Unilever PLC – annual report – 31 December 2025

Industry: consumer goods

1. Accounting information and policies (extract)

ASSETS AND LIABILITIES HELD FOR SALE AND DISCONTINUED OPERATIONS

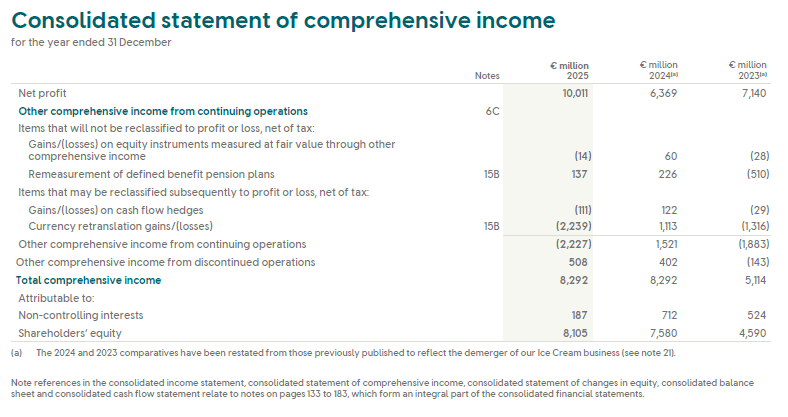

A disposal group is classified as held for sale or distribution when its carrying amount is expected to be recovered principally through a sale or distribution to shareholders rather than through continuing use. A discontinued operation is a component of the Group that has been disposed of or is classified as held for sale or distribution and represents a separate major line of business. In accordance with IFRS 5, the results of discontinued operations are presented separately in the consolidated income statement, consolidated statement of comprehensive income, consolidated statement of cash flows and related notes. Comparative information is re-presented to exclude the results of discontinued operations.

The Ice Cream business met the criteria to be classified as held for distribution in December 2025, following the Board’s formal approval of the demerger. At that point, the distribution was considered highly probable and the internal separation of the Ice Cream territories had been completed, meaning the business was available for distribution in its current condition. As a former reportable segment and major line of business, all Ice Cream activities have been treated as discontinued operations in both current and comparative periods.

In line with IFRS 5, we have disclosed separately in the income statement, statement of comprehensive income and cash flow statement results arising from continuing and discontinued operations. 2023 and 2024 comparatives have been re-presented on the same basis. There has been no change to the 2023 and 2024 balance sheet related amounts, including where balance sheet line item reconciliations have been disclosed within the notes. Further details and a breakdown of discontinued operations are provided in note 21.

CRITICAL ACCOUNTING ESTIMATES AND JUDGEMENTS (extract)

- Non-cash distribution to owners – the demerger of the Ice Cream business was executed through a distribution of shares in The Magnum Ice Cream Company (TMICC) to Unilever shareholders on 6 December 2025. A liability for the non-cash distribution was recognised when the distribution was authorised and no longer at the Group’s discretion, measured at the fair value of the assets to be distributed at that date. The distribution was settled on completion of the demerger, at which point the disposal group was derecognised. Judgement was required in determining the fair value of the Ice Cream business at the distribution date for the purpose of recognising the non-cash dividend in accordance with IFRIC 17 Distributions of Non-cash Assets to Owners. Management determined fair value with reference to the TMICC share price over a five-day period following listing. The resulting non-cash gain is recognised within profit or loss, within the result from discontinued operations. See note 21.

- Accounting for the retained stake in TMICC – management applied judgement in determining that Unilever does not hold significant influence over TMICC, and therefore TMICC is not an associate requiring accounting under the equity method. Whilst it is presumed that significant influence does not exist with a holding of less than 20 percent, careful consideration was given to the representation of Unilever on the board of TMICC, and material ongoing transactions between Unilever and TMICC.

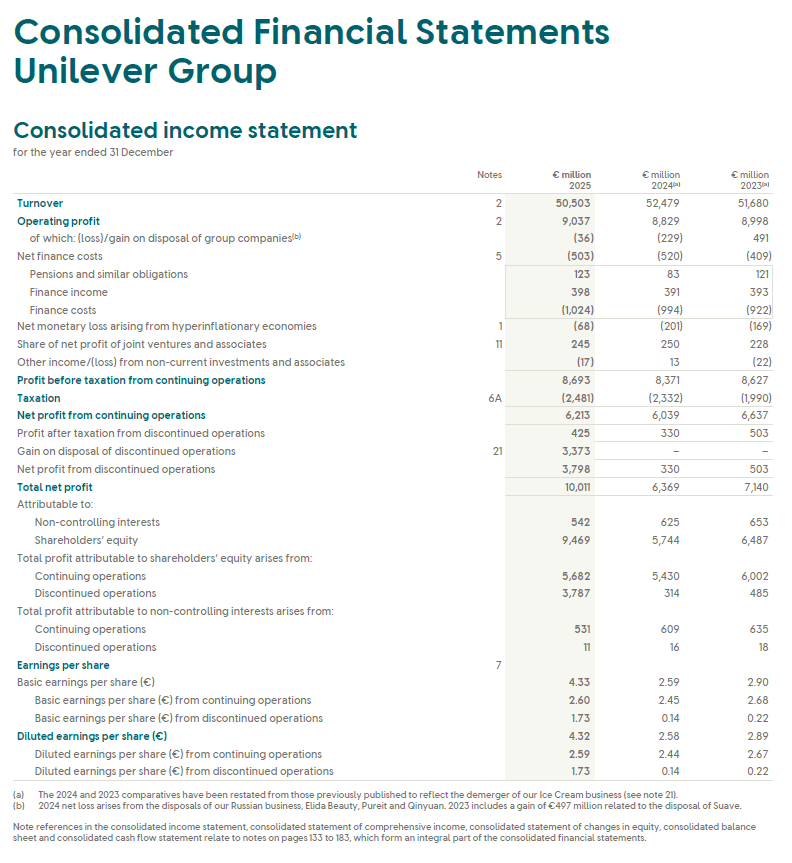

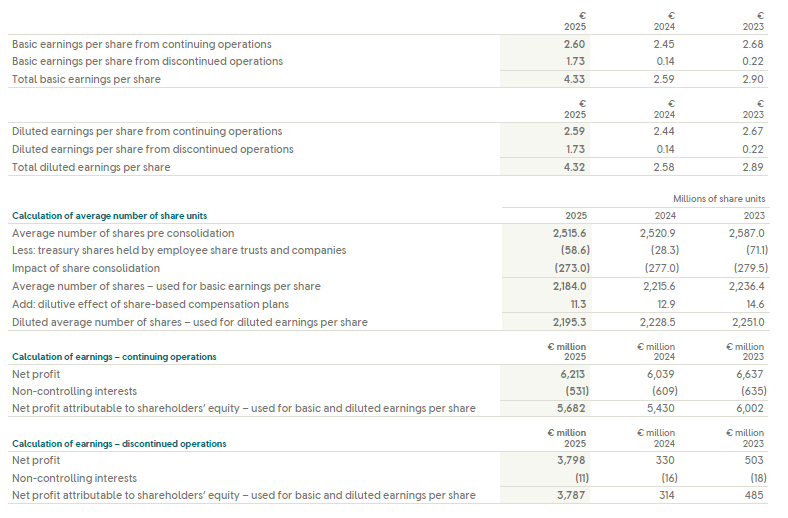

7. Earnings per share

The earnings per share calculations are based on the average number of share units representing the ordinary shares of PLC in issue during the period, less the average number of shares held as treasury shares. On 8 December 2025, Unilever PLC ordinary shares were consolidated to maintain share price comparability before and after the demerger of the Ice Cream business. Shareholders received 8 new Unilever shares with a nominal value of 31/2 pence each for every 9 existing ordinary shares which had a nominal value of 31/9 pence each. The overall effect of the share consolidation and demerger dividend did not constitute a share repurchase at fair value, therefore the average number of shares has been adjusted retrospectively for the impact of the share consolidation in all periods presented.

In calculating diluted earnings per share, a number of adjustments are made to the number of shares, principally, the exercise of share plans by employees.

Earnings per share for total operations for the 12 months were as follows:

8. Dividends on ordinary capital

Dividends are recognised on the date that the shareholder’s right to receive payment is established. This is generally the date when the dividend is declared.

From 1 January 2025, the Group declared dividends in euro (previously GBP). Four quarterly interim dividends were declared and paid during 2025, totalling €1.81/£1.55 (2024: £1.47) per PLC ordinary share.

A quarterly dividend of €1,017 million (2024: €1,121 million) was declared on 12 February 2026, to be paid in April 2026; €0.47/£0.41 per PLC ordinary share (2024: £0.38). Total dividends declared in relation to 2025 were €1.82/£1.58 (2024: £1.48) per PLC ordinary share.

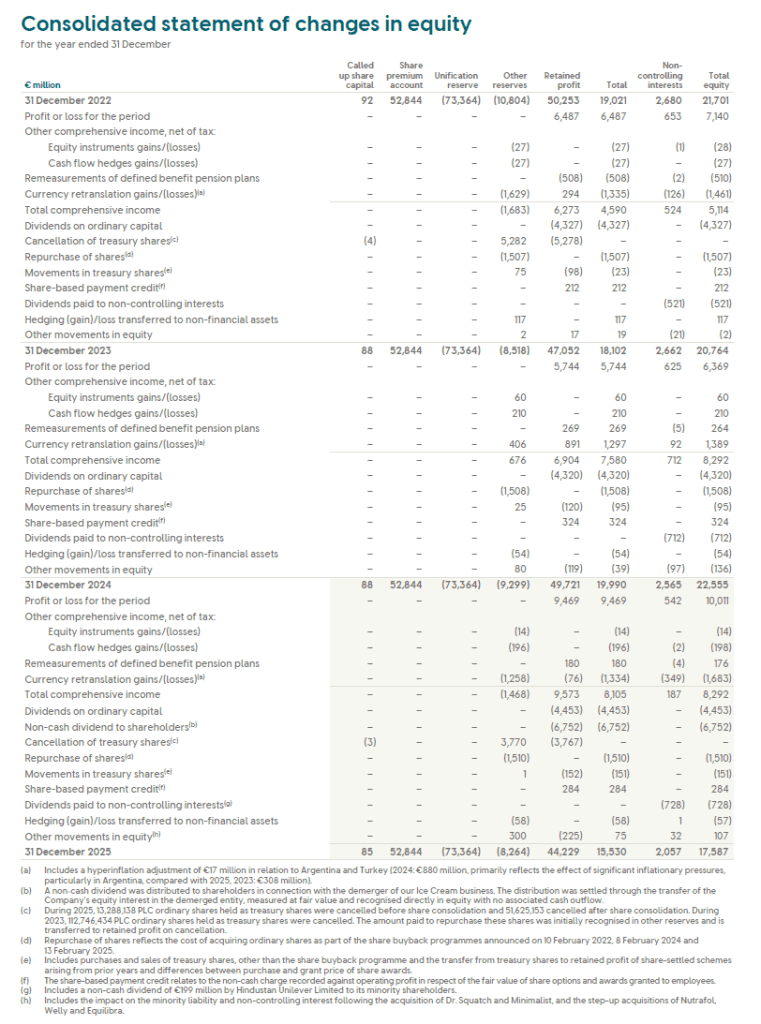

The demerger of the Ice Cream business was effected by Unilever PLC declaring an interim dividend in specie of The Magnum Ice Cream Company. The fair value of the distribution was €6,752 million.

21. Demerger of the Ice Cream Business

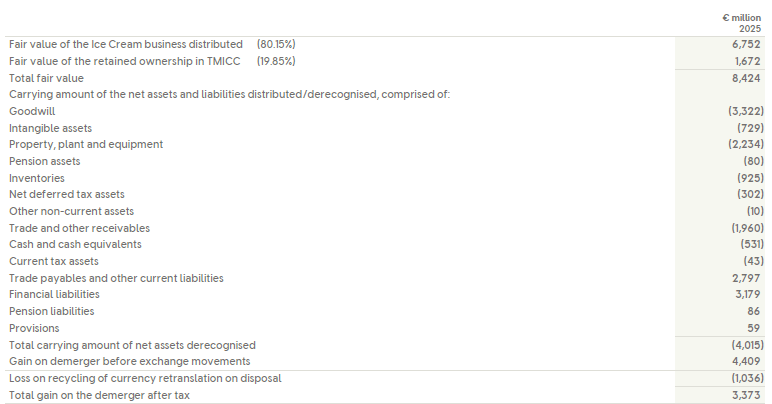

On 6 December 2025, Unilever completed the separation of its Ice Cream business, now known as The Magnum Ice Cream Company N.V. (‘TMICC’) an independent listed company incorporated and headquartered in the Netherlands. The separation was effected through a demerger of 80.15% of Unilever’s holding in TMICC to Unilever shareholders. Unilever retained a 19.85% stake in TMICC, which has been recognised as an equity investment. TMICC shares were admitted to trading on Euronext Amsterdam, the London Stock Exchange and the New York Stock Exchange on 8 December 2025.

Under IFRIC 17 ‘Distributions of Non-cash Assets to Owners’, a liability and an equity distribution are measured at the fair value of the assets to be distributed when the dividend is appropriately authorised and no longer at the entity’s discretion. The liability, dividend distribution and associated gain on demerger were recognised in December 2025 when the demerger distribution was authorised.

The fair value of the Ice Cream business was €8.4 billion. This was measured by reference to the daily closing quoted average TMICC share price over a five-day period post-listing, which was considered representative of the fair value at the distribution date. A gain on distribution of the Ice Cream business was recorded in the Income Statement in 2025. This gain is presented as part of discontinued operations and is exempt from tax.

The gain included €1.7 billion relating to the measurement of the retained stake to fair value using the same methodology. Any future gains or losses on the retained stake will be recognised in other comprehensive income.

The carrying value of the net assets of the Ice Cream business in the consolidated financial statements was €4.0 billion.

In addition, there was a reclassification of the Group’s share of cumulative exchange differences arising on translation of the foreign currency net assets from reserves to the income statement of €1.0 billion. The total gain on the demerger of the Ice Cream business was €3.4 billion.

Total gain on demerger calculation

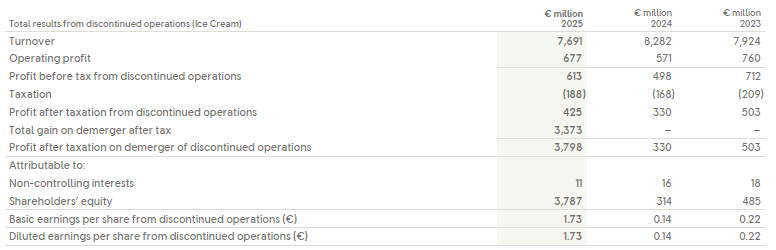

Financial information relating to the operations of Ice Cream is set out below and includes financial information up until the date of the demerger. We have reported everything from turnover to operating profit in line with what was previously disclosed for the Ice Cream business as discontinued operations for the financial years 2023 and 2024. Below operating profit, some allocations have been made to income and costs not historically reported as part of our segment information, where costs are shared by the Ice Cream business. We have recognised the India Ice Cream business as part of discontinued operations and recognised the related assets and liabilities as held for sale in the balance sheet, following an agreement to sell this business to The Magnum Ice Cream Company in the first half of 2026.

Unilever will continue to provide services (including IT infrastructure, marketing and co-packing services), supply materials, and continue to invoice and collect cash on behalf of The Magnum Ice Cream Company under a Transitional Services Agreement (TSA). The management fee for these services is recognised within operating profit. The TSA will continue for a maximum period of two years from the demerger of the Ice Cream business.

This financial information may differ, both in purpose and basis of preparation, from the Historical Financial Information and the Interim Financial Information included in The Magnum Ice Cream Company’s prospectus and from that which may be published by The Magnum Ice Cream Company. As a result, while the two sets of financial information may be similar, they may not be the same because of certain differences in accounting and disclosure under IFRS, including differences in perimeter.

The total results from discontinued operations are as follows (2025 results are for the year to date until 6 December):

Cash flows from discontinued operations included an operating inflow of €0.3 billion. Investing outflow was €0.7 billion, mainly from the cash de-recognised at the time of the demerger and capital expenditure. Financing activities contributed a €3.0 billion inflow, primarily from the bond issuance completed by TMICC. Of this bond finance, €2.7 billion was used to settle an intercompany position between TMICC and Unilever prior to the demerger. The total cash flows arising from discontinued operations are as follows (2025 results are for the year to date until 6 December):