Telia Company AB (publ) – Annual report – 31 December 2024

Industry: telecoms

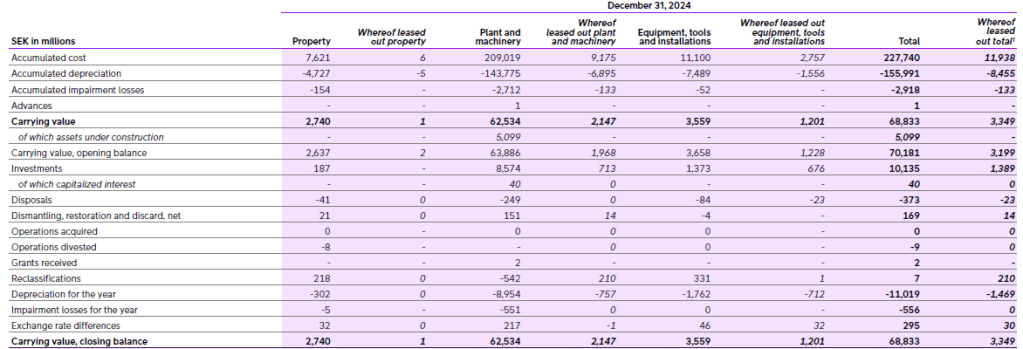

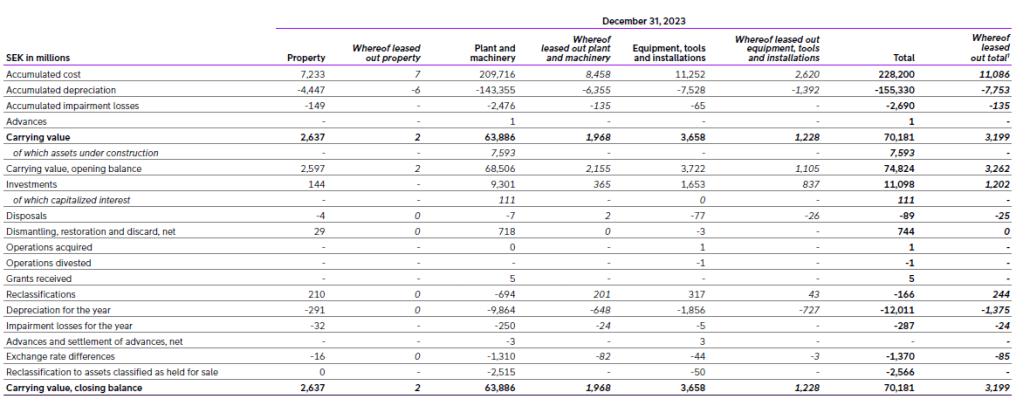

C13. Property, plant and equipment (extract)

The carrying value was distributed and changed as follows.

Disclosures of leased out assets do not include assets which are mainly used in Telia Company’s own operations, and where only a portion of the asset is leased out under an operating lease (mainly network assets).

1) Disclosures of leased out assets do not include assets which are mainly used in Telia Company’s own operations, and where only a portion of the asset is leased out under an operating lease (mainly network assets).