Nikon Corporation – Annual report – 31 March 2025

Industry: manufacturing

17. Leases

(1) As Lessee

As a lessee, the Group primarily leases assets in respect to real estate such as office buildings and warehouses with some contracts containing extension or termination options. Extension options are options to renew the lease for a certain amount of time after the end of the lease term. Termination options are options that allow the lessee to early terminate the lease if the lessee gives a written notice to the lessor prior to the contracted end of the lease term. These options are exercised by the Group by considering real estate price trends and business environment to determine if the lease shall be renewed or terminated for business operations.

There are no escalation clauses or restrictions on dividends, additional borrowings and additional leases provided by the lease contracts.

1) Carrying Amount, Additions and Depreciation of Right-of-use Assets

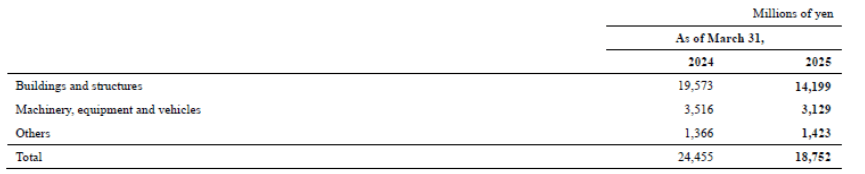

The carrying amount of right-of-use assets is as follows:

Additions to right-of-use assets amounted to ¥11,183 million and ¥6,402 million for the years ended March 31, 2024 and 2025, respectively.

Depreciation of right-of-use assets is as follows:

Note: Depreciation of right-of-use assets is recognized in “Cost of sales” and “Selling, general and administrative expenses” in the consolidated statement of profit or loss.

2) Income and Expenses Relating to Leases

Income relating to leases, which is recognized in the consolidated statement of profit or loss, is as follows:

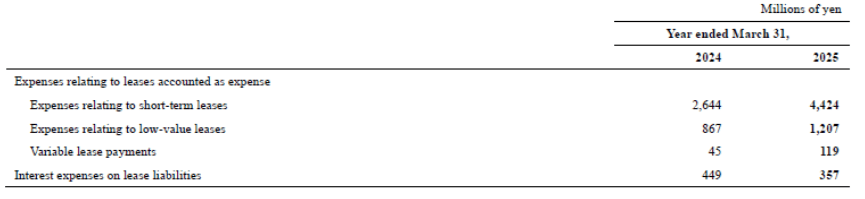

Expenses relating to leases, which are recognized in the consolidated statement of profit or loss, are as follows:

3) Cash Outflow for Leases

Cash outflow for leases, which is recognized in the consolidated statement of cash flows, is as follows:

4) Lease Liability

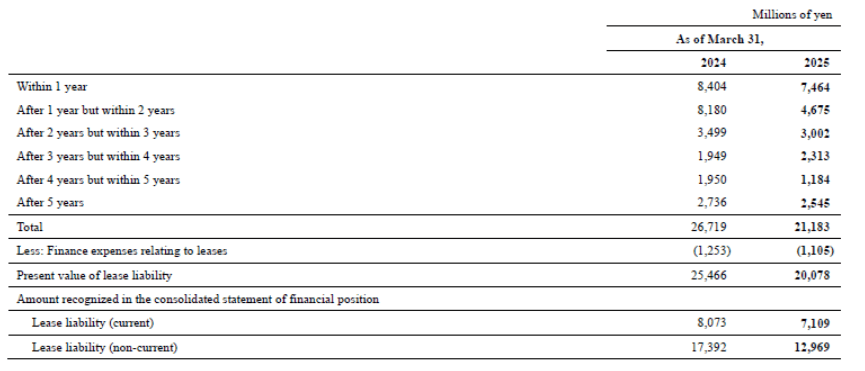

The breakdown of lease liability by maturity is as follows:

(2) As Lessor

1) Finance Leases

The Group mainly leases ultra-wide field retinal imaging devices under finance leases.

The selling profits from finance leases for the years ended March 31, 2024 and 2025 were ¥6,697 million and ¥6,535 million, respectively.

The finance income on the net investment in the lease and the income relating to variable lease payments are as follows:

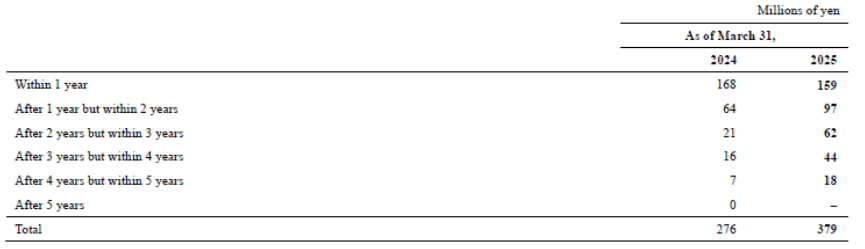

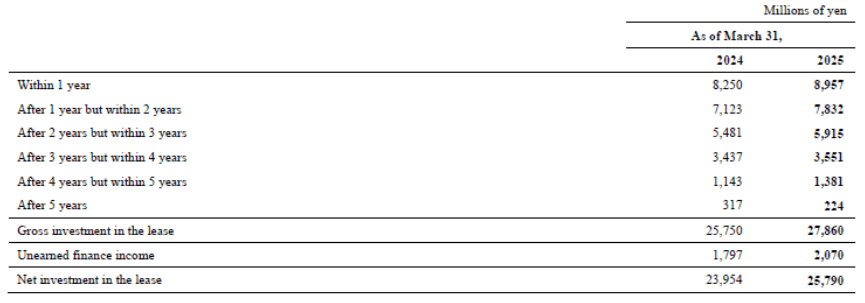

The breakdown of the gross investment in the lease by maturity is as follows:

2) Operating Leases

The Group mainly leases robotic motion control camera equipment under operating leases.

Lease income from operating leases of ¥780 million and ¥561 million were recognized in the consolidated statement of profit or loss for the years ended March 31, 2024 and 2025, respectively.

Lease income includes income of ¥29 million and ¥22 million relating to variable lease payments that do not depend on an index or a rate for the years ended March 31, 2024 and 2025, respectively.

The breakdown of lease receivables by payment due date is as follows: