Finnair Oyj – Annual report – 31 December 2023

Industry: airline

Accounting principles (extract)

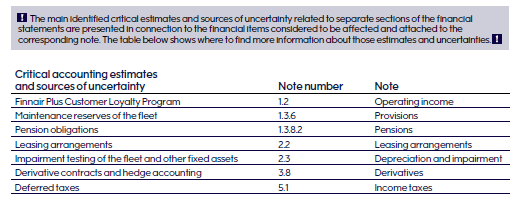

1.3.6 Provisions

Provisions

Provisions are recognised when the Group has a present legal or constructive obligation as the result of a past event, the fulfilment of the payment obligation is probable, and a reliable estimate of the amount of the obligation can be made. The amount to be recognised as provision corresponds to the management’s best estimate of the expenses that will be necessary to meet the obligation at the end of the reporting period.

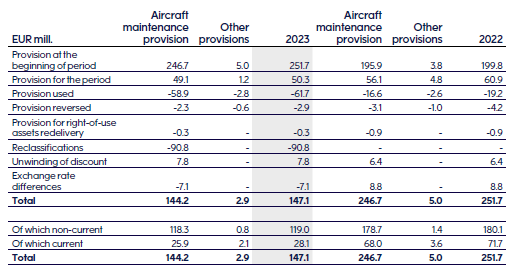

In most cases, the Group is obliged to return leased aircraft and their engines according to the redelivery condition set in the lease agreement. If at the time of redelivery, the condition of the aircraft and its engines differs from the agreed redelivery condition, Finnair needs to either maintain the aircraft so that it meets the agreed redelivery condition or settle the difference in cash to the lessor. To fulfil these maintenance obligations, the Group has recognised airframe heavy maintenance, engine performance maintenance, engine life limited part, landing gear, auxiliary power unit and other material maintenance provisions. The provision is defined as a difference between the current condition and redelivery condition of these maintenance components. The provision is accrued based on flight hours flown until the next maintenance event or the redelivery and recognised in the aircraft overhaul costs in the income statement. The provision is reversed at the maintenance event or redelivery. The price of the flight hour depends on the market price development of the maintenance costs. Estimated future cash flows are discounted to the present value. The maintenance market prices are mainly denominated in US dollars, which is why the amount of maintenance provision changes due to currency fluctuation of the dollar.

The final check and painting required at redelivery are considered unavoidable maintenance costs that realise when the aircraft is redelivered to the lessor, irrespective of the time or flight hours. The counterpart of the provision is recorded in the book value of the right-of-use asset at the commencement of the lease. Respectively, costs depending on the usage of the aircraft are not considered as part of the right-of-use asset cost, but these are recognised according to the principles presented above.

Restructuring provisions are recognised when the Group has prepared a detailed restructuring plan and has begun to implement the plan or has announced it.

Maintenance reserves of the fleet

The measurement of aircraft maintenance provisions requires management judgement especially related to the timing of maintenance events and the valuation of maintenance costs occurring in the future. The future maintenance costs and their timing are dependent on, for example, how future traffic plans actually realise, the market price development of maintenance costs and the actual condition of the aircraft at the time of the maintenance event.

Non-current aircraft maintenance provisions are expected to be used by 2035. Maintenance provisions of 90.8 million euros were reclassified against the acquisition cost of purchased, formerly leased aircraft.

In balance sheet, the non-current provisions and other liabilities 125.9 million euro (186.4) includes, in addition to provisions, other non-current liabilities 6.9 million euro (6.3), which mainly consist of received lease deposits.

2 Fleet and other fixed assets and leasing arrangements (extract 1)

Fleet and other fixed assets and leasing arrangements include notes particularly related to the aircraft fleet. Notes related to the aircraft operated by the Group are combined in this section so that the general view of the fleet is easier to understand. In addition to owned aircraft, the notes cover leased aircraft under different kinds of aircraft lease arrangements.

The assets owned and leased by Finnair consist mostly of aircraft operated by Finnair and Norra. In 2023, the number of owned aircraft was 46 (37) and leased aircraft 33 (43). During the financial year, Finnair purchased two A320 and seven A321 aircraft that it had been leasing in. All aircraft were in operative use as at the balance sheet date.

2 Fleet and other fixed assets and leasing arrangements (extract 2)

2.2 Leasing arrangements

The Group as lessee

Finnair assesses whether a contract that relates to tangible assets is, or contains, a lease in accordance with the IFRS 16. Lease agreements for tangible assets, where the contract conveys the right to use an identified asset for a period of time in exchange for consideration, are classified as leases.

The lease term is the non-cancellable period for which a lessee has the right to use an underlying asset, together with both periods covered by an option to extend the lease if Finnair is reasonably certain to exercise that option; and periods covered by an option to terminate the lease if Finnair is reasonably certain not to exercise the option.

The lease recognition requirements are not applied to short-term leases, where at the commencement date, the lease term is 12 months or less and does not contain a purchase option. Finnair considers the lease period to be the period that is enforceable. Hence, for contracts where the contract term is non-fixed and Finnair has the right to terminate the contract without the permission from the other party with no more than an insignificant penalty and there are no other indications that the contract is enforceable, Finnair classifies these contracts as short-term. The lease recognition requirements are also not applied to leases that are not material to Finnair.

For short-term leases and immaterial leases to which these exemptions are applied, the lease payments are recognised as an expense on either a straight-line basis over the lease term, or on another systematic basis if that basis is more representative of the pattern of Finnair’s benefit.

At the commencement date of a lease, Finnair recognises both a right-of-use asset and a lease liability.

The lease liability is the present value of future lease payments. At Finnair, lease payments for aircraft leases typically contain variable payments that depend on interest rates and indices. The variable payments are included in the measurement of the lease liability from the commencement date of the lease.

The right-of-use asset is measured at cost, comprising

- the amount of the initial measurement of the lease liability;

- any lease payments made at or before the commencement date, less any incentives received;

- any initial direct costs incurred by Finnair; and

- an estimate of costs to be incurred by Finnair in restoring the assets to the condition required by the terms and conditions of the lease.

In most cases, Finnair is obliged to return leased aircraft and their engines according to the redelivery condition set in the lease agreement. If at the time of redelivery, the condition of the aircraft and its engines differs from the agreed redelivery condition, Finnair needs to either maintain the aircraft so that it meets the agreed redelivery condition or settle the difference in cash to the lessor.

The maintenance costs can be divided into two main groups:

1) costs that are incurred independent of the usage of the aircraft / leasing period and

2) costs that are incurred dependent on the usage of the aircraft / leasing period

The final check and painting required at redelivery are considered unavoidable maintenance costs that realise when the aircraft is redelivered to the lessor, irrespective of the time or flight hours. The counterpart of the provision is recorded in the book value of the right-of-use asset at the commencement of the lease.

Respectively, costs depending on the usage of the aircraft are not considered as part of the right-of-use asset cost. Finnair remeasures the lease liability when there is a lease modification that changes the scope of a lease or the consideration for the lease, that was not part of the original terms and conditions of the lease (including changes in lease payments resulting from a change in indices and rates used in variable aircraft lease payments) or when the the likelihood of Finnair using a purchase-option is changed. The amount of the remeasurement of the lease liability is generally recognised as an adjustment to the right-of-use asset. However, if the carrying amount of the right-of-use asset is reduced to zero and there is a further reduction in the measurement of the lease liability, the remaining measurement is recognised in profit or loss.

After initial recognition, right-of-use assets are measured at cost less any accumulated depreciations and accumulated impairment losses. The assets are depreciated with a straight-line method from the commencement date to the shorter of end of useful life of the right-of-use asset and the end of lease term. However, if the lease transfers ownership of the asset to Finnair by the end of lease term or if the cost of the right-of-use asset reflects that Finnair will exercise a purchase option, the right-of-use asset is depreciated from the commencement date to the end of useful life of the asset.

At Finnair aircraft lease contracts contain the interest rate implicit in the lease, even if the aircraft lease agreements do not clearly define the interest rate implicit in the lease. Since the fair values of the aircraft are provided publicly by third parties, Finnair is able to calculate the implicit interest rate for each qualifying aircraft operating lease. The rate implicit in the lease is defined as the rate that causes the sum of the present value of the lease payments and the present value of the unguaranteed residual value of the underlying asset at the end of the lease to equal the sum of the fair value of the underlying asset and any initial direct costs of the lessor. The implicit interest rate is determined by each aircraft lease contract separately.

For other lease contracts, an implicit interest rate cannot be usually determined. The incremental borrowing rate is therefore used and it is determined by each class of assets separately, based on management estimate.

Aircraft lease contracts are usually denominated in foreign currency (US dollars) and the foreign currency lease liabilities are revalued at each balance sheet date to the spot rate. The lease payments (lease payments made) are accounted for as repayments of the lease liability and as interest expense.

The Group as lessor

Agreements, where the Group is the lessor, are accounted for as operating leases, when a substantial part of the risks and rewards of ownership are not transferred to the lessee. The assets leased under operating lease are included in the tangible assets and they are depreciated during their useful life. Depreciation is calculated using the same principles as the tangible assets for own use. Under the provisions of certain aircraft lease agreements, the lessee is required to pay periodic maintenance reserves which accumulate funds for aircraft maintenance. Advances received for maintenance are recognised as liability, which is charged, when maintenance is done. The rents for premises and aircraft are recognised in the income statement as other operating income over the lease term.

Agreements, where the Group is the lessor, are accounted for as finance leases, when a substantial part of the risks and rewards of ownership are transferred to the lessee. Finnair recognises assets held under a finance lease in its balance sheet and presents them as a receivable at an amount equal to the net investment of the lease which is equal to the sum of the present values of the lease income it will receive in the future and the unguaranteed residual value.

Finnair subleases aircraft and buildings as well as ground equipment from time to time, which are classified either as finance leases or operating leases based on the individual contract terms. A lease is classified on its commencement date and is reassessed only if the lease is amended. At the commencement date, for the subleases, a net investment (lease receivable), equaling to the present value of lease payments and the present value of the unguaranteed residual value, is recognised. The proportion of the right-of-use asset subleased is derecognised from the balance sheet and the difference between the right-of-use asset and the net investment is recognised in the profit or loss, in other operating income and expenses. Subsequently, the lease payments received are accounted for as repayments of the lease receivable and as interest income.

Sale and leaseback

In sale and leaseback transactions, where Finnair sells and then leases back aircraft, Finnair measures the right-of-use asset arising from the leaseback at the proportion of the previous carrying amount of the asset that relates to the right-of-use retained by the Group. Accordingly, Finnair recognises only the amount of any gain or loss that relates to the rights transferred to the buyer-lessor.

Leasing arrangements

Determining the interest rate and lease term used in discounting the lease payments, estimating the redelivery obligations of aircraft leases and the classification of sublease agreements to operating and financial leases require management discretion in interpretation and application of accounting standards.

The carrying value of the right-of-use assets are tested for impairment as part of cash generating unit at the balance sheet date. More details is presented in the note 2.3.