LafargeHolcim Ltd – Annual report – 31 December 2015

Industry: construction

- Changes in the scope of consolidation (extract)

4.1 Merger between Holcim and Lafarge

The merger between Holcim and Lafarge announced publicly on April 7, 2014 and structured as a public exchange offer filed by Holcim for all the outstanding shares of Lafarge S.A. with an exchange ratio of nine Holcim Ltd shares for each ten shares of Lafarge S.A., became effective on July 10, 2015. At this date, Holcim Ltd was renamed to LafargeHolcim Ltd.

Exchange offer and merger date

The business combination was accounted for as of July 10, 2015, being the effective date of the merger since LafargeHolcim Ltd controlled Lafarge from that date by owning 87.45 percent of the share capital and at least 84.59 percent of the voting rights of Lafarge S.A. as a result of the public exchange offer. Subsequent to the initial public exchange offer, and in accordance with French regulation, the offer period was re-opened, resulting in LafargeHolcim Ltd holding 278,131,864 Lafarge S.A. shares representing 96.41 percent of the share capital and at least 95.25 percent of the voting rights of Lafarge S.A.. Following the re-opened offer period, the number of LafargeHolcim Ltd shares issued amounted to 250,318,676 shares.

As more than 95 percent of the share capital and voting rights in Lafarge S.A. were tendered, LafargeHolcim Ltd requested the AMF (Autorité des Marchés Financiers) to implement a squeeze-out procedure pursuant to the general regulations of the AMF.

For accounting purposes, the initial public exchange offer and the re-opened public exchange offer are treated as linked transactions and accounted for as one single transaction resulting in LafargeHolcim Ltd holding, and hence consolidating, 96.41 percent of the shares of Lafarge S.A. from the effective date of the merger. As a result, the Group recognized 3.59 percent non-controlling interest for which a squeeze-out procedure was completed in October 2015 as explained further below.

Consideration for the business combination

The consideration calculated on the effective date of the merger amounts to CHF 19,483 million and is detailed in the following table:

Fair value of the LafargeHolcim Ltd shares issued in exchange for Lafarge S.A. shares

The consideration transferred reflects a total of 250,318,676 LafargeHolcim Ltd shares issued as a result of the public exchange offer. The fair value of the shares issued was measured using a LafargeHolcim Ltd share price of CHF 71.55, totaling CHF 17,910 million.

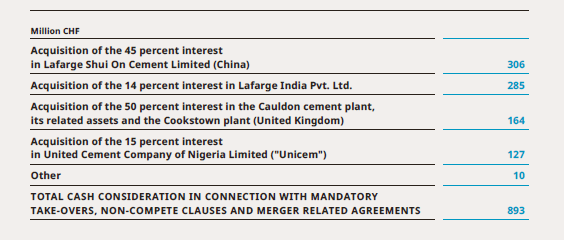

Fair value of the cash consideration in connection with mandatory take-overs, non-compete clauses and merger related agreements

The consideration transferred includes any cash consideration in connection with mandatory take-over, non-compete clauses and merger related agreements. For accounting purposes, the merger and the transactions resulting in these cash considerations are treated as linked and interdependent transactions, accounted for as one single transaction at the effective date of the merger.

The cash consideration reflected in the total consideration transferred includes:

Fair value of previously held interest of Holcim

Prior to the merger, Holcim and Lafarge had an interest of 43.7 percent and 53.7 percent respectively in Lafarge Cement Egypt S.A.E. with Holcim accounting for it as an associate and Lafarge including it as a fully consolidated company. As a result of the merger, LafargeHolcim gained control of Lafarge Cement Egypt S.A.E. through an acquisition in stages. The fair value of Holcim’s previously held equity interest amounts to CHF 464 million resulting in a revaluation gain of CHF 357 million, recorded in the position “Other income” (note 10).

Prior to the merger, Holcim and Lafarge had an equity interest of 42.5 percent and 30.91 percent respectively in the associate company Unicem. As a result of the merger, LafargeHolcim gained control of Unicem through an acquisition in stages. The fair value of Holcim’s previously held equity interest amounts to CHF 216 million resulting in a revaluation gain of CHF 181 million, recorded in the position “Other income” (note 10). The remaining 15 percent interest was acquired by LafargeHolcim in August 2015, as described in the table above.

Adjustment to the consideration recognized in the fourth quarter of 2015

The total consideration for the business combination decreased by CHF 162 million during the fourth quarter of 2015 following the completion of the mandatory take-over procedure for Sichuan Shuangma Cement Company Limited listed shares. As there was no acceptance of this offer, no cash consideration was transferred.

Purchase accounting

For accounting purposes, Holcim has been determined as the accounting acquirer. The acquisition method has been applied. The identifiable assets and liabilities of Lafarge have been fair valued at the effective date of the merger.

The excess of the consideration transferred over the fair value of the Lafarge identifiable net assets is recorded as goodwill.

The recognized amounts of identifiable assets acquired and liabilities assumed as part of the merger are as follows:

The amounts disclosed on the previous page were determined provisionally pending the finalization of the valuation for those assets and liabilities. Up to twelve months from the effective date of the merger, further adjustments may be made to the fair values assigned to the identifiable assets acquired and liabilities assumed, the fair value of the consideration transferred and fair values of Holcim’s previously held equity interests in associates over which control has now been obtained. Hence, the resulting goodwill and its allocation to cash generating units are provisional.

The amounts disclosed above for the assets and liabilities assumed as part of the merger changed to the amounts disclosed in the third quarter 2015. The main change amounts to CHF 485 million for property, plant and equipment and is explained with the refinement of the fair value of terminals and barges.

The fair value of the acquired receivables substantially equals the gross contractual amount to be collected.

The provisional goodwill arising from this transaction amounts to CHF 11,611 million. The goodwill is attributable to the favorable presence of synergies and economies of scale expected from combining the operations of Holcim and Lafarge and to the new, well balanced, global footprint of the combined group. None of the goodwill recognized is expected to be deductible for income tax purposes.

The amount of non-controlling interest recognized amounted to CHF 2,407 million and was measured at the proportionate share of the acquiree’s identifiable net assets at the date of acquisition. The non-controlling interest includes the fair value of Lafarge outstanding stock-options and other equity awards for an amount of CHF 69 million.

Lafarge contributed net sales and net loss of CHF 6,318 million and CHF 321 million respectively to the Group for the period from July 10, 2015 to December 31, 2015. If the acquisition and the related divestments of Lafarge and Holcim businesses had occured on January 1, 2015, net sales and net loss for the year 2015 would have been CHF 29,483 million and CHF 2,085 million respectively.

For the current year, acquisition-related costs of approximately CHF 111 million have been recognized (CHF 42 million included, together with the related net gain on disposal before taxes, in “Other income” and CHF 69 million in “Administration expenses”). The transactions costs for the share issuance and share exchange were recorded in equity for an amount of CHF 56 million.

In 2014, acquisition costs amounted to CHF 67 million and were included in “Administration expenses”.

Acquisition of 3.56 percent non-controlling interest in Lafarge through squeeze-out

Following the re-opened exchange offer, LafargeHolcim Ltd held 278,131,864 Lafarge S.A. shares, representing more than 95 percent of Lafarge S.A. share capital and voting rights. Pursuant to the general regulations of the AMF, LafargeHolcim Ltd initiated on September 14, 2015 a squeeze-out procedure for the shares not owned by LafargeHolcim Ltd. LafargeHolcim Ltd offered the remaining shareholders of Lafarge S.A. a cash indemnification of EUR 60 per each Lafarge S.A. share (net of cost) or as an alternative a share indemnification of 9.45 newly issued LafargeHolcim Ltd shares for 10 Lafarge S.A. shares. The squeeze-out procedure was completed on October 23, 2015 and resulted in a total cash indemnification of CHF 665 million, representing 10,086,921 Lafarge S.A. shares, and the issuance of 633,776 LafargeHolcim Ltd shares. The increase in share capital and authorized capital amounted to CHF 34 million and was recorded against retained earnings. An additional amount of CHF 404 million, being the difference between the total consideration of CHF 699 million and the derecognized non-controlling interest amount of CHF 295 million was recorded in retained earnings as well, leading to a total retained earnings charge of CHF 438 million.

Divestments

LafargeHolcim divested a number of entities and businesses as part of a rebalancing of the global portfolio of the combined group resulting from the merger and to address regulatory concerns. On July 31, 2015, LafargeHolcim disposed of assets to CRH that included operations mainly in Europe, North America and Brazil, followed by assets disposed of in the Philippines on September 15, 2015. The net assets in connection with the acquisition of Lafarge, with a view to resale, were classified as held for sale in the consolidated statement of financial position and as discontinued operations in the consolidated statement of income. The other net assets disposed mainly include property, plant and equipment and long-term liabilities.

The total proceeds amounted to CHF 6.4 billion and resulted in a gain on disposal before taxes of CHF 63 million which is included in “Other income” (note 10). This gain only relates to the disposal of Holcim legacy assets and liabilities as the assets and liabilities of Lafarge were recognized at fair value at the date of acquisition.

In connection with the sale of assets to CRH in 2015, LafargeHolcim has received from CRH several notices claiming a reduction of the purchase price. LafargeHolcim is contesting those claims. In view of the information available to the management and on current analysis, CRH’s claims to a further price reduction under the price adjustment mechanism in the sale agreement are considered to be without merit and are not accepted.