Sime Darby Berhad – Annual report – 30 June 2017

Industry: conglomerate

2 Basis of Preparation (extract)

The financial statements of the Group and of the Company are prepared in accordance with the provisions of the Companies Act, 2016 and comply with the Malaysian Financial Reporting Standards (MFRS) and International Financial Reporting Standards (IFRS).

The financial statements of the Group and of the Company for the financial year ended 30 June 2017 are the first set of financial statements prepared in accordance with the MFRS, including MFRS 1 – First-time Adoption of Malaysian Financial Reporting Standards and MFRS 141 – Agriculture. Subject to certain transition elections as disclosed in Note 58, the Group and the Company have consistently applied the same accounting policies in their opening MFRS statements of financial position as at 1 July 2015, being the transition date, and throughout all years presented, as if these policies had always been in effect. The impact of the transition to MFRS on the Group’s and the Company’s reported financial position, financial performance and cash flows, are disclosed in Note 58.

STATEMENTS OF FINANCIAL POSITION

As at 30 June 2017

Amounts in RM million unless otherwise stated

58 First-time Adoption of MFRS Framework and Early Adoption of MFRS 15

a. Transition from Financial Reporting Standards Framework (FRS) to MFRS

The financial statements of the Group and of the Company for the financial year ended 30 June 2017 are the first sets of the financial statements prepared in accordance with MFRSs.

The Company, in its consolidated financial statements, measured the assets and liabilities of subsidiaries at the same carrying amounts as in the financial statements of those subsidiaries that have adopted the MFRS framework or IFRS earlier than the Company, after adjusting for consolidation adjustments. During the financial year, certain subsidiaries which have adopted the IFRS earlier than the Company changed its accounting policy on deferred tax liabilities on indefinite useful life intangible assets in light of the IFRIC agenda decision. The change in accounting policy has been applied retrospectively and has resulted in additional goodwill and deferred tax liabilities by RM200 million and RM207 million at 1 July 2015 and 30 June 2016, respectively. The Group has reflected these impacts in its consolidated financial statements accordingly.

As provided in MFRS 1, first-time adoption of MFRS can elect optional exemptions from full retrospective application of MFRSs. The Group has elected to apply MFRS 3 – Business Combinations prospectively from the date FRS 3 – Business Combinations was adopted and to deem the carrying amount of investment in each subsidiary, joint venture and associate to be the cost of the investment in the separate financial statements as at the date of transition to MFRSs. The optional exemptions elected by the Group that have an impact on the reported financial positions prepared in accordance with FRSs are disclosed in Note 58(a)(i), (ii) and (iii).

The accounting policies set out in Note 3 and the following optional exemptions elected by the Group have been applied in the opening MFRS statement of financial position as at 1 July 2015 and throughout all periods presented in the financial statements.

Except for a reclassification of merger reserve of RM5,725 million to retained profit as at 1 July 2015, the transition to MFRSs does not impact the financial statements of the Company. The effect of the Group’s transition to MFRSs are as follows:

i. Property, plant and equipment – Deemed cost exemption

Under FRS, valuation adjustments on certain plantation land and building were incorporated into the financial statements. The Group have elected to use the previous revaluation as deemed cost under MFRSs. The revaluation reserve of RM67 million as at 1 July 2015 was reclassified to retained earnings.

ii. Exemption for cumulative translation differences

The Group have elected to reset the exchange reserve to zero. The exchange reserve of RM634 million as at 1 July 2015 was reclassified to retained earnings.

iii. Effects of MFRS 141

Prior to the adoption of MFRS 141 and Agriculture: Bearer Plants (Amendments to MFRS 116 and MFRS 141), produce growing on bearer plants were not recognised and livestock were stated at cost. Following the adoption, these biological assets are measured at fair value less costs to sell. Changes in fair value less costs to sell are recognised in profit or loss.

b. Early Adoption of MFRS 15

With the adoption of MFRS 15, revenue is recognised by reference to each distinct performance obligation in the contract with customer. Transaction price is allocated to each performance obligation on the basis of the relative standalone selling prices of each distinct good or services promised in the contract. Depending on the substance of the contract, revenue is recognised when the performance obligation is satisfied, which may be at a point in time or over time.

In applying MFRS 15 retrospectively, the Group applied the following practical expedients

i. for completed contracts, contracts that begin and end within the same annual reporting period were not restated;

ii. for completed contracts that have variable consideration, rather than estimating variable consideration amounts in the comparative reporting periods, transaction price at the date the contract was completed was used; and

iii. for all reporting period presented before the date of initial application, the amount of the transaction price allocated to the remaining performance obligations and an explanation of when the revenue is expected to be recognised are not disclosed.

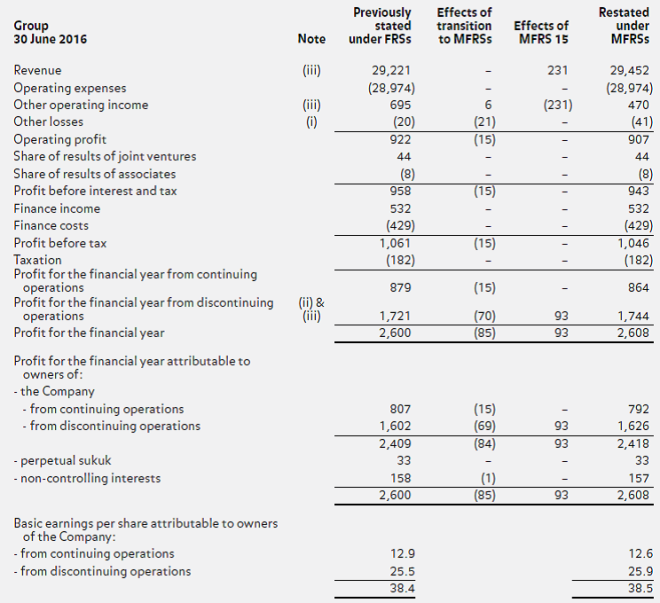

c. Reconciliation of profit or loss

Notes:

i. The operating profit prepared under FRSs included the net exchange gains recycled from exchange reserve following the repayment of foreign currencies denominated net investment and the disposal of foreign subsidiaries. The MFRS adjustments to the operating profit of RM15 million are in relation to the portion of exchange gains which arose prior to 1 July 2015, where the amount has been reset to zero upon the adoption of MFRSs.

ii. The profit for the financial year from discontinuing operations prepared under FRSs included a net exchange gain of RM52 million recycled from exchange reserve. The MFRS adjustments comprise the elimination of the portion of exchange gains which arose prior to 1 July 2015 of RM52 million, and the recognition of the changes in the fair value of biological assets, net of tax, of RM18 million in accordance with the requirement of MFRS 141.

iii. The MFRS 15 adjustments are mainly due to:

– the reclassification of other income of RM231 million to revenue; and

– the effect of changes to the timing of revenue recognition for the property development activities and club membership fees included in profit from discontinuing operations of RM93 million.

d. Reconciliation of comprehensive income

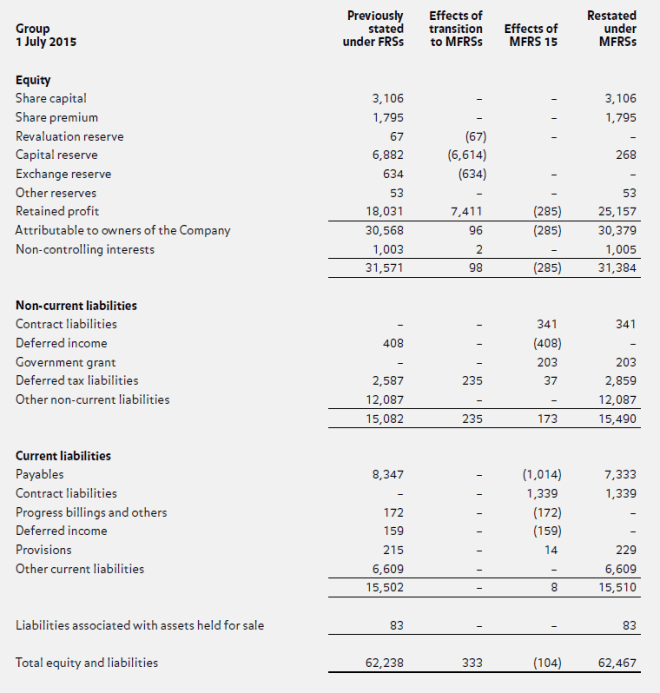

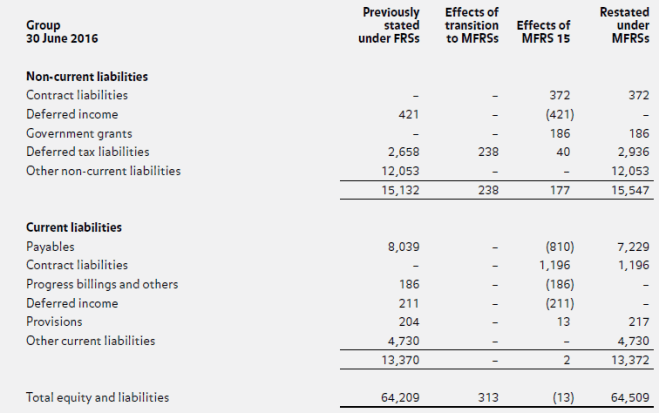

e. Reconciliation of financial position and equity

e. Reconciliation of financial position and equity

Notes:

i. The MFRS adjustments comprised:

– the transfer of the revaluation reserve and exchange reserve to retained profit following the election made by the Group to use the previous revaluation as deemed cost and to reset the exchange reserve as at 1 July 2015 to zero;

– the reclassification of merger reserve and capital reserve of RM6,231 million and RM383 million to retained profit;

– the adjustment to intangible assets and deferred tax liabilities to the same carrying amounts as those subsidiaries that have adopted the MFRS framework or IFRS earlier than the Company, after adjusting for consolidation adjustments; and

– the recognition of the fair value of biological assets of RM106 million as at 30 June 2016 (1 July 2015: RM133 million) in accordance with the requirement of MFRS 141, and the related tax effects of RM31 million (1 July 2015: RM35 million).

ii. The MFRS 15 adjustments are mainly due to:

– the effect of changes to the timing of revenue recognition for property development activities and club membership fees;

– the reclassification of the excess of revenue earned over the billings on construction and property development contracts to contract assets; and

– the reclassification of excess of billings over revenue earned on construction and property development contracts, deferred income and customers deposit to contract liabilities.

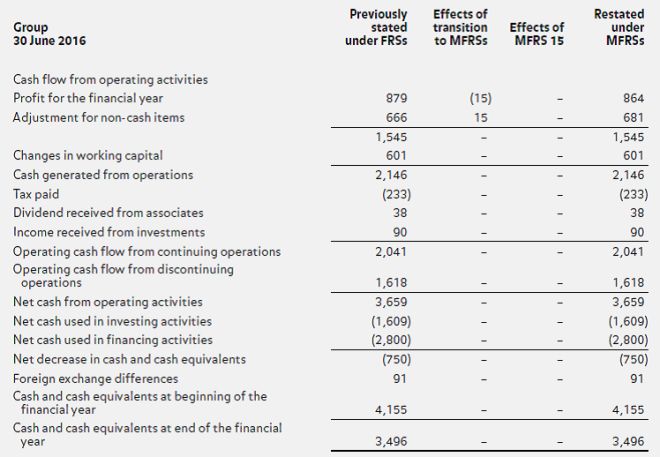

f. Reconciliation of cash flows