Koninklijke Ahold Delhaize N.V. – Annual report – 1 January 2023

Industry: retail

24 PENSIONS AND OTHER POST-EMPLOYMENT BENEFITS (extract)

Multi-employer plans (MEPs)

A number of union employees in the United States are covered by MEPs based on obligations arising from collective bargaining agreements. These plans provide retirement and other benefits to participants generally based on their service to contributing employers. The benefits are paid from assets held in trust for that purpose. Trustees are appointed in equal number by employers and unions, and they are typically responsible for oversight of the investment of the assets and administration of the plan. Contribution rates and, in some instances, benefit levels are generally determined through the collective bargaining process between the participating employers and unions. At year-end, none of the Company’s collective bargaining agreements required an increase in the Company’s total pension contributions for MEPs to meet minimum funding requirements.

Most of these plans are defined contribution plans. The plans that are defined benefit plans, on the basis of the terms of the benefits provided, are accounted for as defined contribution plans because, among other things, there is insufficient information available to account for these plans as defined benefit plans. These plans are generally flat dollar benefit plans. Ahold Delhaize is generally one of several employers participating in most of these plans and, in the event that Ahold Delhaize withdraws from a plan, its allocable share of the plan’s obligations (with certain exceptions) would be based upon unfunded vested benefits in the plan at the time of such withdrawal. Ahold Delhaize’s obligation to pay for its allocable share of a plan’s unfunded vested benefits is called a withdrawal liability. The withdrawal liability payable by Ahold Delhaize at such time as it experiences a withdrawal from a plan is based upon the applicable statutory formula, plan computation methods and actuarial assumptions, and the amount of the plan’s unfunded benefits. Ahold Delhaize does not have sufficient information to accurately determine its ratable share of plan obligations and assets following defined benefit accounting principles, and the financial statements of the MEPs are drawn up on the basis of other accounting policies than those applied by Ahold Delhaize. Consequently, these MEPs are not included in the Company’s balance sheet.

The risks of participating in MEPs are different from the risks of single-employer plans. Ahold Delhaize’s contributions are pooled with the contributions of other contributing employers, and are, therefore, used to provide benefits to employees of these other participating employers. If other participating employers cease to participate in the plan without paying their allocable portion of the plan’s unfunded obligations, this could result in increases in the amount of the plan’s unfunded benefits and, thus, Ahold Delhaize’s future contributions. Similarly, if a number of employers cease to have employees participating in the plan, Ahold Delhaize could be responsible for an increased share of the plan’s deficit. If Ahold Delhaize seeks to withdraw from a MEP, it generally must obtain the agreement of the applicable unions and will likely be required to pay withdrawal liability in connection with this. If a MEP in which Ahold Delhaize participates becomes insolvent, Ahold Delhaize may be required to increase its contributions, in certain circumstances, to fund the payment of benefits by the MEP.

Under normal circumstances, when a MEP reaches insolvency, it must reduce all accrued benefits to the maximum level guaranteed by the United States’ PBGC. MEPs pay annual insurance premiums to the PBGC for such benefit insurance.

MEP – defined benefit plans

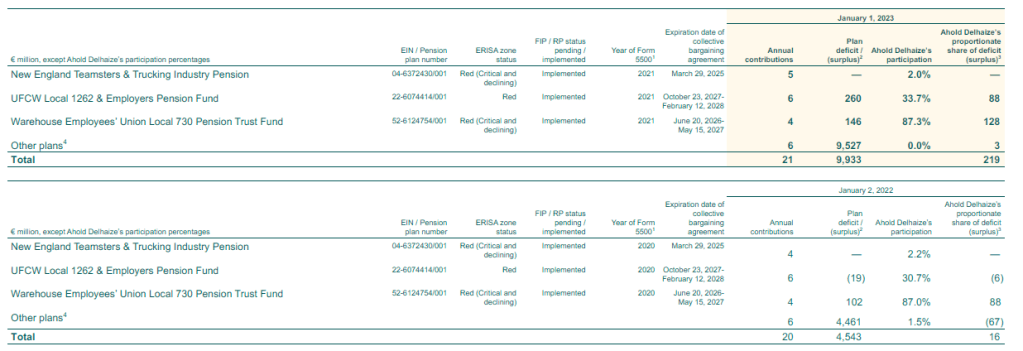

At the end of 2021 and 2022, Ahold Delhaize participated in seven MEPs that are defined benefit plans on the basis of the terms of the benefits provided. The Company’s participation in these MEPs is outlined in the following tables.

Ahold Delhaize’s participation percentage is an indication based on the relevant amount of its contributions during the year in relation to the total contributions made to the plan.

The estimate of the Company’s net proportionate share of the plans’ deficits is based on the latest available information received from these plans, such as the plans’ measurement of plan assets and the use of discount rates between 6.5% and 7.5%. The estimate does not represent Ahold Delhaize’s direct obligation. While it is our best estimate, based upon information available to us, it is imprecise, and a reliable estimate of the amount of the obligation cannot be made.

The EIN/Pension Plan Number column provides the Employer Identification Number (EIN) and the three-digit pension plan number. As with all pension plans, multi-employer pension plans in the U.S. are regulated by the ERISA; the United States Tax Code, as amended; the Pension Protection Act of 2006 (PPA); and the Multi-employer Pension Reform Act of 2014 (MPRA), among other legislation.

Under the PPA, plans are categorized as “endangered” (Yellow Zone), “seriously endangered” (Orange Zone), “critical” (Red Zone), or neither endangered nor critical (Green Zone). This categorization is based primarily on three measures: the plan’s funded percentage, the number of years before the plan is projected to have a minimum funding deficiency under ERISA and the number of years before the plan is projected to become insolvent. A plan is in the “Yellow Zone” if the funded percentage is less than 80% or a minimum funding deficiency is projected within seven years. If both of these triggers are reached, the plan is in the “Orange Zone.” Generally, a plan is in the “Red Zone” if a funding deficiency is projected at any time in the next four years (or five years if the funded percentage is less than 65%). Plans with a funding ratio above 80% are generally designated as being in the “Green Zone.” A plan in the “Red Zone” may be further categorized as “critical and declining” if the plan is projected to become insolvent within the current year or within either the next 14 years or the next 19 years, depending on the plan’s ratio of inactive participants to active participants and its specific funding percentage. MEPs in endangered or critical status are required by U.S. law to develop either a funding improvement plan (FIP) or a rehabilitation plan (RP) to enhance funding through reductions in benefits, increases in contributions, or both. The FIP/RP Status Pending/Implemented column in the table below indicates plans for which an FIP or an RP is pending or has been implemented. Additional information regarding the multi-employer plans listed in the following tables can be found on the website of the U.S. Department of Labor (www.efast.dol.gov).

1 Form 5500 is part of ERISA’s overall reporting and disclosure framework and includes the financial statements of a MEP.

2 The deficit/(surplus) of the plans is heavily influenced by the discount rate applied by the plans, which ranges between 6.5% and 7.5%, consistent with the prior year, and by the projected assets for the funds, which decreased by between 18% and 27%. MEPs discount the liabilities at the plan’s expected rate of return on assets. As a plan nearing insolvency reduces liquidity risk and expected volatility, its expected rate of return on assets declines and, as such, the discount rate will decline, resulting in an increase of the deficit within the plan. The steady liabilities, combined with a significant change in assets, has resulted in erosion of the funded status of these funds.

3 Ahold Delhaize’s proportionate share of deficit (surplus) is calculated by multiplying the deficit/(surplus) of each plan that the Company participates in by Ahold Delhaize’s participation percentage in that plan. This proportional share of deficit/(surplus) is an indication of our share of deficit/(surplus) based on the best available information. The deficit is calculated in accordance with the accounting policies and funding assumptions applied by the relevant plan and does not represent any obligation or liability Ahold Delhaize may have in respect of the plan, which would be accounted for and measured in accordance with Ahold Delhaize’s accounting policies.

4 Other plans include Teamsters Local 639 Employers Pension Plan, UFCW Local 464A Pension Fund, Bakery and Confectionery Union Pension Fund and IAM National Pension Fund, with participation percentages as of January 1, 2023, equal to 3.9%, 24.0%, 0.5% and 0.0%, respectively (January 2, 2022: 4.4%, 23.9%, 0.5% and 0.0%).

If the underfunded liabilities of the multi-employer pension plans are not reduced, by improved market conditions, reductions in benefits and/or collective bargaining changes, increased future payments by the Company and the other participating employers may result. However, all future increases generally will be subject to the collective bargaining process.

In 2020, Ahold Delhaize withdrew from the United Food & Commercial Workers International Union–Industry Pension Fund (the “National Plan”) and the United Food & Commercial Workers (UFCW) –Local 1500 Pension Fund (the “1500 Plan”), resulting in a total withdrawal liability of $634 million (€559 million) and $222 million (€183 million), respectively. In 2020, Ahold Delhaize paid $590 million, which included a transition payment to the new plan, as explained below. In 2021, Ahold Delhaize fully paid the remaining National Plan withdrawal liability in the amount of $190 million. In 2022, Ahold Delhaize paid $57 million on the withdrawal liability for the 1500 Plan. The outstanding withdrawal liability for the 1500 Plan, as of January 1, 2023, amounts to $57 million (€54 million) (January 2, 2022: $110 million (€97 million)). This withdrawal liability is recorded as a financial liability; see Note 23 for the non-current portion and Note 26 for the current portion.

For the National Plan, a new multi-employer variable annuity pension plan (VAPP) was established (effective retrospectively as of July 1, 2020). The new plan is a defined benefit plan and the Company applies defined benefit accounting (the plan is included in the Defined benefit plans above).

For the 1500 Plan, the Company will provide associates who are members of the UFCW Local 1500 future service retirement benefits through an existing defined contribution plan for which defined contribution accounting is applied.

In 2023, the Company expects its total contributions to multi-employer defined benefit plans to be €22 million, which includes RP contribution increases where applicable. Ahold Delhaize has a risk of increased contributions and withdrawal liability (upon a withdrawal) if any of the participating employers in an underfunded MEP withdraw from the plan or become insolvent and are no longer able to meet their contribution requirements or if the MEP itself no longer has sufficient assets available to fund its short-term obligations to the participants in the plan. If and when a withdrawal liability is assessed, it may be substantially higher than the proportionate share disclosed above. Any adjustment for a withdrawal liability will be recorded when it is probable that a liability exists and the amount can be reliably estimated. Ahold Delhaize does not have a contractual agreement with any MEP that determines how a deficit will be funded, except for the FELRA and MAP settlement agreement as described below.

FELRA and MAP settlement agreement

On December 31, 2020, Giant Food, UFCW Locals 27 and 400 (collectively the “Union Locals”), the PBGC, the Food Employers Labor Relations Association and United Food and Commercial Workers Pension Fund (“FELRA”) and the Mid-Atlantic UFCW and Participating Employers Pension Fund (“MAP”) finalized a settlement agreement on Giant Food’s funding obligations with respect to FELRA and MAP. As a result of this agreement, the PBGC approved the combining of MAP into FELRA (the “Combined Plan”) and agreed to provide financial assistance to the Combined Plan following its insolvency. The agreement intended to resolve all of Giant Food’s existing liabilities with respect to the FELRA and MAP Plans and improves the security of pension benefits for associates and reduces financial risk for Giant Food.

In 2020, Giant Food recorded a $609 million pension-related liability and a $211 million defined benefit obligation related to the new variable annuity single-employer plan, with a corresponding reduction in the Ahold Delhaize FELRA and MAP MEP off-balance sheet liabilities.

Beginning January 1, 2021, Giant associates who are represented by UFCW Locals 27 and 400 began to accrue benefits under a single-employer variable annuity plan. In 2021 and 2022, the best estimate of the defined benefit obligation was revised following the American Rescue Plan Act of 2021; see section below.

American Rescue Plan Act of 2021 (ARPA)

On March 11, 2021, the American Rescue Plan Act of 2021 (ARPA) was signed into law. ARPA establishes a special financial assistance program to be administered by the Pension Benefit Guaranty Corporation (PBGC) and funded by transfers from the U.S. Treasury through September 30, 2030. Under this program, eligible multi-employer pension plans may apply to receive a one-time cash payment intended to be the amount required for the plan to pay all benefits through the last day of the plan year ending in 2051. The payment received under this special financial assistance program would not be considered a loan and would not need to be paid back.

The Combined Plan is eligible for special financial assistance and submitted an application to the PBGC on December 30, 2021.The anticipated special financial assistance to the Combined Plan is expected to significantly delay the insolvency of the Combined Plan and consequently significantly reduce the liability of the single-employer plan for excess benefits for which Ahold Delhaize recorded a defined benefit liability in the amount of $211 million in 2020. On January 2, 2022, the best estimate was revised and the defined benefit obligation was reduced to $54 million.

The PBGC announced on April 29, 2022, that it has approved the application submitted to the Special Financial Assistance Program by the FELRA Pension Plan. The assistance that the Combined FELRA and MAP plan will receive is in line with the application submitted to the PBGC on December 30, 2021.

On July 6, 2022, the PBGC issued a final rule implementing changes to the Special Financial Assistance Program. The changes are responsive to public comments received on the PBGC’s interim final rule and will better protect the pensions earned by workers and retirees covered by multi-employer plans eligible for assistance. The final rule became effective on August 8, 2022, and it provides an option for filers under the interim rule to supplement the application for special financial assistance.

On August 8, 2022, the Combined FELRA and MAP plan supplemented its application to the PBGC. The amount of the liability for the excess benefits payable under Giant Food’s single-employer plan was reassessed as part of the supplemental application process, and the liability was reduced to $6 million during 2022, which represents the best estimate based on information available at the year end and includes judgment to determine the projected insolvency based on an assumed investment return.

ARPA has no impact on the FELRA and MAP withdrawal liability presented as Other long-term pension plan obligations. It also has no impact on the 2020 withdrawals from the National Plan and the 1500 Plan.

Eligible plans include, among others, plans that are in “critical and declining” status in any plan year beginning in 2020, 2021 or 2022. Applications for financial assistance must be submitted no later than December 31, 2025. In addition to the Combined Plan, each of the following plans to which various subsidiaries of Ahold Delhaize contribute are expected to be eligible, and to apply, for the special financial assistance:

- New England Teamsters & Trucking Industry Pension Plan

- Warehouse Employees’ Union Local 730 Pension Trust Fund

- Bakery and Confectionery Union and Industry Pension Fund

While ARPA is expected to provide financial assistance to the New England Teamsters & Trucking Industry Pension Plan, the Warehouse Employees’ Union Local 730 Pension Trust Fund and the Bakery and Confectionery Union and Industry Pension Fund, the expected future contributions to those multi-employer plans will not be impacted in the short term. The ongoing contribution requirements will continue to be based on the collective bargaining agreements in place. Accordingly, the special financial assistance for these three plans should not have any impact on Ahold Delhaize’s ongoing contribution obligation.

MEP – defined contribution plans

Ahold Delhaize also participates in 40 MEPs (2021: 39 MEPs) that are defined contribution plans on the basis of the terms of the benefits provided. The majority of these plans provide health and welfare benefits. The Company contributed €295 million and €283 million to multi-employer defined contribution plans during 2022 and 2021, respectively. These contributions are recognized as an expense in the consolidated income statement and related entirely to continuing operations in 2022 and 2021. These plans vary significantly in size, with contributions to the three largest plans representing 63% of total contributions (2021: 62%).