BP p.l.c. – Annual report – 31 December 2022

Industry: oil and gas

1. Significant accounting policies, judgements, estimates and assumptions (extract)

Significant judgement: investment in Aker BP

Judgement is required in assessing the level of control or influence over another entity in which the group holds an interest. For bp, the judgement that the group continues to have significant influence over Aker BP, a Norwegian oil and gas company, following completion of Aker BP’s acquisition of Lundin Energy’s oil and gas business, is significant.

As a consequence of this judgement, bp uses the equity method of accounting for its investment and bp’s share of Aker BP’s oil and natural gas reserves is included in the group’s estimated net proved reserves of equity-accounted entities. If significant influence was not present, the investment would be accounted for as an investment in an equity instrument measured at fair value as described under ‘Financial assets’ below and no share of Aker BP’s oil and natural gas reserves would be reported.

Significant influence is defined in IFRS as the power to participate in the financial and operating policy decisions of the investee but is not control or joint control of those decisions. Significant influence is presumed when an entity owns 20% or more of the voting power of the investee. Significant influence is presumed not to be present when an entity owns less than 20% of the voting power of the investee. IFRS identifies several indicators that may provide evidence of significant influence, including representation on the board of directors of the investee and participation in policy-making processes.

bp owned 27.85% of the voting shares of Aker BP at 31 December 2021 and significant influence was presumed. On completion of Aker BP’s acquisition of Lundin Energy’s oil and gas business on 30 June 2022 , bp’s interest was diluted to 15.9% of the voting shares of Aker BP as a result of new Aker BP shares being issued as partial consideration to Lundin Energy shareholders. bp owned 15.9% of the voting shares at 31 December 2022.

bp’s group chief financial officer, Murray Auchincloss, has been a member of the Aker BP board since 2017. bp’s other nominated director, Kate Thomson has been a member of the Aker BP board since formation of that company in 2016. She is also a member of the Aker BP board’s Audit and Risk Committee. bp also holds the voting rights at general meetings of shareholders conferred by its stake in Aker BP. bp’s management considers, therefore, that the group retained significant influence, as defined by IFRS, over Aker BP following the acquisition of Lundin Energy’s oil and gas business and continues to have significant influence at 31 December 2022.

Significant judgements and estimate: investment in Rosneft

On 27 February 2022, bp announced it will exit its shareholding in Rosneft and bp’s two nominated Rosneft directors both stepped down from Rosneft’s board. As a result, the significant judgement on significant influence over Rosneft was reassessed and a new significant estimate was identified for the fair value of bp’s equity investment in Rosneft. From that date, bp accounts for its interest in Rosneft as a financial asset measured at fair value within ‘Other investments’. Russia has implemented a number of counter-sanctions including restrictions on the divestment of Russian assets by foreign investors. Further, bp is not able to sell its Rosneft shares on the Moscow Stock Exchange and is unable to ascribe probabilities to possible outcomes of any exit process. As a result, it is considered that any measure of fair value, other than $nil, would be subject to such high measurement uncertainty that no estimate would provide useful information even if it were accompanied by a description of the estimate made in producing it and an explanation of the uncertainties that affect the estimate. Accordingly, it is not currently possible to estimate any carrying value other than $nil when determining the measurement of the interest in Rosneft as at 31 December 2022. Events or outcomes within the next financial year, that are different to those outlined above, could materially change the fair value of the investment.

During 2022, Rosneft has held shareholder meetings to approve resolutions to pay dividends. bp did not participate in those meetings. In line with the resolutions, bp would be entitled to dividend income. Russia has imposed restrictions on the payments of dividends to certain foreign shareholders, including those based in the UK, requiring such dividends to be paid in roubles into restricted bank accounts and a requirement for approval of the Russian government for transfers from any such bank accounts out of Russia. Given the restrictions applicable to such accounts, management has made the significant judgement that the criteria for recognizing any dividend income from Rosneft for the year to 31 December 2022 have not been met.

Since the first quarter 2022, bp has also determined that its other businesses with Rosneft within Russia, which are included in the oil production & operations segment also have a fair value of $nil and are subject to similar sanctions and restrictions with respect to the receipt of dividends as described above. Management considers that the criteria for recognizing dividend income from other businesses with Rosneft within Russia that declared a dividend during 2022 have not been met.

The total pre-tax charge during the year-ended 31 December 2022 relating to bp’s investment in Rosneft and other businesses with Rosneft in Russia is $25,520 million.

Significant judgement: formation of Azule Energy

On 1 August 2022, Azule Energy, an independent incorporated 50:50 joint venture, between bp and Eni, was formed through the combination of the two companies’ Angolan businesses. As part of the consideration for contributing its assets, bp received 500,000 shares in Azule Energy. The group determined that the fair value of these shares at the date of the transaction was $6.9 billion and the transaction resulted in a gain on disposal of $3.9 billion, of which 50% has been deferred against the investment on the balance sheet and will be amortised over time, consistent with bp’s accounting policy for unrealized gains on transactions between the group and equity-accounted entities. The fair value was determined using a discounted cash flow analysis with judgments over the assumptions including capital expenditure, costs, production and commodity price forecasts, and a post-tax discount rate that would be applied by a market participant.

17. Investments in associates

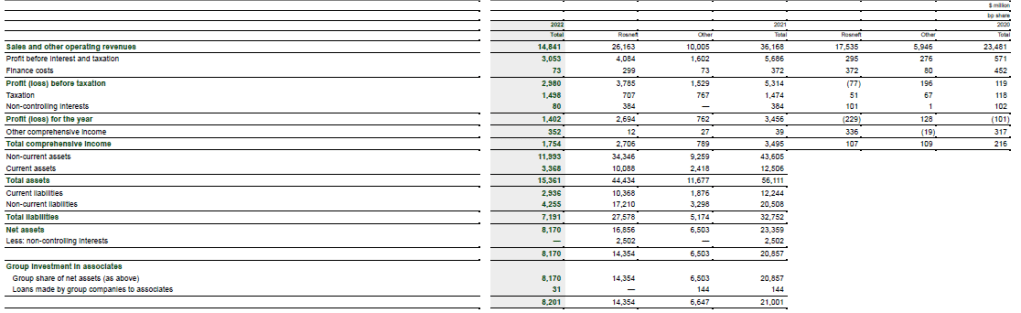

The following table provides aggregated summarized financial information for the group’s associates as it relates to the amounts recognized in the group income statement and on the group balance sheet. There were no individually material associates to the Group at 31 December 2022. The associate which was material to the Group at both 31 December 2021 and 2020 was Rosneft. At 31 December 2021 and 2020 bp classified its investment in Rosneft as an associate because, in management’s judgement, bp had significant influence over Rosneft. On 27 February 2022, bp announced it would exit its shareholding in Rosneft and bp’s two nominated Rosneft directors both stepped down from Rosneft’s board. As a result, the significant judgement on significant influence over Rosneft was reassessed and a new significant estimate was identified for the fair value of bp’s equity investment in Rosneft. From that date, bp accounts for its interest in Rosneft as a financial asset measured at fair value within ‘Other investments’. The total pre-tax charge during the year-ended 31 December 2022 relating to bp’s investment in Rosneft is $24,561 million consisting of $11,082 million included in losses on disposal, primarily relating to the recycling to the income statement of accumulated exchange losses, and a $13,479 million impairment charge including $528 million which relates to estimated earnings in the first two months of the year prior to the loss of significant influence. For further information see Note 1 – Investment in Rosneft and Note 4 Disposals and impairment. As a result of bp’s decision to exit its other businesses with Rosneft in Russia, which were primarily accounted for as investments in associates, an additional impairment charge of $1,043 million including $35 million which relates to estimated earnings in the first two months of the year and accumulated exchange losses of $479 million previously charged to equity have been taken to the income statement. The total pre-tax charge in 2022 relating to bp’s investment in Rosneft and other businesses with Rosneft in Russia is $25,520 million.

The group recognized dividends, net of withholding tax, of $nil from Rosneft in 2022 (2021 $640 million and 2020 $480 million).

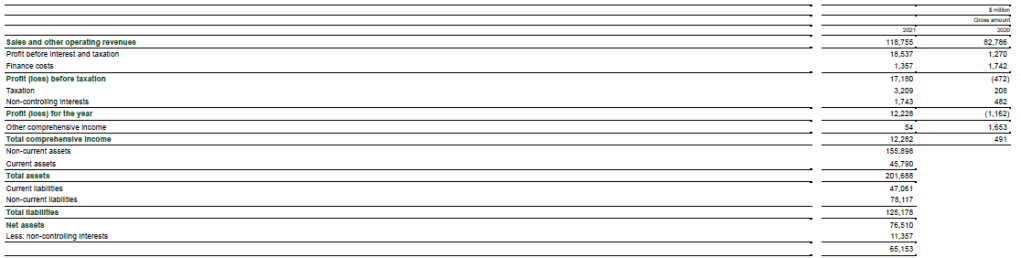

The following table provides summarized financial information relating to Rosneft for 2021 and 2020. This information is presented on a 100% basis and reflects adjustments made by bp to Rosneft’s own results in applying the equity method of accounting. bp adjusted Rosneft’s results for the accounting required under IFRS relating to bp’s purchase of its interest in Rosneft and the amortization of the deferred gain relating to the disposal of bp’s interest in TNK-BP.

Summarized financial information for the group’s share of associates is shown below.

Transactions between the group and its associates are summarized below.

In the normal course of business, bp enters into various arm’s length transactions with associates including fixed price commitments to sell and to purchase commodities, forward sale and purchase contracts and agency agreements.

The terms of the outstanding balances receivable from associates are typically 30 to 45 days. The balances are unsecured and will be settled in cash. There are no significant provisions for doubtful debts relating to these balances and no significant expense recognized in the income statement in respect of bad or doubtful debts. Dividends receivable are not included in the table above.

The majority of purchases from associates in 2022 relate to crude oil and oil products transactions with Aker BP. The majority of purchases from associates in 2021 relate to crude oil and oil products transactions with Rosneft. Sales to associates are related to various entities.

bp has commitments amounting to $8,488 million (2021 $9,930 million), primarily in relation to contracts with its associates for the purchase of transportation capacity. For information on capital commitments in relation to associates see Note 13.

bp’s share of impairment charges taken by associates in 2022 was $nil (2021 $291 million).

13. Capital commitments

Authorized future capital expenditure for property, plant and equipment (excluding right-of-use assets) by group companies for which contracts had been signed at 31 December 2022 amounted to $9,381 million (2021 $8,208 million, 2020 $8,009 million). bp has contracted capital commitments amounting to $1,764 million (2021 $1,075 million, 2020 $1,087 million) in relation to joint ventures and $18 million (2021 $126 million, 2020 $183 million) in relation to associates.

4. Disposals and impairment

The following amounts were recognized in the income statement in respect of disposals and impairments. The impacts of bp’s decision taken on 27 February 2022 to exit its shareholding in Rosneft are included within this note – for further information see Note 1 – Significant judgements and estimate: investment in Rosneft and Note 17 Investments in associates.

Proceeds from disposals of businesses in 2022 includes $669 million relating to the formation of Azule Energy through the combination of bp’s and Eni’s Angolan businesses and $310 million relating to the disposal of bp’s interest in the Sunrise Oil Sands project in Canada. At 31 December 2022, deferred consideration relating to disposals amounted to $191 million receivable within one year (2021 $205 million and 2020 $1,291 million) and $194 million receivable after one year (2021 $823 million and 2020 $2,402 million). The amounts of deferred consideration are reported within Trade and other receivables in Receivables related to disposals in the group balance sheet – see Note 20 for further information. In addition, contingent consideration receivable relating to disposals amounted to $1,896 million at 31 December 2022 (2021 $1,917 million and 2020 $1,999 million). The contingent consideration at 31 December 2022 relates to the prior period disposals of our Alaskan business and certain assets in the North Sea and the disposal of our 50% interest in the Sunrise oil sands project in Canada. These amounts of contingent consideration are reported within Other investments on the group balance sheet – see Note 18 for further information.

Gains and losses on sale of businesses and fixed assets, and closures

gas & low carbon energy

In 2021 gains on disposal of businesses and fixed assets were principally related to a $1,031 million gain on disposal of a 20% participating interest in Block 61 in Oman.

oil production & operations

In 2022 gains principally related to a gain of $1,932 million arising from the contribution of bp’s Angolan business to Azule Energy, a gain of $904 million related to the deemed disposal of 12% of the group’s interest in Aker BP, an associate of bp, following completion of Aker BP’s acquisition of Lundin Energy, and $349 million in relation to the disposal of the group’s interest in the Rumaila field in Iraq to Basra Energy Company, an associate of bp.

Losses included $479 million of accumulated exchange losses previously charged to equity and taken to the income statement as a result of the decision to exit bp’s other businesses with Rosneft within Russia.

In 2021 gains principally resulted from adjustments to disposals in prior periods. Gains include $171 million from the disposal of a 2.1% interest in Aker BP in the North Sea, $100 million from the disposal of certain exploration assets in Brazil, and $502 million fair value movements in relation to deferred and contingent consideration in relation to prior disposals in Alaska and the North Sea.

In 2020, gains principally resulted from adjustments to disposals in prior periods. Gains include $130 million from the disposal of our Alaska operations and interests and $166 million fair value movements in relation to deferred and contingent consideration in relation to the Alaska disposal and prior disposals in the North Sea. Losses included $134 million fair value movements in relation to deferred and contingent consideration arising from prior period disposals in the North Sea, $120 million in relation to the likely disposal of an exploration asset and $78 million from the disposal of certain properties in the US.

customers & products

In 2022, gains principally relate to a gain of $268 million arising from the divestment of our Swiss retail assets. In 2020, gains principally resulted from the $2,300 million gain recognized on the disposal of our Petrochemicals business which completed in December 2020. The gain was adjusted in 2021 as a result of post settlement adjustments. In 2020, losses included $229 million in relation to cessation of manufacturing operations at the Kwinana Refinery following the decision to cease fuel production.

other businesses and corporate

In 2022 the losses on disposal of businesses and fixed assets was $11,082 million in respect of the decision to exit our holding in Rosneft which resulted in the reclassification to the income statement of $10,372 million of accumulated exchange losses, a cash flow hedge reserve of $651 million relating to the original acquisition of Rosneft shares and bp’s cumulative share of Rosneft’s other comprehensive income of $59 million which were all previously charged to equity.

In 2020 the gain on disposal of businesses and fixed assets was principally in respect of the sale and leaseback of our St James’s Square London headquarters.

Summarized financial information relating to the sale of businesses is shown in the table below.

The principal transactions categorized as a business disposal in 2022 were the formation of Azule Energy, the formation of Basra Energy Company and the sale of our 50% interest in the Sunrise oil sands project in Canada.

The principal transaction categorized as a business disposal in 2021 was the sale of a 20% participating interest from bp’s 60% participating interest in Block 61 in Oman.

The principal transactions categorized as a business disposal in 2020 were the sales of our Petrochemical and Alaskan businesses.

Impairments

Impairment losses and impairment reversals in each segment are described below. For information on significant estimates and judgements made in relation to impairments see Impairment of property, plant and equipment, intangibles, goodwill and equity-accounted entities within Note 1. See also Note 12, and Note 15 for further information on impairments by asset category.

gas & low carbon energy

The 2022 impairment loss of $745 million primarily relates to losses incurred in respect of certain assets in Mauritania & Senegal ($729 million) and principally arose as a result of increased forecast future expenditure. The 2022 impairment reversal of $1,333 million primarily relates to the Trinidad CGU ($1,331 million) and principally arose as a result of changes to the group’s oil and gas price assumptions. The recoverable amount of all CGUs for which impairment charges or reversals were recognized in 2022 in total, based on their value in use, is $9,609 million.

The 2021 impairment loss of $834 million primarily relates to losses incurred in respect of certain assets in Mauritania & Senegal ($819 million) and principally arose as a result of increased forecast future expenditure. The 2021 impairment reversal of $2,338 million primarily relates to reversals in respect of producing assets in the KGD6 CGU in India ($1,229 million) and the Trinidad CGU ($600 million) and principally arose as a result of changes to the group’s oil and gas price assumptions and re-assessment of reserves. The recoverable amount of these CGUs on which significant impairment charges or reversals were recognized, based on their value in use, is $7,365 million. The recoverable amount of all CGUs for which impairment charges or reversals were recognized in 2021 in total, based on their value in use, is $17,330 million.

The 2020 impairment loss of $6,214 million primarily relates to losses incurred in respect of producing and development assets in Trinidad ($2,416 million), Mauritania and Senegal ($1,909 million) and India ($1,313 million). Impairment losses were primarily driven by a reduction in bp’s future oil and gas price assumptions and, to a lesser extent, certain technical reserves revisions. The recoverable amount of the impaired CGUs in total was $13,563 million.

oil production & operations

Impairment losses and reversals in all years relate primarily to producing assets and, in 2022, equity accounted investments.

The 2022 impairment loss of $4,480 million primarily relates to impairment of the Pan American Energy Group S.L. joint venture as a result of expected portfolio changes ($2,900 million) and the decision to exit bp’s other businesses with Rosneft within Russia ($1,043 million). The 2022 impairment reversal of $893 million principally relates to changes in price and reserves assumptions in the North Sea ($643 million). The recoverable amount of all CGUs for which impairment charges or reversals were recognized in 2022 in total, based on their value in use, is $7,831 million.

The 2021 impairment loss of $1,617 million principally relates to the decision to exit the Sunrise oil sands project in Canada ($1,109 million). The 2021 impairment reversals of $2,479 million principally arose as a result of changes to the group’s oil and gas price assumptions and re-assessment of reserves. They include amounts in BPX Energy ($1,356 million) and the North Sea ($950 million). The principal CGU on which a significant impairment reversal was recognized was $982 million for Hawkville in BPX Energy. The recoverable amount of these CGUs on which significant impairment charges or reversals were recognized, based on their value in use, is $6,760 million. The recoverable amount of all CGUs for which impairment charges or reversals were recognized in 2021, based on their value in use, is $16,586 million.

The 2020 impairment loss of $6,723 million primarily relates to losses incurred in respect of producing and development assets in the UK North Sea ($2,796 million), the US ($2,744 million), and Canada ($865 million). Impairment losses were primarily driven by a reduction in bp’s future oil and gas price assumptions and, to a lesser extent, certain technical reserves revisions.

customers & products

The 2022 impairment loss of $1,874 million primarily relates to changes in economic assumptions in the Products business including the impairment of the Gelsenkirchen refinery in Germany ($1,366 million), and announced portfolio changes. The recoverable amounts of the CGUs were based on value-in-use calculations. The recoverable amount of all CGUs for which impairment charges or reversals were recognized in 2022 in total, based on their value in use, is $1,648 million.

2021 impairment loss of $962 million principally relates to announced portfolio changes in the products business ($595 million).

2020 impairment loss of $840 million principally relates to portfolio changes in the fuels business, including the conversion of Kwinana refinery to an import terminal. None of the impairment charges were individually material.

Other businesses and corporate

The 2022 impairment loss of $13,536 million arises primarily a result of bp’s decision to exit its shareholding in Rosneft ($13,479 million, including $528 million which relates to estimated earnings in the first two months of the year prior to the loss of significant influence). The recoverable amount of the CGU which comprises Rosneft is estimated to be $nil.

Impairment losses totalling $63 million and $12 million were recognized in 2021 and 2020 respectively.