Heineken N.V. – Annual report – 31 December 2018

Industry: food and drink

4 Changes in accounting policies (extract)

IFRS 15 Revenue from Contracts with Customers

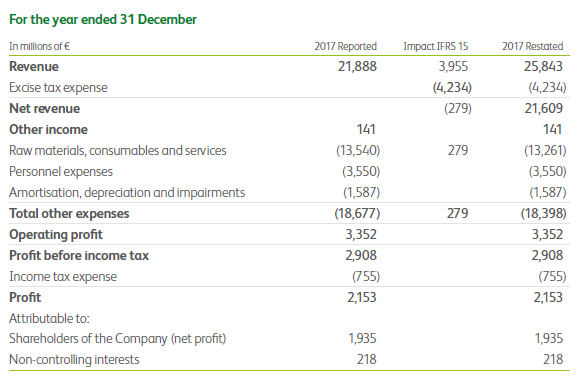

HEINEKEN adopted IFRS 15 ‘Revenue from Contracts with Customers’ as per 1 January 2018. For implementation the full retrospective method is applied, meaning that the 2017 comparative financial information has been restated. HEINEKEN concluded that IFRS 15 did not impact the timing of revenue recognition. However, the amount of recognised revenue is impacted by payments to customers and excise taxes as explained below. HEINEKEN has evaluated the available practical expedients for application of the standard and concluded that these options have no significant impact on HEINEKEN’s revenue recognition. The practical expedients have therefore not been applied.

The adoption of IFRS 15 has changed the accounting for certain payments to customers, such as listing fees and marketing support expenses. Most of these payments were recorded as operating expenses, but are now considered to be a reduction of revenue. Only when these payments relate to a distinct service the amounts continue to be recorded as operating expenses.

IFRS 15 has also changed the accounting for excise tax. Based on IAS 18 different policies were applied by peers in our industry. Some companies included all excises in revenue, some recorded excise only for specific countries and some, like HEINEKEN, excluded all excise from revenue. The clarifications to IFRS 15 describe that an ‘all or nothing’ approach is no longer possible and an assessment of the excise tax needs to be performed on a country by country basis.

Excise taxes are very common in the beverage industry, but levied differently amongst the countries HEINEKEN operates in. HEINEKEN performed a country by country analysis to assess whether the excise taxes are sales-related or effectively a production tax. In most countries excise taxes are effectively a production tax as excise becomes payable when goods are moved from bonded warehouses and are not based on the sales value. In these countries, increases in excise tax are not always (fully) passed on to customers and HEINEKEN cannot, or can only partly, reclaim the excise tax in the case products are eventually not sold to customers. Excise tax is borne by HEINEKEN for these countries and included in revenue. Only for those countries where excise is levied at the moment of the sales transaction and excise is based on the sales value, the excise taxes are collected on behalf of a tax authority and consequently excluded from revenue.

Due to the complexity and variety in tax legislations, significant judgement is applied in the assessment whether taxes are borne by HEINEKEN or collected on behalf of a third party.

To provide full transparency on the impact of the accounting for excise, HEINEKEN presents the excise tax expense on a separate line below revenue in the consolidated income statement. A new subtotal called ‘Net revenue’ is added. This ‘Net revenue’ subtotal is ‘revenue’ as defined in IFRS 15 (after discounts) minus the excise tax expense for those countries where the excise is borne by HEINEKEN. HEINEKEN furthermore discloses the excise collected on behalf of third parties, which is excluded from revenue, in note 6.1 Operating segments.

The IFRS 15 changes have no impact on operating profit, net profit and EPS. In below table the impact of IFRS 15 on the 2017 figures is reflected: