as differences in overseas tax rates. The group’s worldwide business leads to the consideration of a number of important factors which may affect future tax charges, such as the levels and mix of profitability in different jurisdictions, transfer pricing regulations, tax rates imposed and tax regime reforms, acquisitions, disposals, restructuring activities, and settlements or agreements with tax authorities.

Significant ongoing changes in the international tax environment and an increase in global tax audit activity mean that tax uncertainties and associated risks have been gradually increasing. In the medium-term, these risks could result in an increase in tax liabilities or adjustments to the carrying value of deferred tax assets and liabilities. See note 19(f).

The group has a number of ongoing tax audits worldwide for which provisions are recognised in line with the relevant international accounting standard, taking into account best estimates and management’s judgements concerning the ultimate outcome of the tax audits. For the year ended 30 June 2025, ongoing audits that are provided for individually are not expected to result in a material tax liability. The current tax asset of $354 million (30 June 2024 – $304 million) and tax liability of $138 million (30 June 2024 – $136 million) include $217 million (30 June 2024 – $209 million) of provisions for tax uncertainties.

The cash tax paid in the year ended 30 June 2025 amounts to $1,114 million (30 June 2024 – $1,099 million) and is $11 million higher than the current tax charge (30 June 2024 – $7 million lower). This arises as a result of timing differences between the accrual of income taxes, the movement in the provision for uncertain tax positions, the actual payment of cash and refund of the deposit payments.

In December 2021, the OECD released a framework for Pillar Two Model Rules which introduced a global minimum corporate tax rate of 15%, applicable to multinational enterprise groups with global revenue over €750 million. The legislation implementing the rules in the United Kingdom applies to Diageo from the financial year ended 30 June 2025. Diageo is continuously reviewing the amendments to the legislation and also monitoring the status of implementation of the model rules outside of the United Kingdom. Diageo has applied the temporary exception under IAS 12 in relation to the accounting for deferred taxes arising from the implementation of the Pillar Two Model Rules. A current tax expense of $7 million as a result of the Pillar Two Model Rules has been included in the total tax charge for the year ended 30 June 2025.

PRINCIPAL RISKS (extract)