Lloyds Banking Group plc – Annual report – 31 December 2020

Industry: banking

Note 3: Critical accounting judgements and estimates (extract)

Regulatory provisions

Key judgements: Determining the scope of reviews required by regulators

The impact of legal decisions that may be relevant to claims received

Key estimates: The number of future complaints

The proportion of complaints that will be upheld

The average cost of redress

At 31 December 2020, the Group carried provisions of £642 million (2019: £2,408 million) against the cost of making redress payments to customers and the related administration costs in connection with historical regulatory breaches.

Determining the amount of the provisions, which represent management’s best estimate of the cost of settling these issues, requires the exercise of significant judgement and estimation. It will often be necessary to form a view on matters which are inherently uncertain, such as the scope of reviews required by regulators, and to estimate the number of future complaints, the extent to which they will be upheld, the average cost of redress and the impact of decisions reached by legal and other review processes that may be relevant to claims received. Consequently the continued appropriateness of the underlying assumptions is reviewed on a regular basis against actual experience and other relevant evidence and adjustments made to the provisions where appropriate.

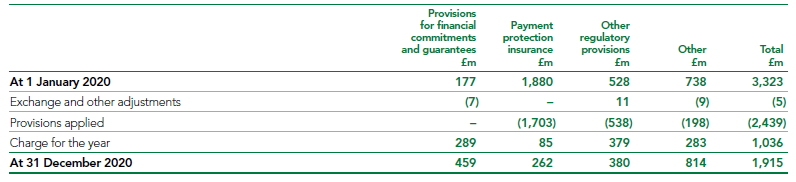

Note 36: Other provisions

Provisions for financial commitments and guarantees

Provisions are recognised for expected credit losses on undrawn loan commitments and financial guarantees. See also note 18.

Payment protection insurance (excluding MBNA)

The Group has made provisions for PPI costs totalling £21,960 million; of which £85 million was recognised in the final quarter of the year ended 31 December 2020. Of the approximately six million enquiries received pre-deadline, more than 99 per cent have now been processed. The £85 million charge in the fourth quarter was driven by the impact of coronavirus delaying operational activities during 2020, the final stages of work to ensure operational completeness ahead of an orderly programme close and final validation of information requests and complaints with third parties that resulted in a limited number of additional complaints to be handled. A small part of the costs incurred during the year also reflect the costs associated with litigation activity to date.

At 31 December 2020, a provision of £201 million remained unutilised relating to complaints and associated administration costs excluding amounts relating to MBNA. Total cash payments were £1,462 million during the year ended 31 December 2020.

Payment protection insurance (MBNA)

As announced in December 2016, the Group’s exposure continues to remain capped at £240 million under the terms of the MBNA sale and purchase agreement. No additional charge has been made by MBNA to its PPI provision in the year ended 31 December 2020; total cash payments in the year were £241 million and the remaining provision at 31 December 2020 was £61 million (31 December 2019: £302 million).

Other provisions for legal actions and regulatory matters

In the course of its business, the Group is engaged in discussions with the PRA, FCA and other UK and overseas regulators and other governmental authorities on a range of matters. The Group also receives complaints in connection with its past conduct and claims brought by or on behalf of current and former employees, customers, investors and other third parties and is subject to legal proceedings and other legal actions. Where significant, provisions are held against the costs expected to be incurred in relation to these matters and matters arising from related internal reviews. During the year ended 31 December 2020 the Group charged a further £379 million in respect of legal actions and other regulatory matters, and the unutilised balance at 31 December 2020 was £380 million (31 December 2019: £528 million). The most significant items are as follows.

HBOS Reading – review

The Group completed its compensation assessment for those within the Customer Review in 2019 with more than £109 million of compensation paid, in addition to £15 million for ex-gratia payments and £6 million for the reimbursement of legal fees. The Group is applying the recommendations from Sir Ross Cranston’s review, issued in December 2019, including a reassessment of direct and consequential losses by an independent panel, an extension of debt relief and a wider definition of de facto directors. Further details of the panel were announced on 3 April 2020 and the panel’s full scope and methodology was published on 7 July 2020. The panel’s stated objective is to consider cases via a non-legalistic and fair process, and to make their decisions in a generous, fair and common-sense manner. Details of an appeal process for the further assessments of debt relief and de facto director status have also been announced. The Group continues to make progress on its assessment of claims for further debt relief and de facto director status, completing preliminary assessments for 98 per cent of claims on both debt relief and de facto directors. As part of these activities the Group has recorded charges in relation to compensation payments and associated costs (projected to the fourth quarter of 2021) in 2020 in applying the recommendations, in respect of debt relief and de facto director status. During 2021, decisions from the independent panel re-review on direct and consequential losses will start to be issued, which is likely to result in further charges but it is not possible to estimate the potential impact at this stage. The Group is committed to implementing Sir Ross’ recommendations in full.

The Dame Linda Dobbs review, which is considering the Group’s handling of HBOS Reading between January 2009 and January 2017, is now expected to complete towards the end of 2021. The cost of undertaking the review is included in the revised provision.

The 2020 charge of £159 million, and lifetime cost of £435 million, includes both compensation payments and operational costs.

Arrears handling related activities

The Group has provided an additional £35 million in the year ended 31 December 2020 for arrears handling related activities, bringing the total provided to date to £1,016 million; the unutilised balance at 31 December 2020 was £62 million.

Customer claims in relation to insurance branch business in Germany

The Group continues to receive claims from customers in Germany relating to policies issued by Clerical Medical Investment Group Limited (subsequently renamed Scottish Widows Limited), with smaller numbers of claims received from customers in Austria and Italy. The German industry-wide issue regarding notification of contractual ‘cooling off’ periods continued to lead to a similar number of claims in 2020 as 2019. The total provision made to 31 December 2020 was £674 million (31 December 2019: £656 million); utilisation of the provision was £28 million in the year ended 31 December 2020 (2019: £28 million); the remaining unutilised provision as at 31 December 2020 was £93 million (31 December 2019: £101 million). The ultimate financial effect, which could be significantly different from the current provision, will be known only once all relevant claims have been resolved.

Other

Following the sale of TSB Banking Group plc, the Group raised a provision of £665 million in relation to various ongoing commitments; £111 million of this provision remained unutilised at 31 December 2020.

Provisions are made for staff and other costs related to Group restructuring initiatives at the point at which the Group becomes committed to the expenditure. At 31 December 2020 provisions of £198 million (31 December 2019: £129 million) were held.

The Group carries provisions of £112 million (2019: £118 million) for indemnities and other matters relating to legacy business disposals in prior years.

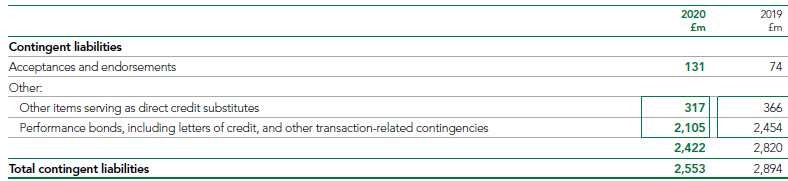

Note 46: Contingent liabilities, commitments and guarantees (extract)

Interchange fees

With respect to multi-lateral interchange fees (MIFs), the Group is not involved in the ongoing litigation which involves card schemes such as Visa and Mastercard (as described below). However, the Group is a member/licensee of Visa and Mastercard and other card schemes. The litigation in question is as follows:

- litigation brought by retailers against both Visa and Mastercard continues in the English Courts (and includes a judgment of the Supreme Court in June 2020 upholding the Court of Appeal’s finding in 2018 that historic interchange arrangements of Mastercard and Visa infringed competition law); and

- litigation brought on behalf of UK consumers in the English Courts against Mastercard, which the Supreme Court has now confirmed can proceed.

Any impact on the Group of the litigation against Visa and Mastercard remains uncertain at this time, such that it is not practicable for the Group to provide an estimate of any potential financial effect. Insofar as Visa is required to pay damages to retailers for interchange fees set prior to June 2016, contractual arrangements to allocate liability have been agreed between various UK banks (including the Group) and Visa Inc, as part of Visa Inc’s acquisition of Visa Europe in 2016. These arrangements cap the maximum amount of liability to which the Group may be subject and this cap is set at the cash consideration received by the Group for the sale of its stake in Visa Europe to Visa Inc in 2016. In 2016, the Group received Visa preference stock as part of the consideration for the sale of its shares in Visa Europe. In 2020, some of these Visa preference shares were converted into Visa Inc Class A common stock (in accordance with the provisions of the Visa Europe sale documentation) and they were subsequently sold by the Group. The sale had no impact on this contingent liability.

LIBOR and other trading rates

Certain Group companies, together with other panel banks, have been named as defendants in private lawsuits, including purported class action suits, in the US in connection with their roles as panel banks contributing to the setting of US Dollar, Japanese Yen and Sterling London Interbank Offered Rate and the Australian BBSW reference rate. Certain of the plaintiffs’ claims have been dismissed by the US Federal Court for the Southern District of New York (subject to appeals).

Certain Group companies are also named as defendants in (i) UK based claims; and (ii) two Dutch class actions, raising LIBOR manipulation allegations. A number of the claims against the Group in relation to the alleged mis-sale of interest rate hedging products also include allegations of LIBOR manipulation.

Furthermore, the Swiss Competition Commission concluded its investigation against Lloyds Bank plc in June 2019. However, the Group continues to respond to litigation arising out of the investigations into submissions made by panel members to the bodies that set LIBOR and various other interbank offered rates.

It is currently not possible to predict the scope and ultimate outcome on the Group of the various outstanding regulatory investigations not encompassed by the settlements, any private lawsuits or any related challenges to the interpretation or validity of any of the Group’s contractual arrangements, including their timing and scale. As such, it is not practicable to provide an estimate of any potential financial effect.

Tax authorities

The Group has an open matter in relation to a claim for group relief of losses incurred in its former Irish banking subsidiary, which ceased trading on 31 December 2010. In 2013, HMRC informed the Group that its interpretation of the UK rules means that the group relief is not available. In 2020, HMRC concluded their enquiry into the matter and issued a closure notice. The Group’s interpretation of the UK rules has not changed and hence it has appealed to the First Tier Tax Tribunal, with a hearing expected in early 2022. If the final determination of the matter by the judicial process is that HMRC’s position is correct, management estimate that this would result in an increase in current tax liabilities of approximately £810 million (including interest) and a reduction in the Group’s deferred tax asset of approximately £270 million. The Group, having taken appropriate advice, does not consider that this is a case where additional tax will ultimately fall due.

There are a number of other open matters on which the Group is in discussions with HMRC (including the tax treatment of certain costs arising from the divestment of TSB Banking Group plc), none of which is expected to have a material impact on the financial position of the Group.

Other legal actions and regulatory matters

In addition, during the ordinary course of business the Group is subject to other complaints and threatened or actual legal proceedings (including class or group action claims) brought by or on behalf of current or former employees, customers, investors or other third parties, as well as legal and regulatory reviews, challenges, investigations and enforcement actions, both in the UK and overseas. All material such matters are periodically reassessed, with the assistance of external professional advisers where appropriate, to determine the likelihood of the Group incurring a liability. In those instances where it is concluded that it is more likely than not that a payment will be made, a provision is established to management’s best estimate of the amount required at the relevant balance sheet date. In some cases it will not be possible to form a view, for example because the facts are unclear or because further time is needed properly to assess the merits of the case, and no provisions are held in relation to such matters. In these circumstances, specific disclosure in relation to a contingent liability will be made where material. However the Group does not currently expect the final outcome of any such case to have a material adverse effect on its financial position, operations or cash flows.

Contingent liabilities, commitments and guarantees arising from the banking business

The contingent liabilities of the Group arise in the normal course of its banking business and it is not practicable to quantify their future financial effect.