Coats Group plc – Annual report – 31 December 2025

Industry: manufacturing

DIRECTORS’ REPORT (extract)

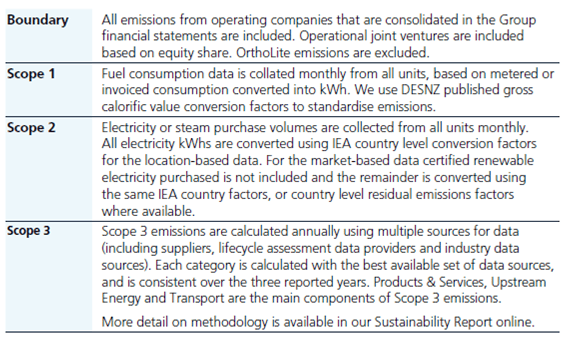

Greenhouse Gas (GHG) Emissions

Absolute emissions for last four years plus 2019 SBTi baseline1

1. All data is calculated following GHG Protocol guidelines.

2. Direct emissions relate to the use of fuels to generate energy on Group facilities, mainly the use of oil and gas to generate heat in the form of steam for use in processing. On-site generation of electricity using diesel or gas fired generators and the use of diesel, petrol and LPG for on-site transport is also included. The calculation methodology here is to convert fuel purchased in each country to kWh and then to CO2e equivalent using DESNZ conversion factors; the data is consolidated globally.

3. Indirect emissions relate mainly to the purchase of electricity from third-party suppliers. This is mostly taken from local electricity grids, but does include some on-site generation of electricity or steam from third-party suppliers. The methodology converts the electricity or other purchased energy from kWh to CO2e using the country level conversion factors published by the International Energy Authority (IEA) for electricity and DESNZ conversion factors for other energy types. This provides the location-based calculation. Market-based calculation deducts any certified renewable energy that is purchased by country and continues to calculate the residue of the energy consumed at the IEA country or DESNZ conversion factors as appropriate. The data is then consolidated globally.

4. Scope 3 value chain emissions cover all other emissions that occur throughout our product and business value chain. This includes the cumulative emissions to produce our raw materials and capital equipment and installations, product and people transport at all stages, downstream processing and consumer use of our sold products and treatment for our waste and our products at the end of their life. The methodology for this varies for each Scope 3 category and follows the GHG Protocol hierarchy of data quality to determine the best available inventory calculation approach. Calculation models are maintained for each individual category and are updated annually as required and consolidated globally.

5. Biogenic emissions cover CO2 emissions that occur from burning bio-mass for the purposes of steam generation. These CO2 emissions are excluded from our reported emissions, however the CH4 and N20 emissions associated with bio-mass are included in our reported.

6. Scope 1 and 2 emissions have been restated for 2019 to 2024 to reflect the sale of Americas yarns and associated Toluca facility closure and transfer of emissions calculations from manual Excel spreadsheet to use of Normative carbon accounting software.

Scope 1 and 2 combined absolute emissions on a market-based approach increase by 42% between 2024 and 2025, however reduced by 30% between 2022 and 2025 versus a 2026 target to deliver a 22% reduction from our 2022 baseline. The increase in Scope 2 market-based emissions in 2025 is due to a regulatory change in Tamil Nadu, India, which has transferred ownership rights of energy attribute certificates (EACs) for offsite wind generated electricity from Coats India to the Tamil Nadu government. Due to this regulatory change, the proportion of our electricity covered by EACs reduced from 74% in 2024 to 62% in 2025, however continues to remain well above our level of 29% in 2022.

We remain ahead of our SBTi 2030 Scopes 1 and 2 emissions reduction, having reduced emissions by 51% from our 2019 baseline. In 2025 we had zero emissions from our UK facilities.

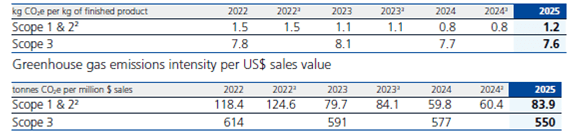

Emissions Intensity1

Greenhouse gas emissions intensity per unit of production

1. We have used these two ratios for several years. The first uses volume of finished goods production in tonnes (Kilo tonnes used for Scopes 1 & 2 are 2025: 107, 2024: 111, 2023: 101, 2022: 117 and hence relates directly to the industrial activity that drives emissions, while the second uses Group turnover and hence relates to overall commercial activity.

2. Figures are calculated on a market basis for Scope 2 emissions.

3. Scope 1 and 2 emissions intensity has been restated for 2022 to 2024 to reflect the sale of the Americas yarns business and associated Toluca facility closure and transfer of emissions calculations from manual Excel spreadsheet to use of Normative carbon accounting software.

Our Scope 1 and 2 volume emissions intensity shows a 47% increase between 2024 and 2025, and a 24% reduction between 2022 and 2025. The increase in 2025 versus 2024 is due to the previously mentioned regulatory change in Tamil Nadu, India.

Scope 3 volume intensity has reduced by 2.4% from 2024 to 2025 and reflects our further positive progress made in transition to non-virgin oil-based materials.

The overall value intensity for Scopes 1 & 2 emissions increased by 39% compared to 2024, with the Scope 3 value intensity reducing by 4.6%.

The difference between the volume and value intensity movements is largely related to movements in price and product mix.

Full details of all reportable greenhouse gas emissions and on the reporting methodology used for the above figures can be found in our online Sustainability Report.

Energy Consumption

1. Energy consumption has been restated for 2022 to 2024 to reflect the sale of the US yarns business and associated Toluca facility closure.

Through 2025 we continued our focus on delivering improvements in energy efficiency, with our smart energy metering programme extended to include structural footwear components sites in China. External energy audits were conducted across a number of key sites. Energy efficiency initiatives focussed on improved use of natural lighting in factories to reduce artificial illumination requirements, use of invertors to optimise efficiency when running electric motors, and optimisation projects on compressed air generation.

Energy consumption in our UK facilities in 2025 was 18MWh and represented 0.003% of global energy consumption.

The following methodology is used for calculating emissions and energy consumption.

TASK FORCE ON CLIMATE-RELATED FINANCIAL DISCLOSURES

Introduction

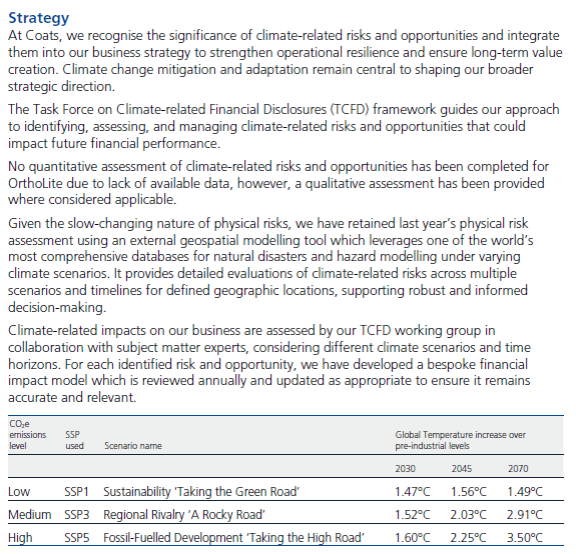

We are pleased to present our 2025 report in response to the Task Force on Climate-related Financial Disclosure (TCFD) recommendations. This report addresses our approach to climate change governance, outlining how Coats integrates climate-related risks and opportunities into the Group’s risk management framework, strategic planning, and decision-making processes. These efforts are aligned with our net zero targets and our transition plan, as detailed on page 195 of this report.

Our TCFD Report outlines how climate considerations are embedded into our risk management, strategic planning and decision making, aligned with our net zero ambition, and we regularly review the financial impacts of our climate related risks and opportunities.

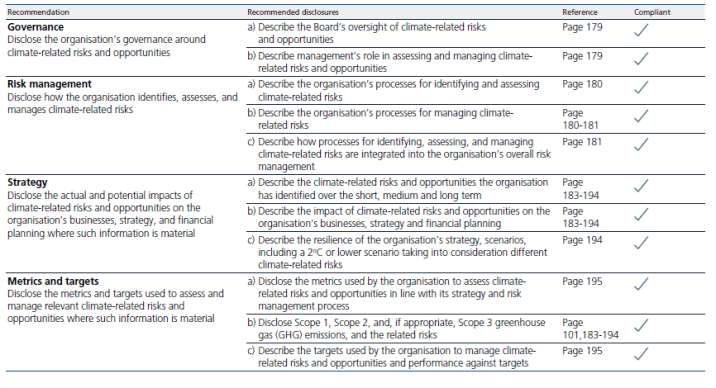

This report covers the four disclosure pillars as detailed in the adjacent table.

Basis of preparation

The report has been prepared with reference to TCFD All Sector Guidance and Supplemental Guidance for Non-Financial Groups.

The Board has noted recommendations in relation to the mandatory disclosures of climate-related financial risk arising from FCA Listing Rule 6.6.6R. In complying with the requirements of the Listing Rule on climate-related disclosures, we consider our disclosure to be consistent with all of the Task Force on Climate-related Financial Disclosures (TCFD) Recommendations and Recommended Disclosures as detailed in ‘Recommendations of the Task Force on Climate-related Financial Disclosures’, 2017, with use of additional guidance from “Implementing the Recommendations of the Task Force on Climate-related Financial Disclosures”, 2021. A quantitative assessment of climate-related risks and opportunities related to the October 2025 acquisition of OrthoLite has not been undertaken; instead, a qualitative assessment of applicable risks and opportunities has been included with further detail provided in the strategy section. A wider assessment of OrthoLite risks and opportunities will be included with our 2026 disclosures.

In this report references are made to other sections in this Annual Report and Accounts (ARA) and in our Sustainability Report (SR). To make it easier to locate these references they are always shown in the following formats: (ARA page X) and (SR page X).

Governance

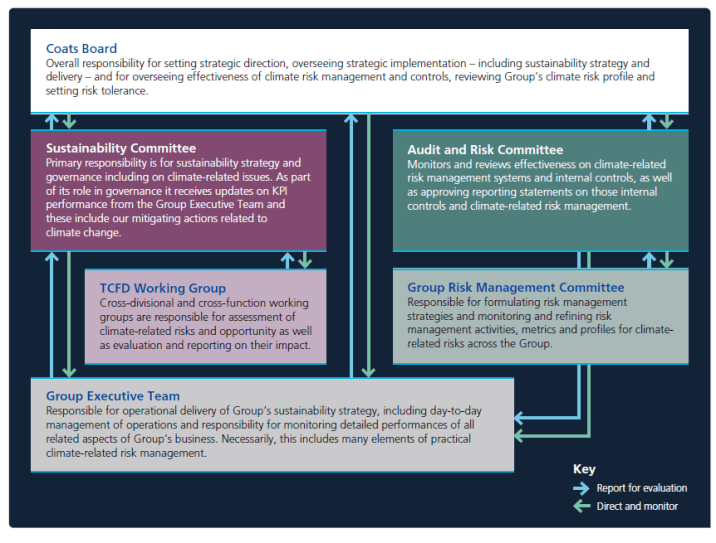

The Board of Directors of Coats oversees and is ultimately responsible for the evaluation of our sustainability strategy, the management of climate-related risks and opportunities, and progress against our sustainability targets, including our interim and long-term net zero targets and net zero transition plan. At management level, the Group Executive Team (GET) is responsible for climate-related deliverables, with the Board receiving regular progress updates during the year (3 updates provided to the Board in 2025). The GET is responsible for operational delivery of the Group’s sustainability strategy, including day-to-day management of operations and responsibility for monitoring detailed performance of all related aspects of the Group’s business, and monitoring of our emission reduction (Scope 1, 2 and 3) plan including costs and investment related to our materials transition strategy.

Two Board sub-committees have important roles to play in managing climate-related risks and opportunities: the Sustainability Committee and the Audit and Risk Committee.

The Sustainability Committee is responsible for the sustainability strategy and governance, including on climate-related issues, and receives updates on KPI performance from the GET including on mitigating actions related to climate change. In 2025, the composition of the Sustainability Committee was reviewed in line with changes to our organisational structure. Reflecting the importance of sustainability to Coats, the Group Chair remains as Chair, and this year our Chief Financial Officer joined the Committee to facilitate greater integration of the financial impacts of climate-related risks and opportunities. Other members include our Group Chief Executive, two Non-Executive Directors, our two Divisional Chief Executives and our Group Sustainability Director. The Audit and Risk Committee monitors and reviews the effectiveness of climate-related risk management systems and relevant internal controls, and approves reporting statements.

In addition, the GET provides updates on the progress of agreed actions directly to the Board, the Sustainability Committee, and the executive Group Risk Management Committee (GRMC) as deemed appropriate. The GRMC is responsible for formulating risk management strategies and monitoring and refining risk management processes and metrics for all risks, including climate-related risks specifically, and convenes on a quarterly basis. The Sustainability Director is responsible for the delivery of climate-related risk assessment work which is reported into the GRMC quarterly as a short update with a full report to the GET annually.

In addition, our cross-divisional and cross-functional TCFD working group (consisting of senior management across areas like finance, procurement and risk) works closely with the Group Sustainability Director who is responsible for assessing the impact of climate risks and opportunities on our business. Monitoring of progress on agreed actions is reported to the GET on a bimonthly basis. The collection of climate-related data for the timely reporting of progress is largely achieved through an internal cloud-based reporting system that collects data from every operating unit on a monthly basis and is reported automatically to multiple internal stakeholders including the GET via dashboards.

The overall governance structure for climate- related risks and opportunities is illustrated in the attached graphic on the next page.

Risk Management

Coats is committed to effectively managing climate-related risks and opportunities that may affect our business, customers, suppliers, and stakeholders.

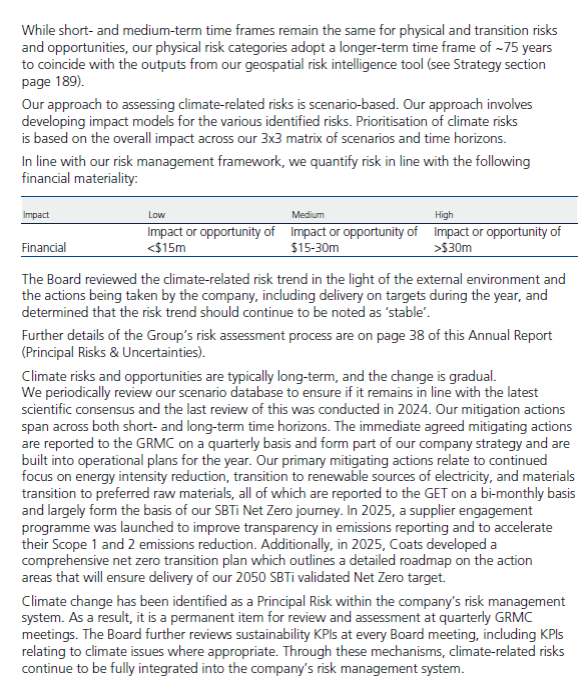

Climate-related risks and opportunities are of strategic, long-term importance to the Group and are assessed and prioritised using the existing Group risk tolerance structure and ensuring integration into the Group risk management framework (see page 44 of this Annual Report).

We assess risks and opportunities across our own operations and value chain, across three climate scenarios and short-, medium-, and long-term time horizons as detailed further in the strategy section of this report.

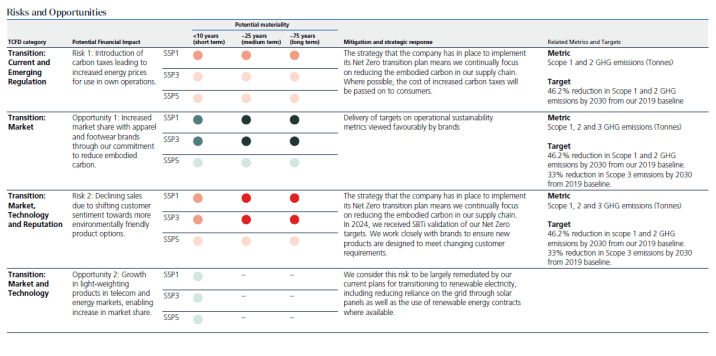

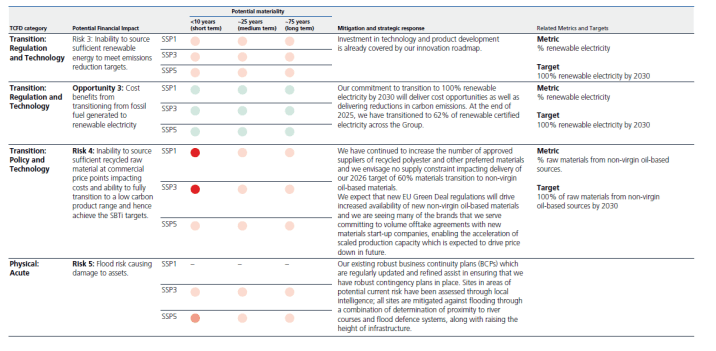

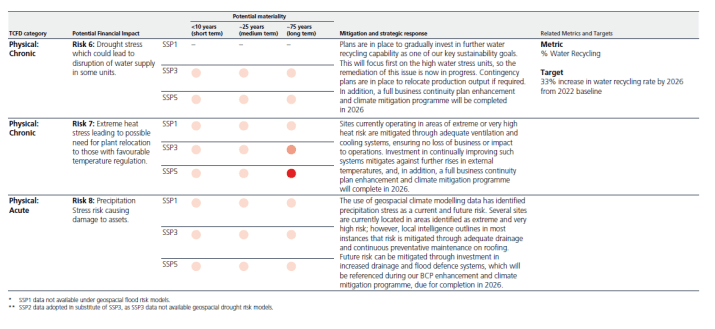

All physical and transition risk categories, as well as current regulatory requirements, are taken into account by Coats when we evaluate the climate-related risks and opportunities that may affect us. We look at how these risks may impact our own operations, or the Group’s upstream and downstream activities, and whether they may first arise in the short- (< 10 years), medium- (~20 years) or long-term (~ 45 years) time frames. These time frames are selected because they correspond roughly to the average remaining life of production assets (short-term), the typical life span of technologies (medium-term) and the possible plant renewal cycle (long-term), as well as aligning to key milestones identified in climate science projections.