Rogers Communications Inc. – Annual report – 31 December 2024

Industry: telecoms

NOTE 6: REVENUE

ACCOUNTING POLICY

Contracts with customers

We record revenue from contracts with customers in accordance with the five steps in IFRS 15, Revenue from contracts with customers, as follows:

- identify the contract with a customer;

- identify the performance obligations in the contract;

- determine the transaction price, which is the total consideration provided by the customer;

- allocate the transaction price among the performance obligations in the contract based on their relative fair values; and

- recognize revenue when the relevant criteria are met for each performance obligation.

Many of our products and services are sold in bundled arrangements (e.g. wireless devices and voice and data services). Items in these arrangements are accounted for as separate performance obligations if the item meets the definition of a distinct good or service. We also determine whether a customer can modify their contract within predefined terms such that we are not able to enforce the transaction price agreed to, but can only contractually enforce a lower amount. In situations such as these, we allocate revenue between performance obligations using the minimum enforceable rights and obligations and any excess amount is recognized as revenue as it is earned.

Revenue for each performance obligation is recognized either over time (e.g. services) or at a point in time (e.g. equipment). For performance obligations satisfied over time, revenue is recognized as the services are provided. These services are typically provided, and thus revenue is typically recognized, on a monthly basis. Revenue for performance obligations satisfied at a point in time is recognized when control of the item (or service) transfers to the customer. Typically, this is when the customer activates the goods (e.g. in the case of a wireless device) or has physical possession of the goods (e.g. other equipment).

The table below summarizes the nature of the various performance obligations in our contracts with customers and when we recognize performance on those obligations.

We also recognize interest revenue on contracts containing significant financing components and on credit card receivables using the effective interest method in accordance with IFRS 9, Financial Instruments.

Payment for Wireless and Cable monthly service fees is typically due 30 days after billing. Payment for Wireless and Cable equipment is typically due either upon receipt of the equipment or over the subsequent 24 months (when equipment is financed through our equipment financing plans). Holders of the Rogers Mastercard have the option to finance devices through Rogers Bank over 36-month or 48-month terms. Payment terms for typical Media performance obligations range from immediate (e.g. Toronto Blue Jays tickets) to 30 days (e.g. advertising contracts).

Contract assets and liabilities

We record a contract asset when we have provided goods and services to our customer but our right to related consideration for the performance obligation is conditional on satisfying other performance obligations. Contract assets primarily relate to our rights to consideration for the transfer of wireless devices. Our long-term contract assets are recognized in “other long-term assets” on our Consolidated Statements of Financial Position.

We record a contract liability when we receive payment from a customer in advance of providing goods and services. This includes subscriber deposits, deposits related to Toronto Blue Jays ticket sales, and amounts subscribers pay for services and subscriptions that will be provided in future periods. Our long-term contract liabilities are recognized in “other long-term liabilities” on our Consolidated Statements of Financial Position.

A portion of our contract liabilities relates to discounts provided to customers on our device financing contracts. Due to the allocation of the transaction price to the performance obligations, the financing receivable we recognize is greater than the related equipment revenue. As a result, we recognize a contract liability simultaneously with the financing receivable and equipment revenue and subsequently reduce the contract liability on a monthly basis.

We account for contract assets and liabilities on a contract-by-contract basis, with each contract presented as either a net contract asset or a net contract liability accordingly.

Deferred commission cost assets

We defer, to the extent recoverable, the incremental costs we incur to obtain or fulfill a contract with a customer and amortize them over their expected period of benefit. These costs include certain commissions paid to internal and external representatives that we believe to be recoverable through the revenue earned from the related contracts. We therefore defer them as deferred commission cost assets in “other assets” and amortize them to “operating costs” over the pattern of the transfer of goods and services to the customer, which ranges from 12 to 90 months. Effective January 1, 2024, as a result of an increase in the customer lifecycle, we updated our amortization period for consumer Wireless and Cable commissions from 24 months to 32 months to better reflect the estimated economic lives of these relationships, which lowered amortization by approximately $115 million for the year.

ESTIMATES

We use estimates in:

- determining the transaction price of our contracts, which requires estimating the amount of revenue we expect to be entitled to for delivering the performance obligations within a contract;

- determining the stand-alone selling price of performance obligations and the allocation of the transaction price between performance obligations; and

- determining the appropriate amortization period of deferred commission cost assets, taking into account the expected pattern of benefits we will receive from the payment of commissions.

Determining the transaction price

The transaction price is the amount of consideration that is enforceable and to which we expect to be entitled in exchange for the goods and services we have promised to our customer. We determine the transaction price by considering the terms of the contract and business practices that are customary within that particular line of business. Discounts, rebates, refunds, credits, price concessions, incentives, penalties, and other similar items are reflected in the transaction price at contract inception.

Determining the stand-alone selling price and the allocation of the transaction price

The transaction price is allocated to performance obligations based on the relative stand-alone selling prices of the distinct goods or services in the contract. The best evidence of a stand-alone selling price is the observable price of a good or service when the entity sells that good or service separately in similar circumstances and to similar customers. If a stand-alone selling price is not directly observable, we estimate the stand-alone selling price taking into account reasonably available information relating to the market conditions, entity-specific factors, and the class of customer.

In determining the stand-alone selling price, we allocate revenue between performance obligations based on expected minimum enforceable amounts to which we are entitled. Any amounts above the minimum enforceable amounts are recognized as revenue as they are earned.

JUDGMENTS

We make significant judgments in determining whether a promise to deliver goods or services is considered distinct and in determining whether our residual value arrangements constitute revenue-generating arrangements or leases.

Distinct goods and services

We make judgments in determining whether a promise to deliver goods or services is considered distinct. We account for individual products and services separately if they are distinct (i.e. if a product or service is separately identifiable from other items in the bundled package and if the customer can benefit from it). The consideration is allocated between separate products and services in a bundle based on their stand-alone selling prices. For distinct items we do not sell separately, we estimate stand-alone selling prices using the adjusted market assessment approach.

Residual value arrangements

Under certain customer offers, we allow customers to defer a component of the device cost until contract termination. We use judgment in determining whether these arrangements constitute revenue-generating arrangements or leases. In making this determination, we use judgment to assess the extent of control over the devices that passes to our customer, including whether the customer has a significant economic incentive at contract inception to return the device at contract termination and to estimate the extent of device returns.

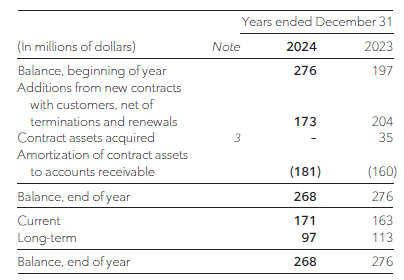

CONTRACT ASSETS

Below is a summary of our contract assets from contracts with customers, net of an allowance for doubtful accounts, and the significant changes in those balances during the years ended December 31, 2024 and 2023.

CONTRACT LIABILITIES

Below is a summary of our contract liabilities from contracts with customers and the significant changes in those balances during the years ended December 31, 2024 and 2023.

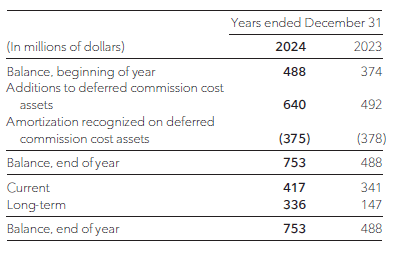

DEFERRED COMMISSION COST ASSETS

Below is a summary of the changes in the deferred commission cost assets recognized from the incremental costs incurred to obtain contracts with customers during the years ended December 31, 2024 and 2023. The deferred commission cost assets are presented within “other current assets” (when they will be amortized into operating costs within one year of the date of the financial statements) or “other long-term assets”.

UNSATISFIED PORTIONS OF PERFORMANCE OBLIGATIONS

The table below shows the revenue we expect to recognize in the future related to unsatisfied or partially satisfied performance obligations as at December 31, 2024. The unsatisfied portion of the transaction price of the performance obligations relates primarily to monthly services; we expect to recognize it substantially over the next three to five years.

We have elected to utilize the following practical expedients and not disclose:

- the unsatisfied portions of performance obligations related to contracts with a duration of one year or less; or

- the unsatisfied portions of performance obligations where the revenue we recognize corresponds with the amount invoiced to the customer.

DISAGGREGATION OF REVENUE