Glencore plc – Annual report – 31 December 2016

Industry: mining

- ACQUISITION AND DISPOSAL OF SUBSIDIARIES (extract)

2016 Disposals

In 2016, Glencore disposed of its controlling interest in the Glencore Agricultural products business (“Glencore Agri”), Ernest Henry mining operation (“EHM”) and its New South Wales’ coal rail haulage business (“GRail”).

The carrying value of the assets and liabilities over which control was lost and the net cash received from these disposals are detailed below:

1 Includes a gain of $1,252 million attributable to the remeasurement of the retained Glencore Agri investment to its fair value upon change in control.

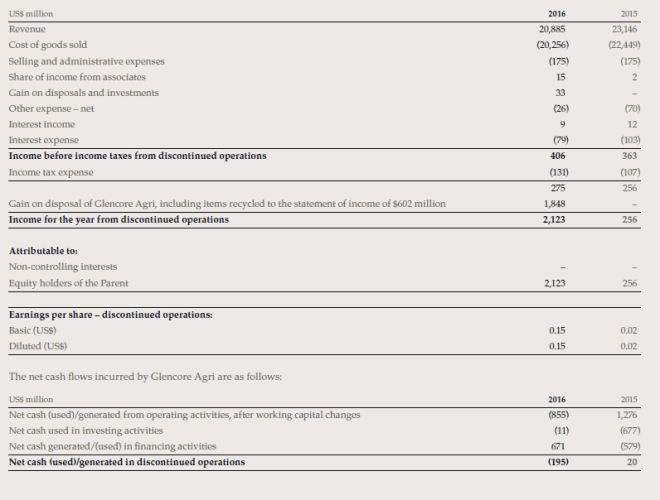

Glencore Agri

On 6 April 2016, Glencore announced that it had entered into an agreement with the Canada Pension Plan Investment Board for the sale of a 40% equity interest in Glencore Agri and on 9 June 2016, entered into an agreement with British Columbia Investment Management Corporation for the sale of a 10% equity interest in Glencore Agri. The aggregate equity consideration for the combined 50% interest, including the indirect assumption of certain levels of net working capital and debt, amounted to $3.125 billion, payable in cash upon closing.

Glencore Agri represents the entire Agricultural products operating segment and was determined to be a discontinued operation prior to the close of transaction on 1 December 2016, and has been disclosed as such. Upon closing of the sale, Glencore is no longer able to unilaterally direct the key strategic, operating and capital decisions of Glencore Agri and was deemed to dispose of its controlling interest at fair value. The difference to the net carrying value was recognised through the statement of income, with Glencore subsequently accounting for its share of the resulting joint venture using the equity method in accordance with IFRS 11 and IAS 28 (see note 9).

The results of Glencore Agri included in the consolidated statement of income until loss of control are detailed below:

EHM

In October 2016, Glencore entered into an agreement with Evolution Mining Limited (“Evolution”), whereby Glencore received $669 million cash in return for a 30% economic interest in the Ernest Henry Mine mining operation (“EHM”) and an entitlement to 100% of the gold produced from Glencore’s remaining 70% interest in EHM. The consideration received was allocated between the two elements of the transaction (sale of the 30% interest and the 70% gold prepaid streaming arrangement) by estimating the fair value of the gold stream by reference to the net present value of the anticipated gold to be delivered over the life of mine ($471 million) with the residual amount representing the consideration for the 30% interest ($198 million). Also see note 19. As part of the transaction, Glencore and Evolution entered into a 70/30 joint venture agreement governing the operations of EHM. As Glencore is no longer able to unilaterally direct the key strategic, operating and capital decisions of EHM, it is deemed to have lost control of EHM and, together with Evolution, jointly controls it. As the new arrangement is an unincorporated joint venture, Glencore derecognised 30% of the identified assets and liabilities of EHM against the proceeds received as noted above.

GRail

In December 2016, Glencore disposed of its New South Wales’ coal rail haulage business to Genesee & Wyoming for cash consideration of $840 million (A$1.1 billion).