Deutsche Telekom AG – Annual report – 31 December 2025

Industry: telecoms

Accounting policies (extract)

Net revenue, contract assets and liabilities/contract costs

Revenues include all revenues from the ordinary business activities of Deutsche Telekom. Ordinary activities do not only refer to the core business but also to other recurring sales of goods or rendering of services. However, gains from sales of items of property, plant and equipment or intangible assets are not recognized as revenue but as other operating income. All ancillary income in connection with the delivery of goods and rendering of services in the course of an entity’s ordinary activities is also presented as revenue. Examples include dunning fees, contractual penalties, and default interest. Income from interest added back from long-term customer receivables and contract assets is also considered ancillary income in the course of ordinary activities where the underlying receivables or contract assets have resulted in the recognition of revenue. Revenues are recorded net of value-added tax and other taxes collected from customers that are remitted to governmental authorities. They are recognized in accordance with the provision of goods or services, provided that collectability of the consideration is probable. For service contracts with a continuous service provision, the contractually agreed total consideration is recognized as revenue on a straight-line basis over the minimum contract term, regardless of the payment pattern.

A contract asset must be recognized when Deutsche Telekom recognized revenue for fulfillment of a contractual performance obligation before the customer paid consideration or before – irrespective of when payment is due – the requirements for billing and thus the recognition of a receivable exist.

A contract liability must be recognized when the customer paid consideration or a receivable from the customer is due before Deutsche Telekom fulfilled a contractual performance obligation and thus recognized revenue. In a customer contract, contract liabilities must be set off against contract assets.

Multiple-element arrangements involving the delivery or provision of multiple products or services must be separated into distinct performance obligations, each with its own separate revenue contribution that is recognized as revenue on fulfillment of the obligation to the customer. At Deutsche Telekom, this especially concerns the sale or lease of a mobile handset or other telecommunications equipment combined with the conclusion of a mobile or fixed-network telecommunications contract. The total transaction price of the bundled contract is allocated among the individual performance obligations based on their relative – possibly estimated – standalone selling prices, i.e., based on a ratio of the standalone selling price of each separate element to the aggregated standalone selling prices of the contractual performance obligations. As a result, the revenue to be recognized for products (often delivered in advance) such as mobile handsets that are sold at a subsidized price in combination with a long-term service contract is higher than the amount billed or collected. This leads to the recognition of what is known as a contract asset – a receivable arising from the customer contract that has not yet legally come into existence – in the statement of financial position. The contract asset is reversed and reduced over the remaining minimum contract period, reducing revenue from the other performance obligations (in this case: mobile service revenues) compared with the amounts billed. In contrast to the amounts billed, this results in higher revenue from the sale of goods and merchandise and lower revenue from the provision of services.

Customer activation fees and other advance one-time payments by the customer that do not constitute consideration for a separate performance obligation are deferred as contract liabilities and recognized as revenue over the minimum contract term or, in exceptional cases (e.g., in the case of contracts that can be terminated at any time) over the expected contract period. The same applies to fees for installation and set-up activities that do not have an independent value for the customer.

As distinct from promotional offers, options to purchase additional goods or services free of charge or at a discount are separate performance obligations (material rights) for which part of the revenue is deferred as a contract liability until the option is exercised or expires, providing the discount on future purchases is an implicit component of the consideration for the current contract and is also significant. The measure of significance is whether the decision by the (average) customer to enter into the current contract is likely to have been significantly influenced by their right to the future discount. Offers for volume discounts for the purchase of additional core products of an entity (e.g., a discount offered on an additional fixed-network contract for mobile customers) are considered by Deutsche Telekom as promotional offers for which customers do not (implicitly) pay as part of the current contract.

Long-term customer receivables (e.g., arising from sales of handsets in installments), contract assets (e.g., arising from the subsidized sale of a handset in connection with the conclusion of a long-term customer contract), or contract liabilities (e.g., arising from a prepayment by the customer) are recognized at present value if the financing component is significant in relation to the total contract value (i.e., including those performance obligations that do not contain a financing component). The discount rate also reflects the customer credit risk. Deutsche Telekom makes use of the option not to recognize a significant financing component if the period between when a good or service is transferred to the customer and when the customer pays for that good or service will be one year or less.

Payments to customers including credits or subsequent discounts are recognized as a reduction in revenue unless the payment constitutes consideration for a distinct good or service from the customer, for which the fair value can be reasonably estimated.

Gross vs. net recognition of revenues. In cases where a company is in an intermediary position between another supplier/vendor (e.g., manufacturer, wholesaler) and a customer, it must be assessed whether the company itself supplies the relevant product or provides the service requested by the customer as the principal or whether the company merely acts as the agent for the supplier. The determining factor is control over the specified good or service prior to transfer to the customer. The assessment determines whether the company must recognize revenue on a gross basis (as a principal) or net of the costs incurred to the supplier (as an agent), i.e., only in the amount of the remaining margin. For Deutsche Telekom, the question arises particularly in the case of (branded) digital products (e.g., streaming services, software licenses, cloud-based software as a service) provided by and purchased from third parties and sold to customers as part of Deutsche Telekom’s product portfolio. As a rule, Deutsche Telekom considers itself to be the principal in the aforementioned cases provided the customer does not enter into any contractual relationship with the third-party supplier and Deutsche Telekom bears primary responsibility for product acceptance and customer support, and is in the position to set the sale price.

Contract costs comprise the incremental costs of obtaining a contract (mainly sales commission paid to employees and third-party retailers in the direct and indirect sales channel) and the costs to fulfill a contract. These must be capitalized if it can be assumed that the costs will be compensated by future revenue from the contract. Incremental costs of obtaining a contract are additional costs that would not have been incurred had the contract not been concluded. Costs to fulfill a contract are costs relating directly to a contract that are incurred after contract inception and serve the purpose of fulfilling the contract but are incurred prior to fulfillment and cannot be capitalized under any other IFRS Accounting Standard. Deutsche Telekom makes use of the option to immediately recognize contract costs whose amortization period would not be more than one year as an expense.

The capitalized contract costs are generally recognized on a straight-line basis over the expected contract period. The expenses are disclosed in Deutsche Telekom’s income statement, not under depreciation and amortization but – depending on the sales channel – as goods and services purchased or personnel costs.

In the indirect sales channel, third-party retailers often arrange service contracts on behalf of and for the account of Deutsche Telekom (as the agent) in connection with the sale of subsidized handsets in their own name and for their own account (as the principal). In such cases, the retailers receive commission in an amount that explicitly or implicitly compensates them for the handset subsidy granted. As in the case of multiple-element arrangements in the direct sales channel, the customer ultimately covers the handset subsidy by paying a price above the standalone selling price for the service contract. Deutsche Telekom considers this an implicit promise to the customer that on conclusion of this service contract they will be able to purchase a handset at a discounted price. The only difference between this promise and the purchase of a service in the direct sales channel is that it is not Deutsche Telekom that is granting the discount as part of a multiple-element arrangement but a third-party retailer that is compensated for it by Deutsche Telekom through the commission it receives for arranging the service contract. As, from an economic substance perspective, these payments constitute indirect payments by Deutsche Telekom to customers, the portion of the commission payments attributable to the (implicit) cost reimbursements to the retailer is not deemed to be contract costs but a contract asset and is therefore recognized as a reduction of the service revenues over the contract term rather than as an expense. This ensures that the amount of the service revenues generated with retail customers for identical rate plans does not depend on the type of sales channel.

Depending on the business model, revenue recognition at Deutsche Telekom is as follows:

The mobile and fixed-network business of the Germany, United States, and Europe operating segments includes mobile services, narrow- and broadband access to the fixed network and the internet, television via internet, connection and roaming fees billed to other fixed-network and mobile operators (wholesale business), and sales or lease of mobile handsets, other telecommunications equipment, and accessories, as well as reinsurance for terminal equipment insurance policies and extended warranties offered to mobile customers. Revenue generated from the use of voice and data communications as well as television via internet is recognized upon rendering of the agreed service. The services rendered relate to use by customers (e.g., call minutes), availability over time (e.g., monthly flat rates), or other agreed rate plans. Revenue and expenses associated with the sale of telecommunications equipment and accessories are recognized when the products are delivered, provided there are no unfulfilled company obligations that affect the customer’s final acceptance of the arrangement. Revenue from the lease of mobile handsets and telecommunications equipment that is not considered a sale in economic terms is recognized monthly as the entitlement to the fees accrued. Advertising revenues are recognized in the period in which the advertisements are exhibited.

Trade-in rights for used handsets which are granted to customers upon contract conclusion under the condition of a new purchase transaction (including renewal of an existing service contract) do not constitute repurchase arrangements; however, if the repurchase prices exceed the fair value of the handsets these rights must be recognized as separate performance obligations for which part of the contractual revenue is deferred until they are exercised or expire.

Particularly in the mobile communications business, the timing of payments for mobile handsets purchased in connection with the conclusion of a service contract differs from the timing of the delivery and hence from revenue recognition. Where a significant financing component exists, revenue is measured at the present value. Whereas the sale of subsidized handsets in connection with the conclusion of (long-term) service contracts in the consumer business is still common in the Germany operating segment and also to some extent in the Europe operating segment, handsets are not sold at a discount at all, or only to a limited extent, in the United States operating segment and to some extent in the Europe operating segments; payment-by-installment models or lease models are offered to customers instead. In both the subsidy model and the payment-by-installment model, an asset must thus be recognized at the date of revenue recognition and is generally settled over a 24-month service contract term through payments made by the customer. The only difference is that with the subsidy model it is a contract asset that is repaid through the portion of the monthly bill that exceeds the allocated monthly service revenues. By contrast, the payment-by-installment model involves an existing legal customer receivable that is settled based on an installment plan – separately from the monthly billing for telecommunications services.

The Systems Solutions operating segment provides, among other things, IT services and network services for corporate customers including IT outsourcing services and the sale of hardware including desktop services. Revenue from service contracts is recognized as the service is performed, i.e., normally on a pro rata basis over the contract term. Revenue from service contracts billed on the basis of time and material used is recognized at the contractual hourly rates as labor hours are delivered and direct expenses are incurred.

Revenue from hardware sales or sales-type leases is recognized when the product is shipped to the customer, provided there are no unfulfilled company obligations that affect the customer’s final acceptance of the arrangement. Any costs of these obligations are recognized when the corresponding revenue is recognized.

Revenue from construction contracts and construction-type service contracts (or elements of service contracts), for which a defined output is promised (e.g., IT developments), is recognized using the percentage-of-completion method. The measure of progress or stage of completion of a contract is generally determined as the percentage of cost incurred up until the reporting date relative to the total estimated cost at the reporting date (cost-to-cost method). In particular for complex outsourcing contracts with corporate customers, a reliable estimate of the total cost and therefore of the stage of completion is not possible in many cases, so revenue is only recognized in the amount of the contract costs expensed. This means that a proportionate profit is not realized until the contract has been completed (zero-profit method).

Revenue from non-sales-type rentals and leases is recognized on a straight-line basis over the lease term.

Judgments and estimates (extract)

Revenue recognition, contract assets and liabilities/contract costs

The determination of the transaction price may also be subject to estimates and assumptions, especially in the case of variable consideration, e.g., performance bonuses paid out at the end of a contract. Since their inclusion can lead over time to the recognition of revenue that must be partially reversed in subsequent periods if the conditions for payment are not met, variable payment components can only be included in the transaction price if it is highly probable that there will be an entitlement to payment. Where the variable consideration leads to a reduction in the payment entitlement or a repayment obligation on the part of Deutsche Telekom (e.g., in the case of volume discounts), the fixed contractual payment must be set lower accordingly. In the case of variable discounts, the non-inclusion of the variable consideration means that these as-yet unknown discounts are generally taken into account with a reducing effect on the transaction price.

The standalone selling prices of individual products or services that are part of multiple-element arrangements are complex to determine, because some of the elements are price-sensitive and, thus, volatile in a competitive marketplace. In many cases, standalone selling prices can also not be observed for the company’s own products. Due to the fact that comparability is generally not completely assured, the use of market prices for similar products, e.g., competitor prices, is subject to an element of uncertainty, as is an estimate using a cost-plus-margin approach. Changes in estimates of standalone selling prices can significantly influence the allocation of the transaction price for the entire multiple-element arrangement among the individual performance obligations and therefore affect both the financial position, i.e., the carrying amount of contract assets and contract liabilities, and the current and future results of operations.

One-time payments by the customer for contracts that can be terminated at any time are recognized over an expected contract period, the length of which depends on the period over which, based on the amount of the payment, the customer is expected to renew or not terminate the contract on a monthly basis. As such, the expected contract period is based on a subjective estimate and is therefore not tantamount to a statistically calculated average customer retention period.

Contract costs are deferred and generally recognized as expense over the expected contract period. The estimate of the expected average contract period is based on historical customer turnover. However, this is subject to fluctuations and has only limited informative value with regard to future customer behavior, particularly if new products are rolled out. If management’s estimates are revised, material differences may result in the amount and timing of expenses for subsequent periods.

The significance of material rights is an estimate that is based on both quantitative and qualitative factors. This is ultimately a matter of judgment, even though it is supported by quantitative facts. Depending on the decision as to whether or not the customer has a material right to be deferred, there may be material differences in the amount and timing of revenues for the current and subsequent periods.

3 Contract assets

The carrying amount of contract assets increased by EUR 0.4 billion against December 31, 2024 to EUR 3.1 billion. Contract assets relate to receivables that have not yet legally come into existence, which arise from the earlier – as compared to billing – recognition of revenue, in particular from the sale of goods and merchandise under long-term multiple-element arrangements (e.g., mobile contract plus handset). Receivables from long-term construction contracts are also recognized under contract assets. Of the total contract assets, EUR 0.4 billion related to contract assets in connection with long-term construction contracts (December 31, 2024: EUR 0.2 billion).

The increase in the carrying amount was mainly due to higher contract assets in the United States operating segment, with EUR 0.5 billion of the increase due to growth in business models in the consumer and business customer areas in the United States, in which discounts are granted on handset sales on the condition of a minimum service contract term. By contrast, exchange rate effects, primarily from the translation from U.S. dollars into euros, decreased the carrying amount.

For information on allowances of contract assets, please refer to Note 43 “Financial instruments and risk management.”

9 Capitalized contract costs

As of December 31, 2025, the carrying amount of capitalized contract costs stood at EUR 3.9 billion and was thus EUR 0.3 billion higher than at the end of the prior year. This increase was attributable in particular to a higher level of capitalized costs of obtaining a contract in postpaid customer business in the United States, Germany, and Europe operating segments. The costs of obtaining a contract mainly include sales commissions paid to employees and third-party retailers in the direct and indirect sales channel. By contrast, exchange rate effects, primarily from the translation from U.S. dollars into euros, decreased the carrying amount.

Overall, capitalized contract costs of EUR 2.9 billion (2024: EUR 2.9 billion) were written down on a straight-line basis over the estimated customer retention period.

18 Contract liabilities

The carrying amount of current and non-current contract liabilities increased year-on-year by EUR 0.2 billion to EUR 3.6 billion. These substantially include deferred revenues. In the United States operating segment, contract liabilities increased by EUR 0.2 billion, mainly in due to effects of changes in the composition of the Group in connection with the UScellular Acquisition. By contrast, exchange rate effects, primarily from the translation from U.S. dollars into euros, decreased the carrying amount. In the Germany operating segment, the carrying amounts decreased by EUR 0.1 billion year-on-year.

Revenue of EUR 2,182 million (January 1, 2024: EUR 1,754 million) from contract liabilities that were still outstanding as of January 1, 2025 was realized in the reporting year. The figure for 2024 has been adjusted retrospectively. Of the total of contract liabilities, EUR 2,572 million (December 31, 2024: EUR 2,378 million) is due within one year.

For further information on the UScellular Acquisition, please refer to the section “Changes in the composition of the Group and other transactions” under “Summary of accounting policies.”

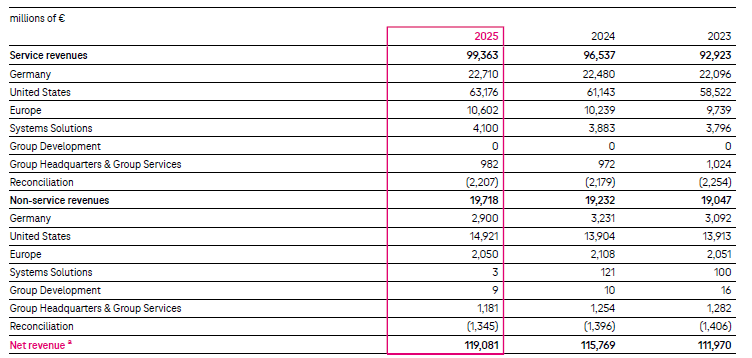

20 Net revenue

Net revenue breaks down into the following revenue categories:

a Revenue includes interest income of EUR 738 million in the reporting year, calculated using the effective interest method (2024: EUR 658 million; 2023: EUR 662 million). This income is primarily attributable to accrued interest on receivables in connection with handsets sold under installment plans in the United States operating segment.

The service revenues essentially comprise predictable and/or recurring revenues from Deutsche Telekom’s core activities. These relate to revenues that are generated from services (i.e., revenues from fixed and mobile network voice services, incoming and outgoing calls, as well as data services) plus roaming revenues, monthly basic charges and visitor revenues, as well as revenues from the ICT business. Service revenue also includes revenues earned in connection with premium services for customers, such as reinsurance for device insurance policies and extended warranties. Revenue from insurance contracts in the scope of IFRS 17 in the Group amounted to EUR 4.3 billion (2024: EUR 4.6 billion; 2023: EUR 4.5 billion).

Non-service revenues mainly comprise one-time and variable revenues, e.g., revenue from the sale or rental of fixed-network or mobile devices, from value-added services, from application and contract services, revenue with virtual network operators, one-time revenue from the build-out of technical infrastructure, and revenue from vehicle and property leasing.

Net revenue includes revenue from the use of entity assets by others in the scope of IFRS 16 in the amount of EUR 0.7 billion (2024: EUR 0.9 billion; 2023: EUR 1.1 billion). Of the revenue from the use of entity assets by others reported in net revenue, EUR 0.6 billion (2024: EUR 0.7 billion; 2023: EUR 0.7 billion) relates to service revenues and EUR 0.1 billion (2024: EUR 0.2 billion; 2023: EUR 0.4 billion) to non-service revenues.

Net revenue for the reporting year was EUR 119.1 billion, up EUR 3.3 billion on the prior-year level. In the Germany operating segment, revenue declined by 0.4 % year-on-year, mainly due to lower mobile terminal equipment revenues. By contrast, service revenues increased in the mobile and fixed-network business. In the United States operating segment, revenue was up 4.1 % against the prior-year level, which was attributable to higher service and terminal equipment revenue. In the Europe operating segment, revenue increased by 2.5 % year-on-year, primarily due to the increase in services revenues in the mobile, fixed-network, and IT business. Revenue in the Systems Solutions operating segment was up 2.5 % year-on-year, mainly due to growth in the Digital and Road Charging areas.

For information on changes in net revenue, please refer to the section “Development of business in the Group” in the combined management report.

The total transaction price attributable to performance obligations that have (partially) not been fulfilled (hereinafter: outstanding transaction price) amounts to EUR 23.7 billion (2024: EUR 22.7 billion, 2023: EUR 23.4 billion).

The portion of the outstanding transaction price attributable to performance obligations that have not been fulfilled or not yet completely fulfilled at the end of the reporting year is generally recognized as revenue over the remaining term of the service contracts concluded. Since most service contracts – unless they can be canceled at any time – have a minimum contract term of 24 months, an average remaining term of approximately 12 months can be assumed, provided the course of business in the mass market business remains virtually unchanged. The disclosures only refer to transactions within the scope of IFRS 15, i.e., they do not include portions of the transaction price being allocated to performance obligations outside the scope of this standard, e.g., leases.

Deutsche Telekom generally makes use of the practical expedients in IFRS 15, according to which outstanding performance obligations under contracts with an expected original term of no more than one year and revenues recognized in accordance with the billed amounts are exempt from the disclosure requirement. Individual subsidiaries deviate from this general approach and have not made use of these practical expedients for groups of contracts with similar characteristics.

Service concession arrangements

Satellic NV, Machelen, Belgium, is a fully consolidated subsidiary of Deutsche Telekom and on July 25, 2014 signed a contractual arrangement with Viapass, the public agency responsible for toll collection in Belgium, for the set-up, operation, and financing of an electronic toll collection system. After Viapass accepted the system on March 30, 2016, the set-up phase was completed on March 31, 2016. The subsequent operation phase has a duration of 12 years, with the additional option for Viapass to extend the term three times by 1 year. Satellic has no entitlement to the toll revenue collected but receives contractually agreed fees for setting up and operating the system. Viapass is authorized to terminate the arrangement giving notice of six months with payment of reasonable compensation. In the event of regular or premature termination of the agreement, Satellic has an obligation to hand over to Viapass, on request, material assets for the operation of the toll collection system that have not yet passed to the ownership of Viapass; in such an event, however, the software platform for toll collection would not be handed over to Viapass. The agreement was classified as a service concession arrangement within the meaning of IFRIC 12. Since the start of the operation phase on April 1, 2016, the separate fees for operation and maintenance services have been recognized as revenue in the respective periods, which totaled EUR 82 million in the reporting year (2024: EUR 89 million; 2023: EUR 94 million).