SimCorp A/S – Annual report – 31 December 2021

Industry: computer software

2.4 Contract balances

Contract balances consist of client-related assets and liabilities.

Contract assets

Contract assets relate to the Group’s rights to consideration for software licensed to clients under subscription agreements with future payments, when that right is conditional on SimCorp’s future performance.

If the timing of payments specified in the contract provides the client with a significant financing benefit, the transaction price is adjusted to reflect this financing component.

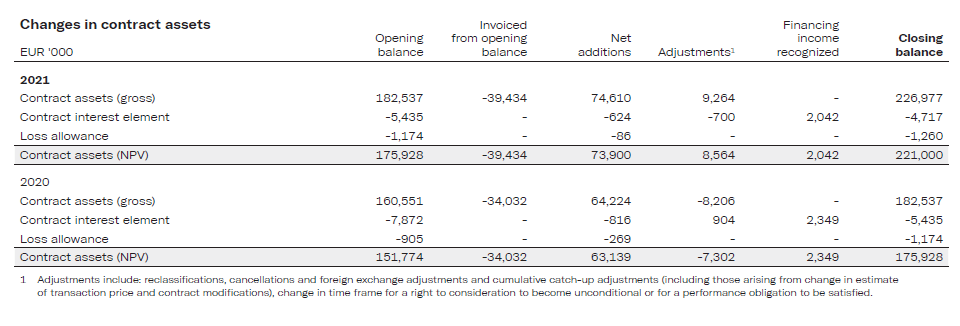

Contract assets increased by EUR 45.1m with subscription-based licenses adding EUR 84.8m (2020: EUR 67.3m) and finance income recognized EUR 2.0m (2020: EUR 2.3m). Foreign exchange as well as adjustments also had a positive impact partly off-set by deduction of expected credit loss provision with overall positive impact of EUR 8.6m (2020: EUR -7.3m). The overall balance was reduced by invoiced subscription-based license fees of EUR 50.3m (2020: EUR 37.9m).

Contract liabilities

When a client pays consideration in advance, or an amount of consideration is due contractually before transferring of the license or service, then the amount received in advance is presented as a liability. Contract liabilities represent mainly prepayments from clients for unsatisfied or partially satisfied performance obligations in relation to licenses, software updates and support, and services. Software updates and support and hosting billing generally occurs at periodic intervals (e.g. quarterly or yearly) prior to revenue recognition, resulting in liabilities.

The majority of license agreements are recognized as revenue in the year of sale. However, contracts with functionality gaps or acceptance criteria may have revenue recognition deferred, resulting in a contract liability when payment has occurred.

Contracts in progress relating to fixed fee professional services are measured at the estimated sales value of the proportion of the contract completed at the statement of financial position date.

Periodic fixed fees for subscription services, software updates and support services, and other multiperiod agreements are typically invoiced yearly or quarterly in advance. Such fee prepayments account for the majority of our contract liability balance.

Fees based on actual transaction volumes for SCDaaS subscriptions and fees charged for non-periodical services are invoiced as the services are delivered. While payment terms and conditions vary by contract type and region, our terms typically require payment within 30 to 60 days.

Accounting policies, judgments and estimates

Amounts invoiced on account in excess of work completed are included in prepayments under current liabilities.

Contract assets from contracts with customers are measured at amortized cost less expected credit losses. Contract assets are within the scope of impairment requirements in IFRS 9.

For contract assets the simplified approach is used, and the expected loss provision is measured at the estimate of the lifetime expected credit losses.

Expected loss rates between 0.03% – 14.13% are applied (2020: 0.04% – 13.36%), based on average default rates by region as published by Standard & Poor. For additional information refer to note 6.2 Risk.

Judgment is required in determining whether a right to consideration is conditional and thus qualifies as contract assets. Estimates are made as to whether and to what extent subsequent concessions or payments may be granted to customers and whether the customer is expected to pay the contractual fees. In this judgment, trading history is considered both with the respective customer and more broadly.

Incremental Costs of Obtaining Customer Contracts

The Group expenses the incremental costs of obtaining a customer contract as incurred. The incremental costs of obtaining a customer contract primarily consist of sales commissions earned by the sales force. Commissions are typically related to the license fee which is recognized upfront upon delivery, consequently, we expense sales commissions concurrently with revenue recognition.

Costs to Fulfill Customer Contracts

The Group does not capitalize costs incurred to fulfil customer contracts. Direct costs for custom development and standard platform are expensed as incurred.

2.5 Receivables

Accounting policies

Receivables are recognized when control over licenses or services, etc. is transferred to a client before the client pays consideration and the right to consideration is not conditional on SimCorp’s future performance.

Trade receivables represent receivables which have been invoiced to clients and remain outstanding. Accrued revenue consists mainly of revenue from the sale of perpetual software licenses and receivables from professional services contracts in progress which are yet to be invoiced. Other receivables are mainly sales and payroll taxes.

Trade receivables for performance obligations satisfied over time are recognized gradually, as the performance obligation is satisfied and in full once the invoice is due.

Receivables are initially recognized at fair value, and subsequently carried at amortized cost less expected loss allowance. Expected loss allowance is recorded on a portfolio basis. The simplified approach is applied and on initial measurement of receivables, all credit losses expected during the lifetime of the receivables are considered.

Additionally, allowances for individual receivables are recognized if there is objective evidence of credit impairment. Account balances are written off either partially or in full if judged that the likelihood of recovery is remote.

Expected loss allowance and impairments are recognized in the income statement under operating expenses. No security has been received with respect to trade receivables.

For information about how the default risk for trade receivables is analysed and managed, how the loss rates for the provision matrix are determined, how credit impairment is determined and what the criteria for write offs are, see the section on credit risk in note 6.2.

No impairment was recognized for trade receivables in 2021 (2020: 0.0m).

The Group’s exposure to currency and credit risk for trade receivables is disclosed in note 6.2 Risk.

6.2 Risk (extract)

Credit risk

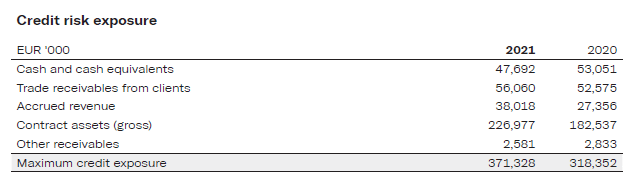

The maximum exposure to credit risk equals the following carrying amounts:

The Group is not exposed to significant risks concerning individual clients or business partners as clients are generally major investment managers in the financial sector. Under the Group’s policy for assuming credit risk, all major clients and other business partners are assessed prior to any contract being signed.

The Group primarily enters financial instruments and transactions with the Group’s relationship banks. Group treasury monitors the Group’s gross credit exposure to banks and operates with individual limits on banks based on rating and access to netting of assets and liabilities.

The main banking relationship is with Nordea Bank and their S&P rating is AA-.

Receivables and contract assets

In assessing expected credit loss of trade receivables and contract assets which comprises many small balances, the Group uses an allowance matrix. Expected loss rates are calculated separately for exposures in different segments based on common credit risk characteristics in relation to geographical region. Two factors are therefore considered when estimating expected loss rates: the actual credit loss experienced over the past seven years and a factor which reflects differences between economic conditions during the period over which the rates were collected, current conditions, and the Group’s view of economic conditions over the expected life of the receivables.

Accumulated average corporate default rates by region as published by Standard & Poor are used as proxy for probability of loss as these provide an indication on counterpart default risk by region of origin. Higher expected loss rates are used for certain balances if individual assessment indicates a higher probability of default. Initially, an expected loss rate from 0.03% up to 2.50% (2020: 0.04% up to 2.89%) is applied for clients with investment grade rating depending on the length of the asset’s lifetime and location.

For unrated clients and clients that do not have investment grade rating, an expected loss rate from 0.36% up to 14.13% (2020: 0.35% up to 13.36%) is applied depending on the length of the asset’s lifetime and the client’s geographical location. A higher rate might be applied to certain clients after individual assessment resulting in the weighted average expected loss rates depicted on the credit risk exposure on receivables and contract assets table.

If there is no reasonable expectation of recovery, the gross carrying amount is written-off. Indicators that there is no reasonable expectation of recovery include, amongst others, the failure of a debtor to engage in repayment plan with the Group, and a failure to make contractual payments for a period greater than three hundred and sixty days past due.

No client represents more than 4.4% (2020: 5.6%) of total receivables from clients.

Expected timing of invoicing for the contract assets balance can be found in note 2.4. The table below depicts information about exposure to credit risk and expected credit loss for trade receivables, accrued revenue and contract assets (gross) on December 31:

1 Includes allowance resulting from individual assessment of outstanding balances.

The expected loss allowance has developed as follows: