TUI AG – Annual report – 30 September 2025

Industry: Leisure

Principles and Methods underlying the Consolidated Financial Statements (extract)

Key judgements, assumptions and estimates (extract)

Assumptions and estimates (extract)

Assumptions and estimates that may have a material impact on the amounts reported as assets and liabilities in TUI Group are mainly related to the following balance sheet-related facts and circumstances:

- Assumptions for use in impairment tests, in particular for goodwill and property, plant and equipment

- Effect of climate-related risks on the useful lives and the measurement of assets

- Impact of geopolitical risks and uncertainties on measurements of assets

- Determination of the fair values for acquisitions of companies and determination of the useful lives of acquired intangible assets

- Determination of useful lives and residual carrying amounts of property, plant and equipment

- Determination of actuarial assumptions to measure pension obligations

- Recognition and measurement of other provisions

- Determination of the incremental borrowing rate used to measure lease liabilities

- Recoverability of future tax savings from tax losses carried forward and tax-deductible temporary differences

- Measurement of tax risks

- Recoverable amounts of touristic prepayments

- Determination that the package holiday represents a performance obligation due to the significant integration service

- Determination of period-related revenue recognition on a straight-line basis over the duration of the trip

- Determination of the expected credit losses (ECL) of financial instruments

Assumptions for use in impairment tests, in particular for goodwill and property, plant and equipment

The impairment tests are performed on the basis of future discounted cash inflows derived from the medium-term corporate planning. Both the derivation of future cash inflows and the determination of the interest rate are heavily influenced by assumptions and estimates and are associated with uncertainties. In addition assumptions and estimates regarding the financial impact of climate-related risks were made, which are described further below.

The determination of future cash surpluses is based on the following assumptions regarding the development of TUI’s business: In financial year 2025, TUI achieved a further year-on-year increase in customer numbers. Revenue increased by more than 4%, while underlying EBIT grew by more than 9% versus financial year 2024. Further growth in revenues and underlying EBIT is expected for financial year 2026. Growth and cost base reduction are planned through the transformation of the Markets + Airline into an integrated global curated leisure marketplace. Additionally, it is assumed that increased use of online sales channels and especially the app, the provision of dynamic production capacities for flights and accommodation, and investments in digitalization will lead to improved results. In the medium term, an improvement in the adjusted EBIT margin of the Markets + Airline to over 3% is expected. In the Cruises segment, results are expected to rise until the 2028 financial year, particularly due to the expansion of the TUI Cruises fleet. TUI Cruises commissioned a new ship in spring 2025 and will expand its fleet to nine ships (excluding the five ships of the Hapag-Lloyd Cruises brand) by 2026 with the delivery of another vessel. The additional shipbuilding contracts signed on 29 September 2025 will not affect results within the three-year plan, as deliveries are scheduled for 2031 and 2033. In September 2025, Marella Cruises withdraw from its shipbuilding capacities. Accordingly, the impairment assessment for Marella Cruises has been conducted under the premise that the company will continue its operations utilizing the current fleet. Therefore, the future discounted cash flows attributable to the remaining useful life of this fleet are utilized for the purposes of the impairment test. Plans for the Hotels & Resorts segment include further earnings growth through asset-right capacity expansion, for example by management and franchise agreements and in equity companies. Furthermore, investments in own hotels are planned. The development of TUI Musement depends, firstly, on the development of customer numbers in the Markets + Airline sector. Meanwhile, TUI Musement is expected to generate growth by expanding its own and direct distribution, both online and via the app.

Other key factors are the weighted average cost of capital after income taxes (WACC), on which discounting is based, the sustainable growth rate and the growth in perpetuity. Changes in these assumptions may have a significant impact on the recoverable amount and the amount of any impairment loss.

The weighted average cost of capital after income taxes (WACC), on which discounting is based, was derived from external capital market information about comparable companies. The cost of capital to Markets + Airline was increased by an additional risk premium of 2.4% (previous year: 2.4%). This additional risk premium was based on an analysis of internal and external market expectations and reflects the elevated uncertainty with regard to medium- and long-term market developments. Additional country-specific risk premiums are included, in particular, in the measurement of individual hotels. For further details on the determination of WACC refer to the section ‘Goodwill’.

Finally, we have implemented sensitivity analyses to estimate the uncertainty associated with the assumptions on which the impairment tests are based. The sensitivities and their impact on the fair value result exclusively from the adjustment of individual parameters. Possible compensatory measures were not taken into account. Sensitivities have been calculated for changes of the WACC and sustainable growth in perpetuity. In addition, sensitivity analyses have been carried out for a general increase or decrease of future cash flows and for material climate related risks. For further details refer to the section ‘Goodwill’.

Effect of climate -related risks on the useful lives and the measurement of assets

Overview of climate related risks

The tourism industry faces significant impacts from climate change. As temperature rises the attractiveness of certain destinations might decline. Extreme weather events due to climate change might damage our assets and might lead to increased cancellations of holidays. Political and legal developments will increase the expenses for emission certificates and customer preferences might change. Climate change might also present opportunities for TUI, for example extending the touristic season in summer destinations or to diversify to new regions. All these changes will impact the financial performance of TUI and will have a more significant impact long term.

As a result of climate-related risks TUI has committed in 2023 to the Science Based Targets initiative (SBTi) to reduce emissions by 2030 in comparison to a baseline 2019. Our targets are:

- Reduction of CO2e per revenue passenger kilometre by 24% by 2030

- Reduction of absolute CO2e from our cruise operations by 27.5% by 2030

- Reduction of absolute CO2e from TUI Hotels & Resorts by 46.2% by 2030

Furthermore, it is the commitment of TUI to achieve net-zero emissions by 2050. The reduction of emissions will be accomplished with investments in new technologies and the use of fuel with less CO2 emissions.

To assess the impact of climate-related risks on our financial performance and business model TUI has conducted a qualitative and quantitative climate risk assessment in the Financial Year 2023. A number of assumptions underpin this assessment regarding changes to the intensity and frequency of weather related events, technological development, development of energy and emission certificate prices and the development of knowledge on global warming. The assumptions are reviewed and adjusted as necessary. The impact of climate-related risks was assessed for two scenarios, one scenario which implies a global warming of approximately 4.3°C and a scenario which implies a global warming of approximately 1.5°C, both by 2100. The analysis was carried out for the periods up to 2030, 2040 and 2050. The level of uncertainty of the results of the analysis increases over time.

Given the uncertainty TUI has applied critical estimation and judgment in the evaluation of the impact of climate-related risks regarding the recognition and measurement within its financial statements which are described below.

Effect of climate -related risks on the useful lives of assets

The useful lives of assets can be affected by climate-related risks in different ways:

- Physical changes in the climate like an increased frequency and intensity of acute events (storms, fire and floodings) as well as long term trends like increased temperature might impact our assets.

- Transitional changes related to the transition to a low-carbon economy including policy, legal, technology and market changes might affect the use of our assets.

In the assessment of the impact of the climate change on the useful lives of our assets TUI applied the following assumptions and estimates:

The impact of physical risks on our aircraft and our cruise ships is assumed to be low. Both assets could be used flexibly, and itineraries or flight routes could be adjusted. The main risk relates to the commitment of TUI to decarbonize its business. However, all aircraft in the current aircraft fleet have the capability to utilise sustainable aviation fuel (SAF). In addition, the useful lives of our aircraft, which are mainly leased and recognized as right of use assets, end before 2050 so that TUI could replace the aircraft with new technologies such as hydrogen powered aircraft. Likewise, our cruise ships can either already utilise sustainable marine fuel (SMF) or can be converted to do so. Accordingly, TUI concluded that climate-related risks do not affect the useful life of aircraft or cruise ships.

TUI also assessed the useful lives of our hotels in light of climate related risks. Based on the aforementioned analysis TUI concludes that the risk from acute weather events like storms, fire and floodings will increase only to a level which is still manageable through insurance and the large and regional spread of our hotels & resorts portfolio. Furthermore, the increase of these risks will most likely occur in the long term so that our leased hotels with a relatively short useful life are less affected. Based on this analysis TUI concludes that none of our hotels will have a reduced useful life due to sea level rise. The risk for our hotels relating to the decarbonization of our business is assumed to be low as there exists already technology to produce carbon neutral energy for example from renewable sources such as solar panels or wind turbines. The useful lives of our hotels could also be affected by consumer behaviour reacting to e.g. increased temperatures. Certain destinations might see a reduced number of tourists in the long term, especially in the peak season e.g. in summer in the Mediterranean. However, it is assumed that the shoulder seasons in spring and autumn will become broader which will mitigate this effect. In addition, TUI has the ability to steer our customers to our owned Hotels and to manage reduced numbers of guests through reduction in use of 3rd party capacity. Overall, TUI does not see any impact of more climate-related risks on the useful lives of hotels.

Overall useful lives and residual values have not been amended in the previous and reporting year as a result of climate related risks.

Impact of climate -related risks on the measurement of deferred tax assets in relation to losses carried forward

TUI applies a five-year planning horizon derived from its medium-term corporate planning when determining the usability of tax losses carried forward and deductible temporary differences. Medium-term climate-related risks are factored into the measurement of deferred tax assets in relation to losses carried forward. Accordingly, the considerably higher charges that will occur in the long term do not impact the measurement of deferred tax assets in relation to losses carried forward.

Impact of climate -related risks on impairment tests, in particular for goodwill and property, plant and equipment

When performing impairment tests, the discounted future financial charges determined on the basis of the above-mentioned climate-related risk analysis were deducted from the discounted future cash flow surpluses calculated based on our medium-term planning. Due to the long-term nature of these future charges and uncertain technological and regulatory developments, the charges determined in this manner are subject to a high level of uncertainty.

The underlying assumption is that until 2030 TUI will reduce its climate-damaging emissions in accordance with the SBTi and will subsequently follow a linear path to achieving net-zero emissions by 2050. It is likewise assumed that the emissions of our suppliers are reduced for the period up to 2050. These will be achieved in particular by gradually replacing aircraft fuel and bunker oil with fuels that do not cause climate-damaging emissions. The expectation here is that these fuels will be available in sufficient quantities. This assumption depends on the development of technologies and production capacities and is therefore subject to elevated uncertainty. A key estimate concerns price movements for fuels without greenhouse gas emissions. Currently the prices for these fuels are far higher than conventional fuels. In contrast to the previous year, it is now anticipated that the prices for fuels with no greenhouse gas emissions will significantly exceed those of conventional fuels. The prior year’s assumption had been that prices would converge by 2050. This revised expectation is based on the incorporation of various estimates regarding future price developments, as well as procurement experience with such fuels.

Technological innovation, such as in the form of hydrogen-powered aircraft, is not taken into account. Greater fuel efficiency was only considered insofar as it relates to the planned fleet renewal in aviation or else can be achieved by means of known technologies such as underwater coatings on cruise ships. Fleet expansion in the Cruises segment at TUI Cruises has also been factored in. In the segment Hotels & Resorts, it is assumed that emission reductions will be achieved by means of existing and continued investments in renewable energies, such as solar panels.

This reduction in greenhouse gas emissions will be underpinned by a public regulatory framework encompassing everyone, including TUI’s suppliers, leading in particular to a reduction in free emission allowances or an increase in the price of emission certificates. While harmful gas emissions will be reduced in the manner described above, rising prices for emission certificates will generate substantial financial charges before the expenses for emission certificates drop to zero in 2050. The calculation of these financial charges reflects TUI’s own costs, and the costs of emission certificates passed on by suppliers.

In addition, physical risks from climate-related one-off events such as storms or floods or long-term developments such as rising temperatures, affecting the Hotels & Resorts segment, were taken into account. Average annual charges were determined based on external studies. It is expected that the financial impact of these climate-related risks is relatively low.

Overall, the use of low-emission fuels and rising prices for emissions will lead to significant financial charges, particularly for energy-intensive aviation operations in the Northern Region, Western Region, and Central Region segments. The Cruises segment will also be impacted. In Hotels & Resorts segment, the burden will be relatively low; in fact, the autonomous generation of energy, such as by means of solar power, may even generate cost savings.

One key assumption, then, concerns the extent to which costs for low-emission fuels and emission certificates can be passed on to customers. TUI assumes that the reduction in greenhouse gas emissions will generate general price increases (green inflation). TUI additionally benefits from opportunities to pass on costs across the entire value chain. Overall, TUI therefore assumes that it will be able to pass on 90% of the costs in aviation, a sector that is particularly affected, and 95% in other sectors.

In the light of the uncertainties regarding the long-term financial burden from climate-related risks, TUI has calculated sensitivities for the particularly affected Markets + Airline. These are presented in the section on ‘Goodwill’. The sensitivities relate to assumptions on the development of climate-related risks in general, the development of prices for alternative fuels and emission certificates and the potential for passing on climate change-related costs to our customers. Overall, TUI does not regard climate-related risks as a triggering event for carrying out impairment tests.

Impact of geopolitical risks and uncertainties on measurements of assets

Geopolitical risks and uncertainties arising from geo- and economic-political conflicts, pandemics, and natural disaster – such as the Russian war of aggression against Ukraine, armed conflicts in the Middle East, or U.S. trade and tariff policies – may adversely impact TUI’s operating performance and financial position. The asset valuation is based on the following key assumptions:

Crises and wars, for example in the Middle East or Ukraine, may lead to volatility in fuel prices, which directly affects operating costs for our cruise ships and aircraft. A significant portion of the expenditure within the Markets + Airline is denominated in foreign currencies other than the functional currency of the respective unit. Consequently, exchange rate fluctuations and volatile fuel prices caused by geopolitical incidents could have an impact on future net cash inflows. The valuation of the assets of these businesses assumes that TUI’s hedging strategy effectively mitigates the impact of fuel price volatility and foreign exchange risk. For further information on the risk management of TUI see section ‘Financial instruments’.

Subdued macroeconomic growth and inflationary pressures due to geo- and economic-political conflicts may increase price elasticity among customers, a trend further amplified by the transparency of online platforms and artificial intelligence-driven booking platforms. This risk primarily affects the Markets + Airline. As a tour operator, these units typically enter into fixed contractual commitments for flight and hotel capacity prior to the season, creating exposure to underutilization risk or distressed pricing in the event of declining demand. The valuation of the assets of these businesses incorporates the assumption that the accelerated roll-out of dynamic packaging solutions – where TUI does not pre-commit to fixed capacity – as well as the strategic transformation of Markets & Airline into an integrated platform with cross-border capacity allocation will mitigate this risk. For the impairment test of assets within Markets + Airline, a discount rate (WACC) including a risk premium of 2.4% has been applied to reflect amongst others these uncertainties. Sensitivity analyses performed on the goodwill impairment tests for the Northern Region, Western Region, and Central Region did not indicate any impairment (see section ‘Goodwill’).

Geopolitical risks in destinations primarily affect assets within the Hotels & Resorts segment. Political instability or anti-tourism movements may lead to decrease in demand for certain destinations, resulting in lower occupancy rates of hotels. The valuation of assets in Hotels & Resorts assumes that such disruptions are temporary only and therefore have a limited impact on the valuation of hotels held as long-term investments. In addition, TUI can offer hotels in other destinations. Furthermore, TUI retains the flexibility to prioritize its owned hotel portfolio to optimize occupancy and mitigate valuation risk. TUI has implemented emergency response and business continuity plans that minimize operational disruption and reduce risks to our reputation and financial integrity. The board assumes that TUI will maintain destination acceptance through social and environmentally responsible tourism practices and strategic partnerships with local stakeholders. Given the inherent unpredictability of these risks, country-specific risk premiums embedded in the discount rate for individual hotel valuations serve to capture these uncertainties in the impairment assessment.

The impact of natural disasters on assets, particularly within Hotels & Resorts, is assessed as minor due to comprehensive insurance coverage and therefore does not affect the valuation.

Within the Cruises segment geopolitical risks exist comparable to those in Markets + Airline, particularly in relation to fuel price volatility and exchange rate fluctuations. These risks are actively mitigated through TUI’s comprehensive hedging strategy. Local risks, such as natural disasters or regional conflicts, are assessed as having a limited impact, as cruise itineraries and destination ports can be adjusted flexibly in response to such events.

Property, plant and equipment

The measurement of wear-and-tear to property, plant and equipment items entails estimates. The carrying amount of property, plant and equipment as at 30 September 2025 totals €4,133.3m (previous year €3,697.4m). Material assumptions and estimates are the determination of useful lives and residual carrying amounts of property, plant and equipment. The effects of climate-related risks are also taken into account here. From the analysis to review the amounts carried, an evaluation is carried out on a regular basis to assess whether there are any indications of a potential impairment. These indications relate to a number of areas and factors, e.g. the market-related or technical environment but also physical condition. If any such indication exists, management must estimate the recoverable amount on the basis of expected cash flows and appropriate interest rates.

More detailed information on the useful lives and residual values of property, plant and equipment items is provided in the section ‘Property, plant and equipment’ in the section ‘Accounting and measurement methods’.

(12) Goodwill

Goodwill

Disposals of goodwill are attributable to the divestment of several companies. In Central Region, goodwill declined by €0.2m following the sale of the shares in InteRes Gesellschaft für Informationstechnologie mbH. The sale of Ranger Safaris ltd., ARP Africa Travel Ltd. and Pollman’s tours and Safaris Ltd. (ARP group) resulted in the disposal of a part of the goodwill of the ‘Musement’ cash-generating unit (€5.8m). Goodwill disposal in the previous year related to the divestment of the Raiffeisen-Tours RT-Reisen GmbH (Central Region) and of Club Hotel CV SA (Robinson). Detailed information on acquisitions and divestments is provided in the section ‘Acquisitions – divestments’.

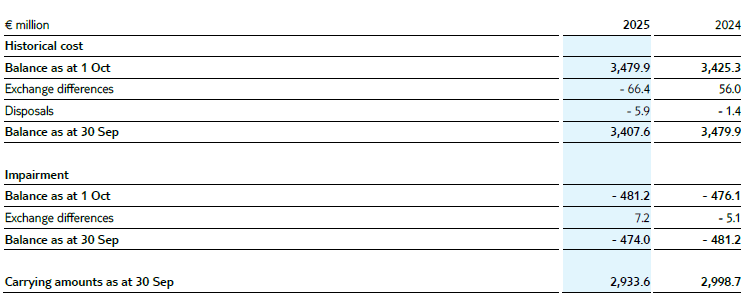

In accordance with the provisions of IAS 21, goodwill allocated to the individual segments and sectors was recognised in the functional currency of the subsidiaries and subsequently translated when preparing the consolidated financial statements. Similar to the treatment of other differences from the translation of annual financial statements of foreign subsidiaries, differences due to exchange rate fluctuations between the exchange rate at the date of acquisition of the subsidiary and the exchange rate at the balance sheet date are taken directly to equity outside profit and loss and disclosed as a separate item. In financial year 2025, an decrease in the carrying amount of goodwill of €59.2m (previous year increase of €50.9m) resulted from foreign exchange differences.

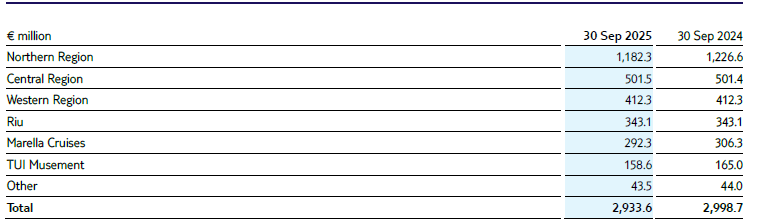

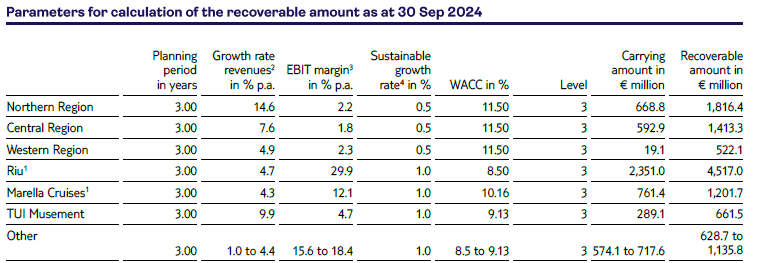

The following table presents a breakdown of goodwill by the significant cash-generating unit (CGU) at carrying amounts. ‘Other’ consists of the two independent cash-generating units, Robinson, and Midnight International (formerly Blue Diamond), which belong to the Hotels & Resorts segment.

Goodwill per cash -generating unit

As at 30 September 2025, an impairment test of capitalised goodwill was performed at the level of cash-generating units. No impairments of capitalised goodwill were identified.

For all CGUs, the recoverable amount was determined on the basis of fair value less costs of disposal, being the higher value compared to the value in use. The fair value was calculated by discounting the expected cashflows. This was based on the medium-term plan for the respective entity as at 30 September 2025. Different from the prior year, the impairment test for Marella Cruises at 30 September 2025 has been prepared under the assumption that future discounted cash flows are derived from the remaining useful life of the existing fleet. Budgeted revenues and EBIT margins are based on expectations of the future business performance. Refer to the section ‘Key judgements, assumptions and estimates’.

The discount rates are calculated as the weighted average cost of capital, taking account of country-specific risks of the CGU and based on external capital market information. In the sector Markets + Airline a risk premium of 2.4% (previous year 2.4%) was added to the cost of capital. For further information refer to ‘Key judgements, assumptions and estimates’. The unchanged high weighted average cost of capital reflects the current market situation.

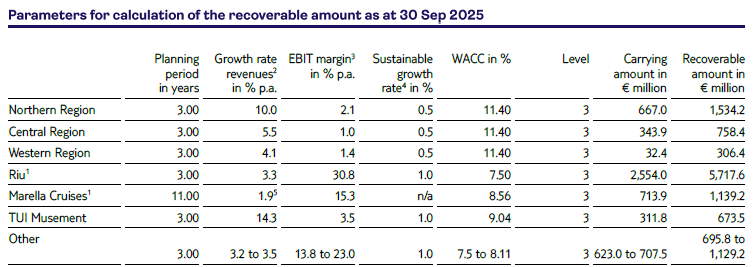

The table below provides an overview of the parameters versus the previous financial year, underlying the determination of the fair values per CGU. As in the previous year, the EBIT margin has been adjusted for deductions of centrally incurred costs. The table lists the CGUs to which goodwill has been allocated:

1 Those are groups of CGUs.

2 Planned growth rate in revenues in % in relation financial year 2028 to financial year 2027

3 EBIT-Margin for financial year 2028 after deduction of centrally incurred costs

4 Growth rate of expected net cash inflows

5 As assumed, revenues will decline by an average of 20% starting in 2031 p.a.

1 Those are groups of CGUs.

2 Planned growth rate in revenues in % in relation financial year 2027 to financial year 2026

3 EBIT-Margin for financial year 2027 after deduction of centrally incurred costs

4 Growth rate of expected net cash inflows

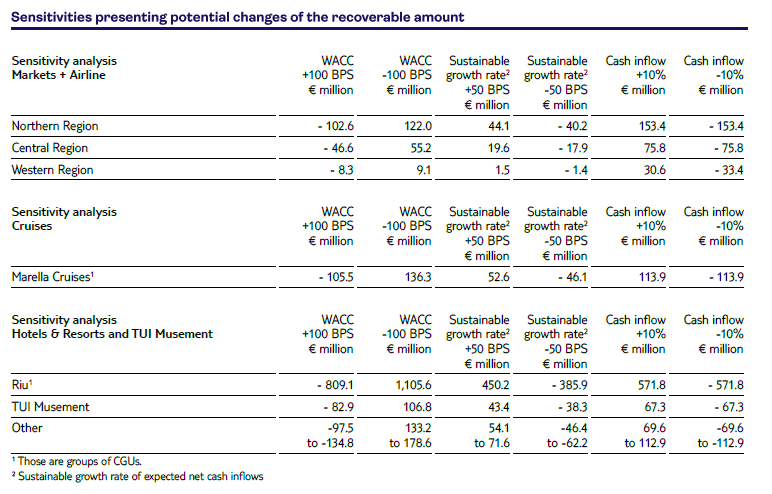

In view of the existing uncertainties regarding future business development, an analysis of sensitivities for the main planning parameters was carried out. In the sector Markets + Airline a risk premium of 2.4% (previous year 2.4%) was added to the cost of capital. For further information refer to ‘Key judgements, assumptions and estimates’. The following table shows the effects of potential deviations in fair value in financial year 2025:

The fair values determined in the sensitivity analysis would have led to an impairment requirement of €24.8m in the CGU Robinson if the WACC had increased by 100 basis points. With the exception of the impairments presented in the Hotels & Resorts segment, the sensitivity analysis did not reveal any further indications of an additional need for impairment losses.

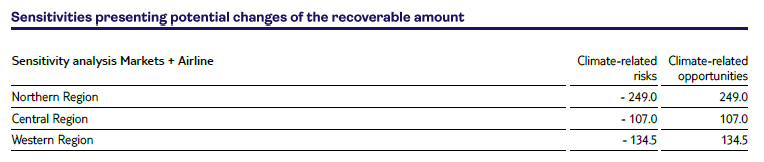

As in the previous year, the financial impact of climate related risks on the business model of TUI was included in the impairment test of capitalised goodwill. The use of low-emission fuels and rising prices for emission certificates will lead to significant financial charges, particularly for energy-intensive aviation operations in the Northern Region, Western Region, and Central Region segments. The Cruises segment will also be impacted. In Hotels & Resorts, the burden will be relatively low; in fact, the autonomous generation of energy, such as by means of solar power, may even generate cost savings. In addition, physical risks from climate-related one-off events such as storms or floods or long-term developments such as rising temperatures, mainly affecting Hotels & Resorts, were taken into account. It is expected that the financial impact of these climate-related risks is relatively low. The financial impact overall is dependent on the degree to which costs can be passed on to customers. For further information on the impact of climate related risks on impairment test refer to the section ‘Key judgements, assumptions and estimates’. The estimation of the financial impact is particularly uncertain with regard to the development of climate related risks, the price development for alternative fuel and emission certificates and the willingness of customers to bear these costs, amongst others. Therefore, sensitivities of climate related risks and opportunities were calculated for especially impacted energy intensive Markets + Airline. In September 2025, Marella Cruises withdraw from its shipbuilding capacities. The impairment test for Marella Cruises has therefore been prepared under the assumption that future discounted cash flows are derived from the remaining useful life of the existing fleet. Given this limited timeframe, climate-related risks are not expected to have a material impact; therefore, no sensitivity analysis has been performed. The sensitivity for climate related risks refers to an increase of climate related costs by 50%. The climate related opportunities relate to a decrease by 50%.

The sensitivity on climate related risk would not have led to an impairment. The following table provides the effects of the sensitivities on the fair value as of 30 September 2025.