Mowi ASA – Annual report – 31 December 2025

Industry: agriculture

Note 2 – Accounting policies (extract)

Revenue

Revenue from contracts with customers is recognised when control of the goods are transferred to the customer at an amount that reflects the consideration to which the Group expects to be entitled in exchange for those goods. The Group has generally concluded that it is the principal in its revenue arrangements, because it typically controls the goods before transferring them to the customer.

Sale of fish products

Revenue for the Group derives mainly from the sale of fish and elaborated fish products either on spot sales or from contracts. The Group recognises revenue from the sale of fish and elaborated fish products at the point in time when control of the goods is transferred to the customer. Revenue is generally recognised on delivery of the goods (i.e. a certain point in time). Based on group business of sale of fish and elaborated fish products the customers do not pay any advances. The normal credit term is 30 days upon delivery, and based on the nature of the product there is generally no right of return or warranties. Refund is only given if delivered goods is damaged or delivered with discrepancy compared to agreement, such is immaterial.

The Group considers whether there are other promises in the contract that are separate performance obligations to which a portion of the transaction price needs to be allocated, currently no multiple performance obligations have been identified. In determining the transaction price for the sale of goods, the Group considers the effects of variable consideration, the existence of significant financing components and consideration payable to the customer (if any). At the balance sheet date the group has no outstanding performance obligations in contracts that have original duration of more than 1 year.

Biomass

Changes in the estimated fair value of the biomass are recognised in profit or loss. The fair value adjustment is presented in the statement of comprehensive income as “Net fair value adjustment biomass”. The net fair value adjustment consists of “fair value adjustment on biological assets”, “fair value adjustment on harvested fish” and “fair value on incident based mortality”, see Note 6. The fair value adjustment on biological assets represents the change in fair value of the biomass less the change in accumulated cost of production for the biomass. The fair value adjustment on harvested fish is the release from stock of the fair value adjustment related to the fish harvested in the period. The fair value adjustment on incident based mortality is the release from stock of the fair value adjustment related to the fish recognised as incident based mortality in the period. The accumulated cost of incident based mortality is included in “cost of materials” in the statement of comprehensive income.

Biological assets

Fair value of biological assets is calculated based on a present value model which does not rely on historical cost. Fish ready for harvest (mature fish), are valued at expected sales price with a deduction of cost related to harvest, transport etc. For fish not ready for harvest (immature fish), cost to completion is also deducted. The model uses an interpolation methodology where the known data points are the value of the fish when put to sea and when recognised as mature fish. Technically, the interpolation is calculated per location. The effect of this is that fish that have the same weight and quality are valued similarly. The interpolation model has a natural interpretation in the form of a present value calculation where an imputed rent of assets (i.e. theoretical license rent) per location is included as part of the rate of return. Thus, the value is to a lesser degree affected by the site because low production cost at a high quality site is offset by a higher imputed rent and vice versa. All surplus return in the future is assigned to the licenses through a similarly high imputed rent of assets, and where any shortage in return is recognised in profit and loss immediately. The interpolation model is updated every month, with best estimates for time of harvest, remaining months at sea, expected price at time of harvest and estimated residual cost to grow the fish to harvest weight. The methodology has the effect that any changes in price will have full effect on the biomass at hand, while the price effect on increased weight going forward will be allocated to the license and recognised over time as remaining time at sea decreases. An effect of this is that even with high salmon prices there is no profit at the time the fish is put to sea because all surplus return is assigned to future periods (licenses). Correspondingly the fair value of small fish is rather insensitive to price fluctuations.

An interpolation model as described works best if important variables such as pace of growth, mortality and feed conversion ratios are constant per unit of time or weight increase. Experience shows that in particular there is a deviation from an even development during the first period in sea relating to increased value due, among other things to reduced risk after handling of the fish, vaccination and mortality related to the transfer to sea. This has been adjusted for.

Biological assets comprise eggs, juveniles, smolt and fish in the sea. Biological assets are, in accordance with IAS 41 and IFRS 13, measured at fair value less cost to sell. In line with IFRS 13, the highest and best use of the biological assets is applied for the valuation. In accordance with the principle for highest and best use, the fish is considered to have optimal harvest weight at 4 kg gutted. This corresponds to that a live weight of approximately 4.8 kg (there may be regional variances) or more are classified as mature fish, while fish that have still not achieved this weight are classified as immature fish. All fish at sea are subject to a fair value calculation, while broodstock and smolt are measured at cost less impairment losses.

The calculation of the estimated fair value is based on market prices for harvested fish and adjusted for estimated differences in accordance with IFRS 13. The prices are reduced for harvesting costs and freight costs to market, to arrive at a net value back to farm. The valuation reflects the expected quality grading and size distribution. The valuation is completed for each Business Unit and is based on the biomass in sea for each seawater site and the estimated market price in each market derived from the development in recent contracts as well as spot prices. Where reliable forward prices are available, those have been used. The change in estimated fair value is recognised in profit or loss based on measurement as of each period, and is classified separately. At harvest, the fair value adjustment is classified as fair value adjustment on harvested fish. In cases of incident based mortality, the fair value adjustment is classified as fair value adjustment on incident based mortality when occurring. Both are included in net fair value adjustment of biological assets in the statement of comprehensive income.

Onerous contracts

At each reporting date, management assesses if there are contracts in which the unavoidable costs of meeting the Group’s obligations under the contract exceed the economic benefits expected to be received in accordance with IAS 37. Fair value adjustment of biological assets is included in the unavoidable cost. This implies that the contract may be considered onerous even though the actual production cost of the products sold is lower than the contract price. Volumes used in the calculation is based on estimated remaining volumes for the contracts. Onerous contracts are classified as provisions in the statement of financial position.

Note 3A – Estimates and judgements (extract)

Estimates (extract)

Biological assets

Biological assets comprise eggs, juveniles, smolt and fish in the sea. These assets are measured at fair value less cost to sell, unless the fair value cannot be measured reliably. The estimation of the fair value relies on a series of uncertain assumptions, e.g., biomass volume, biomass quality, size distribution, market prices, expected future costs, remaining time to harvest and total time to harvest.

Mowi measures all deviations in biomass volume compared to estimates when a site is harvested out. Except for situations where there has been an incident causing mass mortality, particularly early in the cycle, combined with an inability to count and weigh fish after the event in fear of further stressing the fish, volume deviations are normally minor. Similarly, excluding the effects of soft flesh and melanin, the quality of the fish can normally be estimated with a relatively high degree of accuracy. Categorisation of quality is normally set per country based on averages, but can be set individually per site when needed. The size distribution shows some degree of variation but normally not to an extent that significantly changes the estimated value of the biomass (the value of two fish at five kg is very similar to the value of two fish weighing four and six kg, respectively).

The accumulated cost of the fish per kg will only deviate from the estimate if the volume is different from the estimate. For the estimation of future costs, there is uncertainty with regard to feed prices, other input costs and biological development. Mowi measures cost deviations vs. budget as part of the follow up of business units. Excluding special situations (incidents etc.), the deviations in costs vs budgets are normally limited for a group of sites, although individual sites might show deviations. The estimation of costs influences the biomass value through the recognised fair value adjustment in the statements of comprehensive income and financial position (calculated as fair value less accumulated biological costs).

The key element in the estimation of fair value is the assumed market price. The assumed market price is the price that we expect to receive on the future date when the live fish is harvested. We derive these prices from a variety of sources, normally a combination of the prices achieved in the previous month and the contracts most recently entered into. For salmon of Norwegian, Scottish, Icelandic and Faroese origin, quoted forward prices (Sisalmon) are normally used in the estimation, see Note 2. The use of third-party forward prices improves the reliability and comparability of the price estimation.

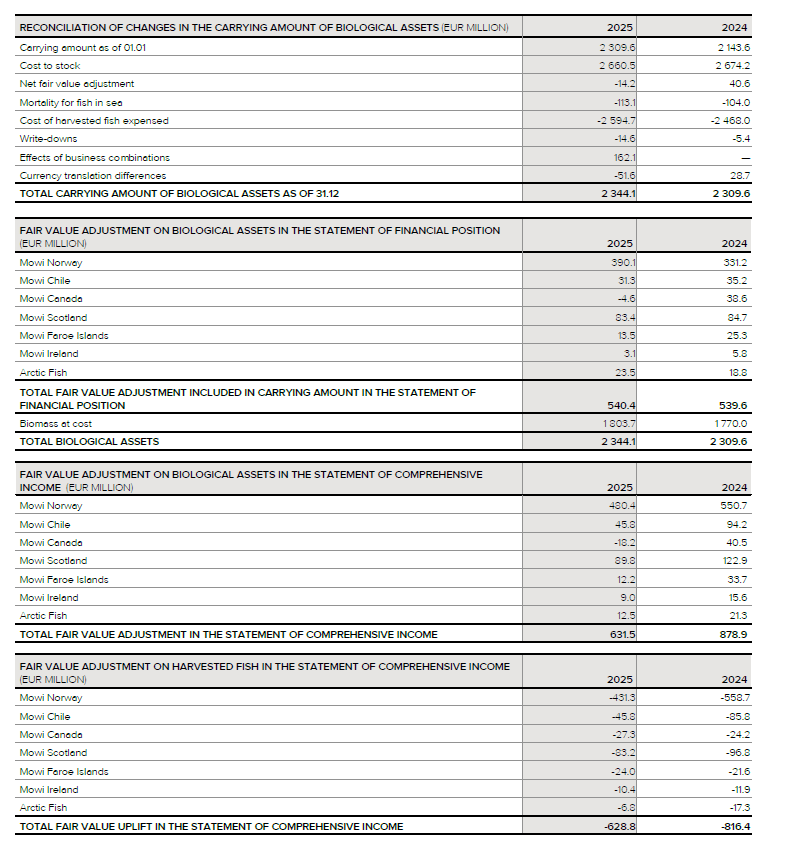

For further information about biological asset values please see Note 6, Biological assets.

Note 3B – Environmental risk

Climate change represents both risks and opportunities for Mowi. We recognise the growing significance of climate change on our business and the increasing role of producing food from the ocean as a solution to climate change. Mowi has developed a sustainability strategy, the Leading the Blue Revolution Plan. It sets ambitious goals to ensure our salmon is raised in the ocean in harmony with nature, using an eco-efficient value chain while offering solutions to global challenges such as climate change and food security.

Climate change has been identified as an operational, strategic, reporting and compliance risk to Mowi which can potentially impact our business in the short, medium, and long term. Mowi follows the COSO (Committee of Sponsoring Organisations) enterprise risk framework to assess and identify risks, including climate change risks. The risk of climate change on Mowi’s financial position can be classified into two types of risks; physical risk and transition risk. Physical risks are related to the increase and severity of extreme weather and long-term environmental changes. The physical related climate risks relate mainly to extreme weather events and increased seawater temperatures which can impact the risk of escape incidents, the frequency of algae blooms, and the availability of the raw materials for our fish feed (medium to long term impact). Transition risks refer to the changes in technological advancements within clean energy, shifts in consumer behaviour and political interventions, such as restrictions and costs related to emissions etc. The transition risks and opportunities include legislation or regulations imposing overall caps or taxes on greenhouse gas emissions (short-medium term impact). An increased recognition of seafood as a low carbon footprint protein is a transitional opportunity for Mowi.

These risks can affect Mowi in multiple ways, such as winters storms or El Niño giving tougher conditions, an increase of algae blooms and jelly fish due to increased water temperature can reduce quality and cause mortality on fish reducing revenue, or result in increased operating expenses with increased level of maintenance on nets and pens with tougher climate and expenses based on access to raw material in our fish feed, additional expenses for taxes with new regulation, or expenses to adapt our way of business to changed expectations from stakeholders. The changes, however, can also provide opportunities with faster growing fish in higher sea temperatures and increased revenues as well on the uptake of new technology. The risk can also impact the carrying amount and useful life of both tangible and intangible assets as weather tear or regulation might require earlier replacements.

These risks and opportunities are part of our risk assessment as part of the annual budget and long term plan process and considered in our impairment testing at year end. The long-term effects of climate change are uncertain, but we believe that Mowi will play an increasing role in producing healthy nutritious food through an eco-efficient value chain. No impairment related to environmental risk is recognised as of year end and there has been no change in useful life for our assets.

Note 6 – Biological assets

Valuation of biological assets

Biological assets are, in accordance with IAS 41, measured at fair value less cost to sell. All fish at sea are subject to a fair value calculation, while broodstock and smolt are measured at cost less impairment losses.

Biomass measured at fair value, is categorised at Level 3 in the fair value hierarchy, as the input is mostly unobservable. In line with IFRS 13, the highest and best use of the biological assets is applied for the valuation. In accordance with the principle for highest and best use, we consider that the fish have optimal harvest weight at 4 kg gutted. This corresponds to a live weight of approximately 4.8 kg (there may be regional variances). Fish of this weight or above are classified as ready for harvest (mature fish), while fish that have still not achieved this weight are classified as not ready for harvest (immature fish). The valuations are carried out at business unit level based on a common model and basis for assumptions established at group level. All assumptions are subject to monthly quality assurance and analysis at the group level.

The valuations are based on an income approach and takes into consideration unobservable input based on biomass in the sea, the estimated growth rate and cost to completion at site level. Mortality, quality of the fish going forward and market price are considered at business unit level. A special assessment is performed for sites with high/low performance due to disease or other deviating factors. The market prices are derived from observable market prices where available.

Assumptions used for determining fair value of live fish

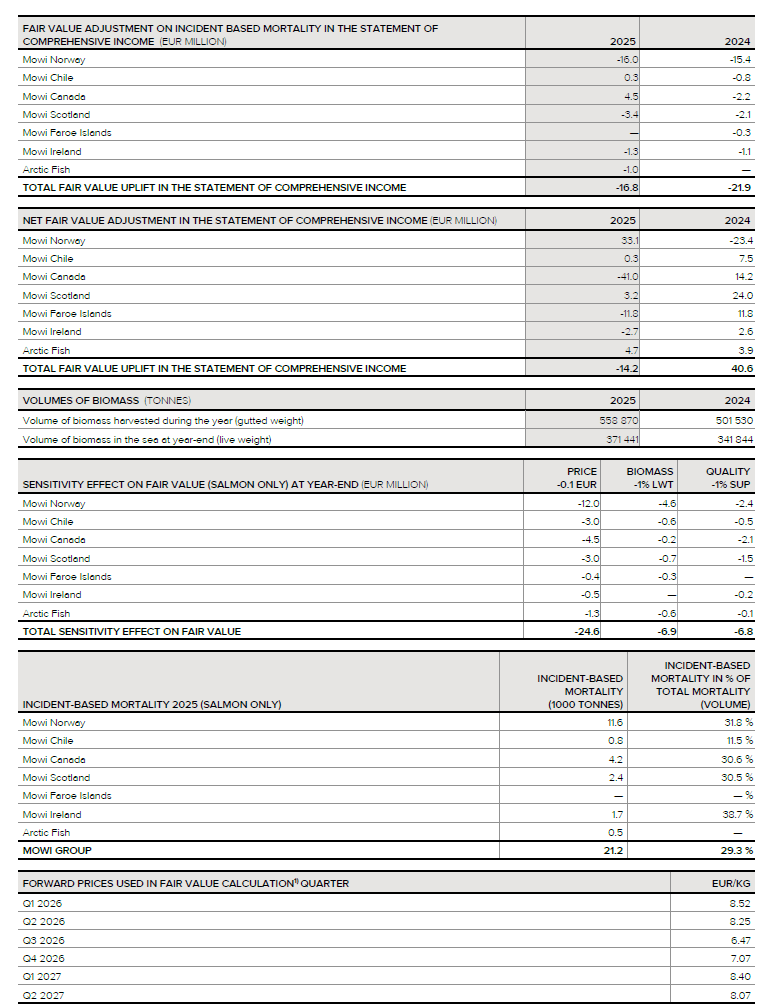

The estimated fair value of the biomass will always be based on uncertain assumptions, even though the group has built substantial expertise in assessing these factors. Estimates are applied to the following factors; biomass volume, the quality of the biomass, size distribution, cost, mortality and market prices.

Biomass volume: The biomass volume is in itself an estimate based on the number of smolt released into the sea, the estimated growth from the time of stocking, estimated mortality based on observed mortality in the period, etc. There is normally little uncertainty with regard to biomass volume.

The level of uncertainty will, however, be higher if an incident has resulted in mass mortality, especially early in the cycle, or if the fish’s health status restricts handling. If the total biomass at sea was 1% lower than our estimates, this would result in an change in value of EUR -6.9 million.

The quality of the biomass: The quality of the biomass can be difficult to assess prior to harvesting, if the reason for downgrading is related to muscle quality (e.g. the effect of Kudoa in Canada). In Norway downgraded fish is normally priced according to standard rates of deduction compared to a Superior quality fish. In our fair value model for salmon of Norwegian origin, we have used EUR 2.00 as deduction from Superior to Production grade quality. In other countries the price deductions related to quality are not as standardised. Due to the challenging winter sore situation in Norway in the first half, group superior rate was 91% in 2025 (87% in 2024). A one percentage point change from Superior quality to Production grade quality would result in a change in value of EUR -6.8 million.

The size distribution: Fish in sea grow at different rates, and even in a situation with good estimates for the average weight of the fish there can be a considerable spread in the quality and weight of the fish. The size distribution affects the price achieved for the fish, as each size category of fish is priced separately in the market. When estimating the biomass value, a normal size distribution is applied.

Cost: For the estimation of future costs, there is uncertainty with regard to feed prices, other input costs and biological development. Mowi measures cost deviations vs. budget as part of the follow up of business units. Excluding special situations (incidents etc.), the deviations in costs vs budgets are normally limited for a group of sites, although individual sites might show deviations. The estimation of costs influences the biomass value through the recognised fair value adjustment in the statements of comprehensive income and financial position (calculated as fair value less accumulated biological costs).

Mortality: Normalised mortality will affect the fair value estimates both as a reduction of estimated harvesting volumes and because cost to completion includes cost incurred on fish that eventually will perish.

Market price: The market price assumption is very important for the valuation and even minor changes in the market price will result in significant changes in the valuation. The methodology used for establishing the market price is explained in Note 2. A EUR 0.1 decrease in the market price would result in a decrease in value of EUR 24.6 million.

The market price risk is reduced through fixed price/volume customer contracts and financial contracts, as well as our downstream integration as explained in Note 13.

Climate Risk : Climate risk is included in the assessment for calculating the Fair value of live fish. Due to the short time period relevant for the Fair value uplift (maximum of 2 years) climate risk has not had a material effect on the valuation of biomass in sea.

Write-down of biomass and incident-based mortality

Incident-based mortality is accounted for when a site either experiences elevated mortality over time or substantial mortality due to an incident at the farm (outbreak of disease, lack of oxygen etc). The cost of incident based mortality is included in “cost of materials” in the statement of comprehensive income. The fair value element is adjusted through fair value adjustment on incident based mortality, and included in net fair value adjustment in the statement of comprehensive income.

1) Norway, Faroe Islands and Arctic Fish only. Before reduction of export costs.

Note 13 – Capital management and risk management (extract)

Price/liquidity risk

The Group is continuously monitoring liquidity and estimates expected liquidity development on the basis of budgets and monthly updated forecasts from the business units. Mowi’s financial position and development depend significantly on spot price developments for salmon, and these prices have historically been volatile. As such Mowi is exposed to movements in supply and demand for salmon. Mowi has to some extent mitigated its exposure to spot prices by entering into bilateral fixed price/volume contracts with its customers. The contract share has normally varied between 20% and 50% of our sold volume, however hedged volumes can increase up to 65% under special circumstances, and the duration of contracts has typically been three to eighteen months. Furthermore Mowi reduces its exposure to spot price movements through value-added processing activities and tailoring of products for its customers. Other key liquidity risks are fluctuations in production and harvest volumes, biological issues, and changes in the feed price, feed being the most important individual factor on the cost side. Feed costs are correlated to the marine and agricultural commodity prices of the ingredients.

A portion of the Group’s trade payables are included in the Group’s supply chain financing agreements and thus have financial institutions as counterparties, rather than individual suppliers. This results in the Group being required to settle a certain amount with a single counterparty, rather than less significant amounts with several counterparties. Management does not consider the supply chain finance agreements to result in excessive concentrations of liquidity risk.

Mowi’s aim is to maintain a balance between long-term financing and flexibility by using credit facilities, new borrowings and bonds.

Note 19 – Secured liabilities and guarantees (extract)