Ibstock plc – Annual report – 31 December 2016

Industry: manufacturing

- Summary of significant accounting policies (extract)

Employee benefits

The Group operates various post-employment schemes, including both defined benefit and defined contribution pension plans.

Pension obligations

A defined contribution plan is a pension plan under which the Group pays fixed contributions into a separate entity. The Group has no legal or constructive obligations to pay further contributions if the fund does not hold sufficient assets to pay all employees the benefits relating to employee service in the current and prior periods. A defined benefit plan is a pension plan that is not a defined contribution plan.

Typically, defined benefit plans define an amount of pension benefit that an employee will receive on retirement, usually dependent on one or more factors such as age, years of service and compensation.

The amount recognised in the balance sheet in respect of defined benefit pension plans is the present value of the defined benefit obligation at the end of the reporting period less the fair value of plan assets. The defined benefit obligation is calculated annually by independent actuaries using the projected unit credit method. The present value of the defined benefit obligation is determined by discounting the estimated future cash outflows using interest rates of high-quality corporate bonds that are denominated in the currency in which the benefits will be paid, and that have terms to maturity approximating to the terms of the related pension obligation.

Where defined benefit schemes have a surplus, the surplus is recognised if future economic benefits are available to the entity in the form of a reduction in the future contributions or a right to refund. See below judgement regarding the application of IFRIC 14.

The current service cost of the defined benefit plan, recognised in the income statement in employee benefit expense, except where included in the cost of an asset, reflects the increase in the defined benefit obligation resulting from employee service in the current year, benefit changes curtailments and settlements.

Past-service costs are recognised immediately in income. The net interest cost is calculated by applying the discount rate to the net balance of the defined benefit obligation and the fair value of plan assets, taking account of any changes in the defined benefit asset/liability during the period as a result of contributions and benefit payments. This cost is included in interest expense in the income statement.

When the benefits of a defined benefit plan are changed or when the plan is curtailed, the change in the present value of the defined benefit obligation arising that relates to the plan amendment or curtailment is recognised immediately in profit or loss on its occurrence. Before determining the past service cost (including curtailment gains or losses) or a gain or loss on settlement, the net defined benefit obligation (asset) is remeasured using the current fair value of plan assets and current actuarial assumptions (including current market interest rates and other current market prices) reflecting the benefits offered under the plan before the plan amendment, curtailment or settlement.

Remeasurement gains and losses arising from experience adjustments and changes in actuarial assumptions are charged or credited in other comprehensive income in the period in which they arise.

At 31 December 2015, a reimbursement asset was recognised representing an indemnity receivable from the former parent undertaking which was directly contributed to the pension scheme. A related liability for any additional pension liabilities that may arise as a result of the equalisation of pension benefits has been recognised within post-employment benefit obligations (see Note 21). This asset was received in January 2016.

For defined contribution plans, the Group pays contributions to publicly or privately administered pension insurance plans on a mandatory, contractual or voluntary basis. The Group has no further payment obligations once the contributions have been paid. The Group recognises contributions payable to defined contribution plans in exchange for employee services in employee benefit expense.

- Critical accounting judgements and estimates (extract)

Judgements (extract)

Defined benefit pension schemes

The Group’s accounting policy for defined benefit pension schemes requires management to make judgements as to the nature of benefits provided by each scheme and thereby determine the classification of each scheme. For defined benefit schemes, management is required to make annual estimates and assumptions about future returns on classes of scheme assets, future remuneration changes, employee attrition rates, administration costs, changes in benefits, inflation rates, life expectancy and expected remaining periods of service of employees. Management will reassess these assumptions going forward following the closure of the Scheme.

In relation to the Group’s post-employment obligations in the US, management make estimations relating to employee numbers, inflation rates, discount rates and future contribution rates. See Note 21(b) for further details.

These assumptions are based on the environment in the respective country. The assumptions used may vary from year to year, which would affect future net income and net assets. Any differences between these assumptions and the actual outcome also affect future net income and net assets. In making these estimates and assumptions, management considers advice provided by external advisers, such as actuaries. These assumptions are subject to periodic review.

In accounting for defined benefit plans, management is required to make judgements in relation to the application of International Financial Reporting Interpretations Committee guidance IFRIC 14 and its applicability to Ibstock plc. This judgement concerns the Group’s ability to recognise an actuarial surplus/notional surplus on the UK defined benefit pension scheme, should such a surplus/notional surplus arise in future. The Group has considered the application of this guidance, including proposed amendments to IFRIC 14 published as an exposure draft in June 2015. The Group has applied IFRIC 14 and recognised an additional liability of £14.2 million for minimum funding requirements. The Group has applied IFRIC 14 in preparing the Group consolidated financial statements, has reassessed these assumptions following the closure of the Scheme, and is keeping the position under review in the light of developments in the proposed amendments to IFRIC 14.

Additionally management has exercised judgement in the treatment of the multi-employer US pension as a defined contribution scheme.

Note 21 describes the assumptions used together with an analysis of the sensitivity to changes in key assumptions.

- Exceptional items (extract)

2016

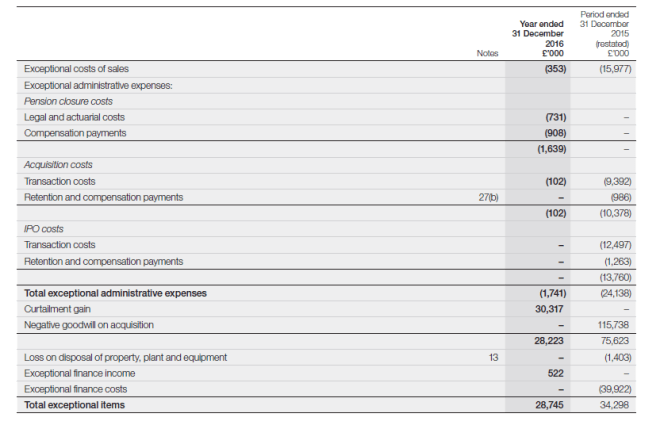

Included within the current year are the following exceptional items:

Exceptional cost of sales

Exceptional costs of sales in the current year of £353,000 represent redundancy costs associated with restructuring the Group’s operations in Ravenhead. Similar activities resulting in these costs are only expected to arise infrequently.

Pension closure costs

Professional advisor fees of £731,000, together with employee compensation payments of £908,000, were incurred in the current year in relation to the closure of the Group’s UK defined benefit pension scheme. Due to the non-recurring nature of the closure, these costs were treated as exceptional.

A curtailment gain of £30,317,000 arose in 2016 as a result of the Group’s decision to close the UK defined benefit scheme to future accrual.

Transaction costs

Professional fees and other costs of £102,000 incurred in the current year have been classified as exceptional. These costs are directly attributable to acquisition activity arising in the year and were classified as exceptional due to their non-recurring nature.

Exceptional finance income

Exceptional finance income in the year resulted from gains made on foreign currency contracts around the date of the UK’s EU Referendum. Similar gains are not expected to recur.

All exceptional items were settled in cash, other than compensation costs accrued at the balance sheet date and the pension curtailment gain that is non-cash in nature based on an actuarial valuation of the Group’s UK defined benefit pension scheme as at 31 December 2016.

Tax on exceptional items

Apart from the following items, exceptional items are taxable or deductible in full in the current period.

(i) The curtailment gain of £30,317,000 is not taxable in the current period. A deferred tax expense of £5,850,000 has been recognised in the period.

(ii) Administrative expenses include additional employer pension contributions of £265,000 arising from the closure of the Group’s UK defined benefit pension scheme. These pension contributions are tax deductible on a paid basis and a deferred tax asset of £51,000 has therefore been recognised.

(iii) Administrative expenses include exceptional legal and professional fees of £102,000 which are not tax deductible.

- Post-employment benefit obligations (extract 1)

(a) Defined benefit plan

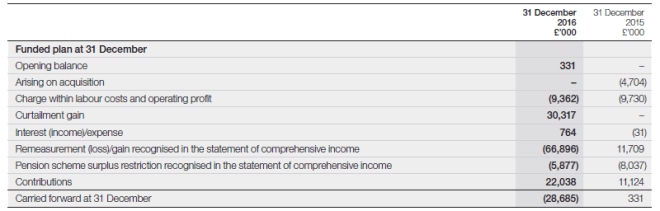

Analysis of movements in the net obligation during the period:

The Group participates in the Ibstock Pension Scheme (the ‘Scheme’), a defined benefit pension scheme in the UK. The Scheme has four participating employers – Ibstock Brick Limited, Forticrete Limited, Anderton Concrete Products Limited, Figgs Bidco Limited (from 26 February 2015) and Tyrone Brick Limited (up to 26 February 2015). The Scheme is funded by payment of contributions to a separate trustee administered fund. The scheme is a revalued earnings plan and provides benefits to its members based on their length of membership in the scheme and their average salary over that period. Following consultation with members, accounting for the Scheme’s closure to future accrual occurred in the year ended 31 December 2016. As a result, benefits were reassessed as active members were transferred to deferred membership.

The Scheme is administered by trustees who employ independent fund managers for the investment of the pension scheme assets. These assets are kept entirely separate from those of the Group.

Total annual contributions to the Scheme are based on independent actuarial advice, and are gauged to fund future pension liabilities (including projected increased in earnings and pensions) in respect of service up to the balance sheet date. The Scheme is subject to independent actuarial valuation at least every three years using the projected unit method.

The valuation used as at 31 December 2016 has been based on the results of the 30 November 2014 valuation, updated for changes in demographic assumptions, as appropriate.

Through its defined benefit pension plan, the Group is exposed to a number of risks that are inherent in such plans and arrangements. There are, however, no unusual, entity-specific or plan-specific risks, and no significant concentrations of risk. The risks can be summarised as follows:

- asset value volatility, with the associated impact on the assets held in connection with the funding of pension obligations and the related cash flows;

- changes in bond yields, with any reduction resulting in an increase in the present value of pension obligations, mitigated by an increase in the value of plan assets;

- risk of volatility in inflation rates as pension obligations are generally linked to inflation; and

- life expectancy, as pension benefits are provided for the life of beneficiaries and their dependents.

The Company and Trustees intend to de-risk the Scheme’s investment strategy by moving towards a position that is predominantly liability matching in nature. This involves an Asset Liability Management (‘ALM’) framework that has been developed to achieve long-term investments that are in line with the obligations under the Scheme. Within this framework the ALM objective is to match assets to the pension obligations by investing in risk-reducing assets (such as long-term fixed interest and index-linked securities). The Company actively monitors the investment strategy to ensure that the expected cash flows arising from the pension obligations are sufficiently met.

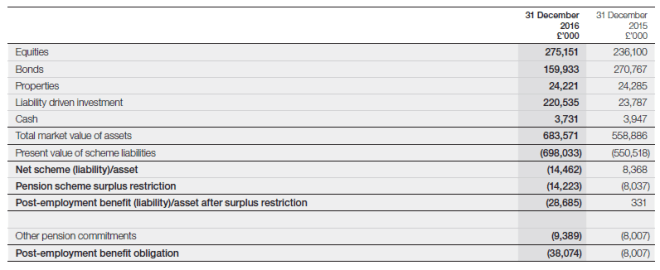

Balance sheet assets/(obligations):

All equities and bonds have a quoted market price in an active market. Properties and cash and cash equivalents are unquoted. Liability driven investment (‘LDI’) are funds constructed to reduce the risk within the Scheme. They help to mitigate against movements in inflation or interest rates by moving in a similar way to the liabilities following market movements. The funds are constructed from gilts and swaps. The Scheme’s LDI fund is managed by BMO and is predominantly unquoted.

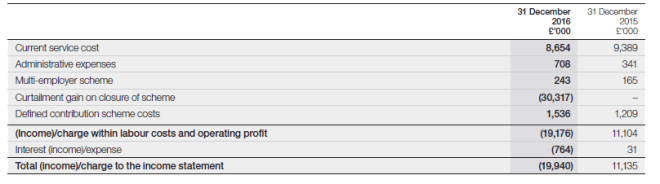

The amounts recognised in the income statement are:

- Post-employment benefit obligations (extract 2)

The Group contributed 16.0% of pensionable salaries to the Scheme during the period reported. Based on the most recent valuation, a payment schedule was agreed with the Trustees of the Ibstock Pension Scheme so that the Scheme’s deficit can be eliminated. This included the Group contributing 16% of pensionable salaries to the Scheme in the year ended 31 December 2016 (no longer required following the closure of the Scheme to future accrual), as well as a further £7.0 million per annum until May 2021. The weighted average duration of the defined benefit obligation is 20 years (2015: 19 years). In the year ended 31 December 2016, other costs related to the closure of the scheme to future accrual of £1,639,000 were incurred and classified as exceptional (see Note 5).