Tesco PLC – Annual report – 28 February 2026

Industry: retail

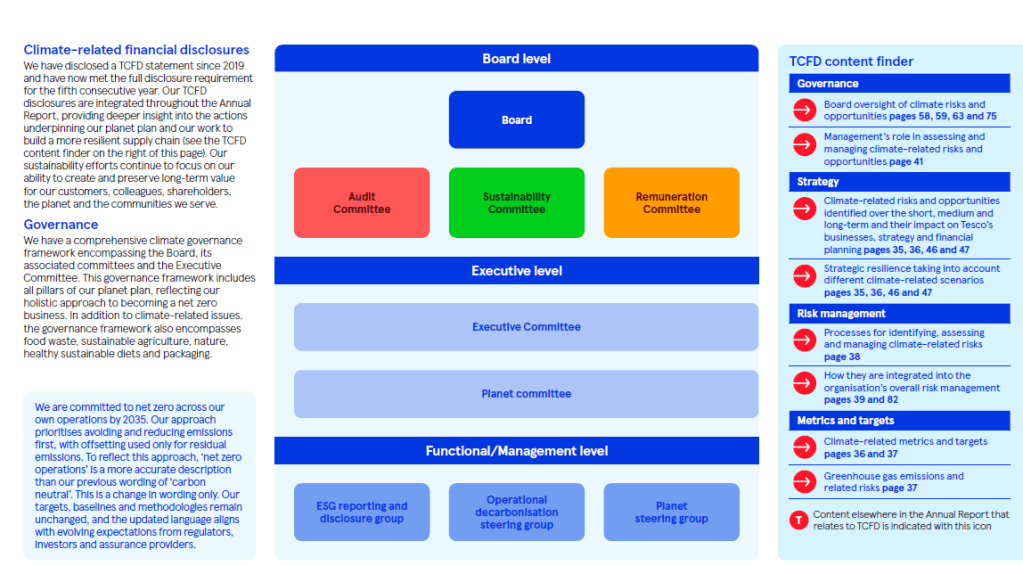

Task Force on Climate-related Financial Disclosures

TCFD

(page 41(extract))

(page 46-47)

TCFD risks and opportunities

Page 45 (extract)

Pages 58-59

Page 75

Sustainability Committee (extract)

Directors’ report (extract)

Streamlined energy and carbon reporting (SECR) disclosures

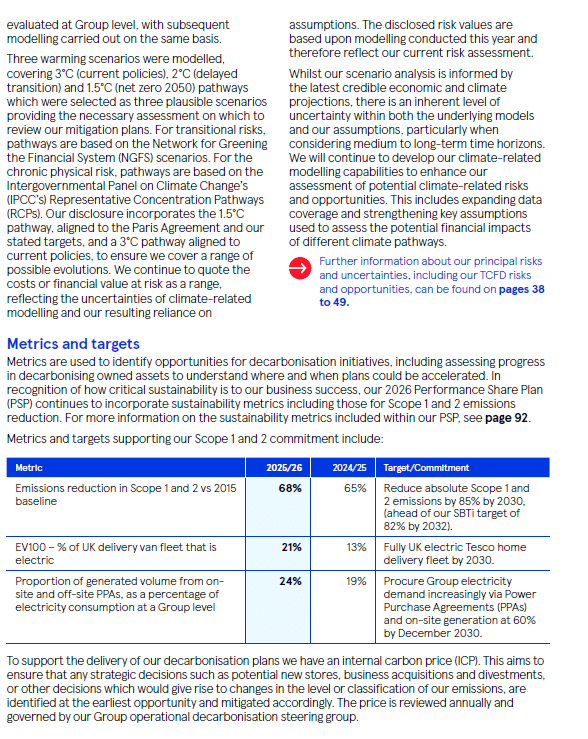

A breakdown of our GHG emissions in accordance with our regulatory obligation to report GHG emissions pursuant to section 7 of the Companies Act 2006 (Strategic report and Directors’ report) Regulations 2013 and the Companies (Directors’ Report), and Limited Liability Partnerships (Energy and Carbon Report) Regulations 2018 can be found on page 37. We continue to implement initiatives to drive energy efficiency across our operations in support of our net zero ambitions.

Examples include:

- Addressing emissions from heating, ventilation and air conditioning (HVAC) by trialling low carbon alternatives to gas boilers;

- Improving refrigeration efficiency and reducing refrigerant emissions in our stores and distribution centres;

- Switching from diesel to electric vans in our UK home delivery fleet;

- Addressing transport emissions associated with our distribution fleet, trialling low-carbon fuels while working directly with manufacturers on long-term decarbonisation solutions such as electric HGVs; and

- Installing electric hook up points for our refrigerated trucks and low-emission refrigeration units powered by electricity.

For further information, see pages 34 to 37.