Roche Holding Ltd – Annual report – 31 December 2018

Industry: pharmaceuticals

33. Significant accounting policies (extract)

Changes in accounting policies (extract)

‘Definition of a Business’ (Amendments to IFRS 3)

In October 2018 the International Accounting Standards Board issued amendments to IFRS 3 ‘Business Combinations’. The amendments further clarify the definition of a business and add an optional ‘concentration test’ to aid the assessment of whether a transaction represents a business combination or is simply in substance the purchase of a single asset or group of similar assets. These amendments are mandatory from 2020 and may be early adopted. The amendments are particularly relevant for many of the acquisitions carried out by the Group, since the value in the acquired companies often largely consists of the rights to a single product or technology. Therefore, effective 1 January 2018, the Group has early implemented these amendments, with prospective application and with no restatement of comparative period information.

Note 6 has been expanded and renamed as ‘Mergers and acquisitions’ to include both transactions accounted for as business combinations and asset acquisitions. Asset acquisitions are acquisitions of legal entities that do not qualify as business combinations under IFRS 3. Cash consideration paid for asset acquisitions at the transaction date and subsequent additional contingent payments made upon the achievement of performance-related development milestones are now presented in the line ‘Asset acquisitions’ as disclosed in Note 6. Subsequent consideration for performance-related development milestones for transactions treated as asset acquisitions is recognised as intangible assets when the specific milestones have been achieved. Previously intangible assets acquired in asset acquisitions were included in the line items ‘Purchase of intangible assets’ in the statement of cash flows and ‘Additions’ in Note 10 ‘Intangible assets’.

1. General accounting principles (extract)

Key accounting judgements, estimates and assumptions (extract)

Business combinations. The Group initially recognises the fair value of identifiable assets acquired, the liabilities assumed, any non-controlling interest and the consideration transferred in a business combination. Management judgement is particularly involved in the assessment of whether or not the net assets acquired constitute a business and in the recognition and fair value measurement of intellectual property, inventories, contingent liabilities and contingent consideration. In making this assessment, management considers the underlying economic substance of the items concerned in addition to the contractual terms. Management also applies as it considers appropriate the optional ‘concentration test’ as set out in the amendments to IFRS 3 ‘Business Combinations’ published in October 2018 to aid the assessment of whether a transaction represents a business combination or is simply in substance the purchase of a single asset or group of similar assets.

6. Mergers and acquisitions

The Group has implemented the amendments to IFRS 3 ‘Business Combinations’ issued in October 2018. The amendments further clarify the definition of a business. The effect of the amendments is particularly applicable for many of the acquisitions carried out by the Group, since the value in the acquired companies often largely consists of the rights to a single product or technology. From 2018 such transactions will be accounted for as asset acquisitions rather than business combinations. This note has been expanded and renamed as ‘Mergers and acquisitions’ to include both transactions accounted for as business combinations and asset acquisitions. Asset acquisitions are acquisitions of legal entities that do not qualify as business combinations under IFRS 3. Cash consideration paid for asset acquisitions at the transaction date and subsequent additional contingent payments made upon the achievement of performance-related development milestones are now presented in the line ‘Asset acquisitions’ as disclosed separately below. Subsequent consideration for performance-related development milestones for transactions treated as asset acquisitions is recognised as intangible assets when the specific milestones have been achieved. Previously intangible assets acquired in asset acquisitions were included in the line items ‘Purchase of intangible assets’ in the statement of cash flows and ‘Additions’ in Note 10 ‘Intangible assets’. As a result of the amendments to IFRS 3 (see Note 33) the acquisition of Ignyta, Inc. has been reassessed and accounted for as an asset acquisition in these Annual Financial Statements rather than as a business combination as disclosed in the 2018 Interim Financial Statements. This led to a decrease in goodwill of CHF 267 million, a decrease in intangible assets of CHF 103 million and a decrease in deferred tax liabilities of CHF 370 million.

Business combinations – 2018

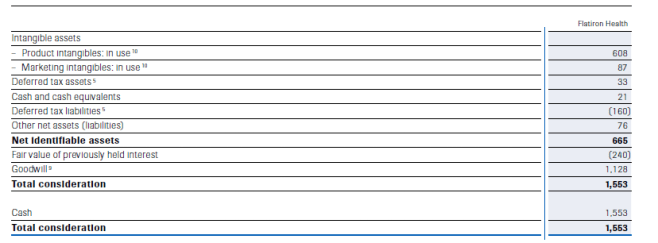

Flatiron Health, Inc. On 5 April 2018 the Group acquired a 100% controlling interest in Flatiron Health, Inc. (‘Flatiron Health’), a privately owned US company based in New York City. Flatiron Health is a market leader in the curation and development of real-world evidence for cancer research as well as in oncology-specific electronic health record software. Flatiron Health is reported in the Pharmaceuticals Division. The total consideration was USD 1,616 million, which was paid in cash.

The identifiable assets acquired and liabilities assumed are set out in the table below.

Business combinations – 2018: net assets acquired in millions of CHF

The fair value of Flatiron Health’s technology platform was determined using an excess earning method that is based on management forecasts and observable market data for discount rates, tax rates and foreign exchange rates. The present value was calculated using a risk-adjusted discount rate of 10.4% for Flatiron Health. The valuation was performed by an independent valuer.

The Flatiron Health accounts receivable is comprised of gross contractual amounts due of CHF 30 million which were all expected to be collectable at the date of the acquisition.

Goodwill represents the value of accelerating progress towards data-driven personalised healthcare in cancer and to advance the use of real-world evidence to set new industry standards for oncology research and development. It also represents a control premium, the acquired work force and expected synergies. None of the goodwill is expected to be deductible for income tax purposes.

The Group recognised a financial gain of CHF 78 million for fair valuing the 12% interest in Flatiron Health held by the Group prior to the transaction. This gain is included in the statement of changes in equity within the line item ‘Net change in fair value – financial assets at fair value through OCI’ in 2018 and has been transferred to ‘Retained earnings’ upon obtaining control.

Directly attributable transaction costs of CHF 3 million were reported in the Pharmaceuticals operating segment within general and administration expenses.

In the nine months to 31 December 2018 Flatiron Health contributed revenue of CHF 56 million and a net loss (after tax) of CHF 175 million to the results reported for the Pharmaceuticals Division and the Group. If the acquisition had occurred on 1 January 2018 management estimates that Flatiron Health would have contributed revenue of CHF 78 million and a net loss (after tax) of CHF 187 million in 2018. This information is provided for illustrative purposes only and is not necessarily indicative of the results of the combined Group that would have occurred had Flatiron Health actually been acquired at the beginning of the year, or indicative of the future results of the combined Group.

Business combinations – 2017

mySugr GmbH. On 29 June 2017 the Group acquired a 100% controlling interest in mySugr GmbH (‘mySugr’), a private company based in Vienna, Austria. mySugr is reported in the Diagnostics operating segment as part of the Diabetes Care business. The total cash consideration was EUR 64 million.

Viewics, Inc. On 27 November 2017 the Group acquired a 100% controlling interest in Viewics, Inc. (‘Viewics’), a privately owned US company based in San Jose, California. Viewics is reported in the Diagnostics operating segment. The total consideration was USD 81 million, of which USD 62 million was paid in cash, USD 9 million was deferred consideration which is being paid over the period from the date of control to 2021 and USD 10 million arose from a contingent consideration arrangement. The contingent payments are based on the achievement of performance-related milestones and the range of undiscounted outcomes is between zero and USD 10 million.

The identifiable assets acquired and liabilities assumed are set out in the table below.

Business combinations – 2017: net assets acquired in millions of CHF

The fair value of the product intangible asset for mySugr is determined using a replacement cost method. The fair value of the other intangible assets is determined using an excess earning method that is based on management forecasts and observable market data for discount rates, tax rates and foreign exchange rates. The present value is calculated using a risk-adjusted discount rate of 13.0% for mySugr and 9.5% for Viewics. The valuations were performed by independent valuers.

Goodwill represents a control premium, the acquired work force and the synergies that can be expected from integrating the acquired companies into the Group’s existing business. None of the goodwill is expected to be deductible for income tax purposes.

The Group recognised a financial gain of CHF 7 million and CHF 2 million respectively for fair valuing the 12% interest in mySugr and the 10% interest in Viewics held by the Group prior to the transaction. This gain is included in other financial income (expense) for 2017.

Directly attributable transaction costs of CHF 2 million were reported in the Diagnostics operating segment within general and administration expenses.

The impact of the mySugr and Viewics acquisitions on the 2017 results for the Diagnostics Division and the Group were not material.

Cash flows from business combinations

Business combinations: net cash outflow in millions of CHF

1) In 2018 directly attributable transaction costs for business combinations amounted to CHF 3 million and are included in the cash flow from operating activities.

Asset acquisitions – 2018

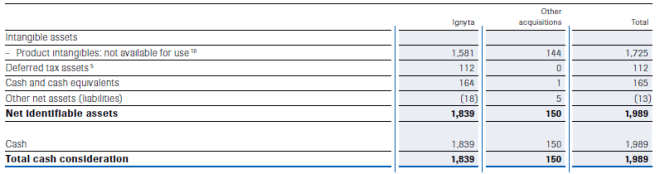

Ignyta, Inc. On 8 February 2018 the Group acquired a 100% controlling interest in Ignyta, Inc. (‘Ignyta’), a publicly owned US company based in San Diego, California, that had been listed on Nasdaq. With the acquisition, the Group obtained rights to Ignyta’s lead product candidate, entrectinib, an orally bioavailable, CNS-active tyrosine kinase inhibitor for patients who have tumours that harbour ROS1 or NTRK fusions. Ignyta is reported in the Pharmaceuticals Division. The total consideration was USD 1,949 million, which was paid in cash.

Other acquisitions. On 27 September 2018 the Group acquired a 100% controlling interest in Tusk Therapeutics Ltd (‘Tusk’), a private company based in Stevenage, United Kingdom. Tusk has developed an antibody with a novel mode of action aimed at depleting regulatory T-cells which suppress immune responses, including those against cancer cells. Tusk is reported in the Pharmaceuticals Division.

On 20 November 2018 the Group acquired a 100% controlling interest in Jecure Therapeutics, Inc. (‘Jecure’), a privately owned US company based in San Diego, California. With the acquisition, the Group obtained rights to Jecure’s preclinical portfolio of NLRP3 inhibitors. Jecure is reported in the Pharmaceuticals Division.

The total cash consideration paid at the acquisition date for both acquisitions was CHF 150 million. Additional contingent payments may be made based upon the achievement of performance-related milestones.

Asset acquisitions – 2018: net assets acquired in millions of CHF

Cash flows from asset acquisitions

Asset acquisitions: net cash outflow in millions of CHF

Foundation Medicine transaction

On 7 April 2015 the Group acquired a 61.3% controlling interest in Foundation Medicine, Inc. (‘FMI’), which has been treated as a fully consolidated subsidiary of the Group since that date. The common stock of FMI was publicly traded and was listed on the Nasdaq under the stock code ‘FMI’. At 31 December 2017 the Group’s interest in FMI was 57.5%.

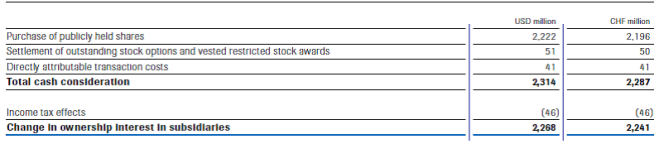

On 18 June 2018 the Group entered into a merger agreement with FMI to acquire the outstanding shares of FMI’s common stock not already owned by the Group at a price of USD 137.00 per share in cash. The merger agreement was approved by the Board of Roche and a special committee of the independent directors of FMI and by its full board of directors. A tender offer was launched on 2 July 2018. On 31 July 2018 the transaction closed and FMI became a 100% owned subsidiary of the Group. It has been accounted for in full as an equity transaction. The cash consideration for the purchase of all public shares, including shares issuable on FMI’s outstanding stock incentive plans and payment of related fees and expenses, amounted to USD 2.3 billion, as set out in the table below. These amounts have been recorded to equity as a change in ownership interest in subsidiaries.

Foundation Medicine transaction