Victrex plc – Annual report – 30 September 2025

Industry: manufacturing

GOING CONCERN AND VIABILITY STATEMENT

GOING CONCERN

The Directors have performed a robust going concern assessment including a detailed review of the business’ rolling forecast and consideration of the principal risks faced by the Group and the Company, as detailed on pages 28 to 34. This assessment has paid particular attention to current trading results and both the impact of the ongoing global economic and sector specific challenges on the aforementioned forecasts.

Both the Group and the Company maintains a strong balance sheet providing assurance to key stakeholders, including customers, suppliers and employees. The Group had net debt of £24.8m at 30 September 2025, a reduction of £15.9m from 31 March 2025, and an increase of £3.7m from 30 September 2024. The increase in net debt during the year largely relates to the payment of dividends in February 2025, £40.1m, and June 2025, £11.7m. Underlying operating cash conversion improved to 121% for the year ended September 2025 from 114% for the year ended September 2024, supported by lower capital expenditure and the ongoing reduction in the inventory position. The Group drew on its UK revolving credit facility during the period to pay the final dividend, with a maximum drawn down of £18m (£26m maximum drawn down in the year ended 30 September 2024), before fully repaying the facility by the end of the year from operating cash flows. Of the gross debt position of £49.0m, £19.4m is due within one year. The Group maintains a cash balance sufficient to manage short-term liquidity and provide headroom against ongoing trading volatility. The cash balance at 30 September 2025 was £24.2m. Approximately 50% is held in the UK, on instant access, where the Group incurs the majority of its expenditure. At the date of this report, the Group has drawn c.£32m of its Chinese banking facility in its Chinese subsidiaries (with a total facility of c.£40m available until June 2029, subject to continuing to meet draw down criteria which will be reassessed in November 2026 as detailed below) and has unutilised UK banking facilities of £60m through to October 2028 of which £40m is committed and immediately available and a further £20m is available subject to lender approval.

The rolling forecast is derived from the Group’s Integrated Business Planning (‘IBP’) process which runs monthly. Each area of the business provides forecasts which consider a number of external data sources, triangulating with customer conversations, trends in market and country indices as well as forward-looking industry forecasts: for example, forecast aircraft build rates from the two major manufacturers for Aerospace; rig count and purchasing manager indices for E&I; World Semiconductor Trade Statistics semiconductor market forecasts for Electronics; and Needham and IQVIA forecasts for medical procedures.

The assessment of going concern included conducting scenario analysis on the aforementioned forecast. Whilst Sustainable Solutions has seen a continued recovery in sales volumes during FY 2025, although revenue growth was lower due to sales mix, Medical continues to experience lower demand, primarily in Spine which is offsetting strong progress in other application areas, with Medical sales reducing for the second year in a row since the record FY 2023. With economic forecasts remaining mixed, particularly for the chemical sector, and supply chains continuing to be cautious in both segments, the scenario analysis performed by management focuses on the Group’s ability to sustain a further period of suppressed demand in Medical and a return to lower volumes in Sustainable Solutions. In assessing the severity of the scenario analysis the scale and longevity of the impact experienced during previous economic downturns have been considered, including the differing impacts on the Sustainable Solutions and Medical segments.

Using the IBP data and the reference points from previous economic cycles, management has created two scenarios to model the impact of a reversal of the recovery seen in Sustainable Solutions since January 2024 and the continuing effect of softer demand within Medical at a regional/market level and aggregated levels on the Group’s profits and cash generation through to January 2027 with consideration also given to the six months beyond this. The impact of climate change is not considered to have a significant impact over the going concern period and, as a result, the scenario testing noted below does not incorporate any additional sensitivity specific to climate change.

The Directors have modelled the following scenarios:

Scenario 1 – Sustainable Solutions demand reduces back to the levels seen before the recovery in volumes for a period of six months from January 2026, before recovering to the levels seen in the past 12 months for the remainder of the going concern period. Medical revenue remains in line with the softer level experienced during FY 2025 through to June 2026 before recovery commences at a rate of 10% per annum through the remainder of the going concern period. Inventory is reduced in line with sales.

Scenario 2 – In line with scenario 1 through to June 2026 but with the lower demand continuing throughout 2026, i.e. throughout the going concern period. This would give an annualised volume below c.3,500 tonnes, a level not seen since 2013 with the exception of the COVID impacted FY 2020. In this scenario softer demand would continue to impact Medical revenue which would remain at an annualised revenue comparable to FY 2025 of c.£58m throughout the going concern period, a level, prior to FY 2025, not seen in the past 10 years. Inventory is reduced in line with sales. The Directors consider scenario 2 to be a severe but plausible scenario.

Following operational challenges sales from the new PEEK manufacturing facility in China have remained at a modest level during FY 2025; however, with the challenges now largely resolved and the Commercial team in place to more aggressively pursue the opportunities, volume growth is forecast to accelerate. Whilst this happens there is a period where additional funding is required to see it through to net cash generation. In concluding on the going concern position, it has been assumed that the Group will provide the additional funds in full, which the Board considers to be the worst case scenario. The locally provided external funding is due for repayment in December 2026. The Group has agreed to refinance this facility through to June 2029 with the drawdown of a new facility in November 2026 to repay the existing facility. This facility is not committed until it is drawn down and therefore the going concern assessment assumes that the £24.6m is repaid by December 2026, which would require a partial drawdown of the UK revolving credit facility in each of the scenarios.

Before any mitigating actions the sensitised cash flows show the Group has significantly reduced cash headroom, which would require continued use of the committed UK banking facility during the going concern period. The level of facility drawn down is forecast to be similar with the past two financial years. The level of facility drawn down is higher in scenario 2 but in neither scenario is the committed facility fully drawn, nor drawn down for the whole year. With cash levels lower than has historically been the case for Victrex, particularly if the aforementioned new China bank facility is not drawn down and therefore the existing facility requires repayment using the UK revolving credit facility, or other as yet unsecured new facilities, in December 2026, the Group and the Company have identified a number of mitigating actions which are readily available to increase the headroom.

These include:

- Use of committed facility – the undrawn committed facility could be drawn at short notice. Conversations with our banking partners indicate that the £20m uncommitted accordion could also be readily accessed. The covenants of the facility have been successfully tested under each of the scenarios;

- Securing additional debt facilities – the company could seek to obtain additional debt from existing banking partners or other potential lenders;

- Deferral of capital expenditure – the base case capital investment over the next 12 months is lower than recent years with major projects now completed. This could be reduced further by limiting expenditure to essential projects and deferring all other projects later into 2026 or beyond;

- Reduction in discretionary overheads – costs would be limited to prioritise and support customer-related activity;

- Further reduction in inventory levels – the elevated inventory level seen at the end of FY 2023 has been partially unwound across FY 2024 and FY 2025 with a further reduction targeted in FY 2026. The scenarios noted above include an acceleration of the inventory unwind but a more aggressive approach could be taken to provide additional cash resources; and

- Reduction/deferral/cancellation of dividends – the Board considers the cash position and interests of all stakeholders before recommending payment of a dividend. A dividend has been proposed for payment in February 2026 of c.£40m and in the past an interim dividend of c.£12m has been paid in July, giving a combined annual outflow of c.£52m.

Reverse stress testing was performed to identify the level that sales would need to drop by in order for the Group or Company to be unable to meet its liabilities as they fall due before the end of the going concern assessment period. Sales volumes would need to consistently drop materially below the low point in scenario 2 which is not considered plausible.

As a result of this detailed assessment and with reference to the Group and Company’s strong balance sheet, existing committed facilities and the cash preserving levers at the Group and Company’s disposal, but also acknowledging the current economic uncertainty created by the increase in global tariffs, particularly in the US, the depressed chemical sector and the war in Ukraine continuing, the Board has concluded that both the Group and Company have sufficient liquidity to meet their obligations when they fall due for a period of at least 12 months after the date of this report. For this reason, they continue to adopt the going concern basis for preparing the financial statements.

VIABILITY STATEMENT

1. Assessment of prospects

The Directors have assessed the Group’s longer-term prospects, primarily with reference to the results of the Board-approved five-year strategic plan. This is driven by the Group’s business model (detailed on pages 8 and 9) and strategy (detailed on page 10 to 13), which are fundamental to understanding the future direction of the business, while factoring in the Group’s principal risks (detailed on pages 28 to 34) and the potential opportunities and risks of climate change (detailed on pages 46 to 47). The Directors continue to consider the ongoing challenges to the global economy, including the impact on each market and geography which the Group serves, and the uncertainty this creates, particularly in the early years of the strategic plan. The Directors have also considered the Group’s ability to generate cash, manage shareholder returns and maintain a strong financial position throughout the economic cycle, including the level of cash and overall net debt at 30 September 2025.

The strategic planning process is undertaken annually and includes analyses of profit performance (including core business and new product pipeline and ‘mega-programmes’), cash flow, investment programmes (including manufacturing capacity increases and the acquisition pipeline) and returns to shareholders. Completion of the strategic plan is a Group-wide process engaging employees throughout the business, including all senior management in their respective areas. The strategy was reviewed and approved by the Board in March 2025 (covering the five years to September 2030). The strategy is built market by market, geography by geography recognising the differing dynamics in each whilst also considering the longer-term impact of the Company achieving its goal of Net Zero across all scopes by 2050, including reducing 2022 Scope 1 & 2 emissions by 50% by the interim testing date of 2032, combined with the wider global ambition to reduce carbon usage. The Company also operates a shorter-term rolling 24-month forecast, predicated on the IBP process, which forms the basis for the 2026 budget and key operational decisions over this shorter time frame. The first year of the strategy has been realigned to the 2026 budget, taking account of changes to the economic outlook since the strategy was finalised, with subsequent years reviewed and updated where the revisions to the first two years are expected to have a consequential impact, either positive or negative. The realigned strategy was approved by the Board alongside the 2026 budget in October 2025 and has also been used for the annual impairment review detailed on page 149.

2. Viability period

The Directors have assessed the viability of the Group over the five-year period to September 2030, being the period covered by the Group’s Board-approved strategic plan.

The Board considers five years to be an appropriate time horizon for the strategic plan, being the period over which the Group actively focuses on its development pipeline and resulting capital investment programme. As part of the longer-term considerations, to support capacity planning and assessment of projects which will take longer to reach meaningful revenue, the Group does prepare forecasts for a period of more than five years; however, a period greater than five years is considered too long for the strategic plan given the inherent uncertainties involved.

3. Assessment of viability

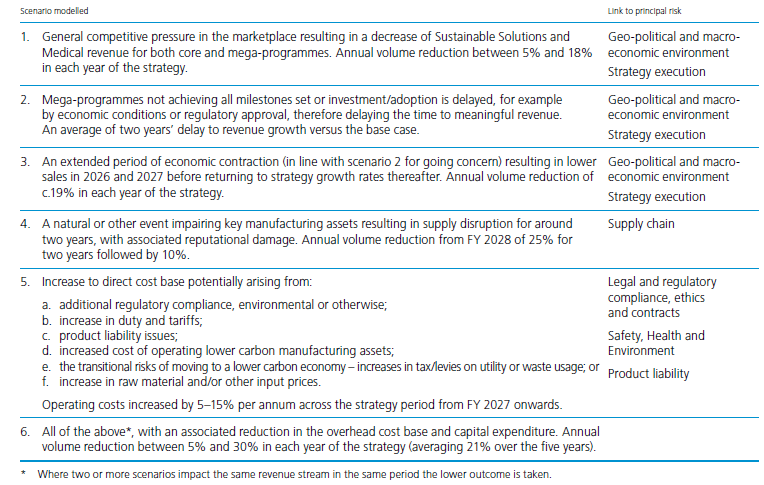

To make their assessment of viability, the Directors have tested a number of additional scenarios on the base case position of the five-year strategic plan. These scenarios encompass key trading assumptions combined with the potential impact of crystallisation of one or more of the principal risks over the five-year period. Whilst each of the principal risks has a potential impact, the scenario analysis has been focused on those considered to have the most significant financial impact, primarily to the revenue growth of the Group. The risks have been assessed for their potential impact on the Group’s business model, future trading and funding structure.

The mega-programmes are forecast to have a material impact on the Company’s revenue over the strategic period. Progress continues to be made across the mega-programmes with milestones being achieved as outlined in the Strategic report on pages 1 to 67 even though the translation of the progress into revenue growth has been slower than anticipated. The timing of future milestone achievement and the resulting impact on revenue growth remain the key variables which the Directors have incorporated into scenario 3 described below.

The impact on the strategy of both the Company achieving its goal of Net Zero across all scopes by 2050 and the wider economy achieving Net Zero carbon over a long period continues to be understood and assessed. The physical risks and transitional opportunities and risks have been considered in detail as described in the Sustainability report on pages 38 to 67. The physical risks presented by climate change are not expected to have a material impact on the Company’s ability to manufacture product over the strategy period and therefore no sensitivity has been performed. At the revenue level the transitional opportunities are considered to outweigh the risks over both the short and longer time horizons, supporting continued growth in Company revenues, albeit the impact of this is only likely to be material outside of the five-year strategy window. The primary transitional risk relates to the additional capital and operating costs associated with electrification of the heat sources used in the manufacturing processes, which primarily rely on the burning of gas. Failure to do this will potentially leave the Group exposed to the likely levers used by regulators and governments to drive down use of carbon – taxation and levies. Work is ongoing to reduce the carbon usage in the manufacturing process, both through using green sources of electricity to supply the aforementioned electrical heat sources and redesigning the chemical process to reduce the overall energy requirement and waste generation. Acknowledging the risk to the decarbonisation of the manufacturing process, primarily in respect of timing, and increased cost of operation have been assumed in scenario 5. The Company would seek to recover this cost from customers but for the purpose of the scenario analysis a worst case position of no recovery has been assumed.

The scenarios tested were carefully considered by the Directors, factoring in the potential impact, probability of occurrence and the effectiveness of the mitigating actions. In addition, whilst considered implausible, a combined scenario (scenario 6) was also tested, which contained an aggregation of all scenarios considered. Consistent with going concern, it has been assumed in all scenarios (except scenario 6 – see below) that the future funding needs, including the repayment of external debt when it becomes due, of the PEEK manufacturing facility in China are met by the Group, which the Board considers to be the worst case scenario.

The downside scenarios applied to the strategic plan are as follows:

The key mitigating actions available to the Directors are consistent with those outlined above in going concern, incorporating the Group’s ability to manage its cost base, reduce working capital and raise new finance and the possibility of delaying capital programmes and/or restricting shareholder returns, all of which could be applied over the longer viability period. In addition to these specific mitigation plans, the Group’s two distinct segments, both with diverse geographic markets, assist in reducing the risk of regional economic challenges and sector specific issues. Further, the strategy of partnering closely with customers to develop the right applications and our existing and growing list of specified products are also important mitigants.

The results of this stress testing showed that the Group would be able to remain solvent and maintain liquidity over the assessment period. The Group is profitable under all scenarios, including scenario 6. The lowest cash balance was in scenario 6, in which the cash balance remains positive albeit at a level where continued use of the debt facilities in China and partial use of the RCF is required through the five-year period. The China facility has recently been refinanced through to June 2029, subject to a reassessment of the draw down criteria in November 2026. The Directors anticipate that the criteria will be met and that the facility could be further extended, based on the forecast sales growth and cash generation, if required through to the end of the 5 year horizon, but recognise this is not committed.

The RCF is available until October 2028 and the Directors anticipate refinancing would take place before this date. Whilst there is no guarantee this will be successful, the Directors anticipate, based on the ongoing profitability of the business, to be able to successfully refinance through to the end of the five-year horizon. Covenant compliance has been successfully tested under scenario 6 throughout the period to October 2028.

In the event refinancing of the China facility and the RCF is unsuccessful, the Directors have other mitigating options available to increase headroom which are outlined in the going concern disclosure on pages 35 and 36. Due to the severity and implausibility of scenario 6, an outcome that requires use of the aforementioned facilities, this is considered akin to a reverse stress test.

4. Viability statement

Based on the results of this detailed analysis the Directors have a reasonable expectation, that the Group will be able to continue in operation and meet its liabilities as they fall due over the five-year period to September 2030. This is predicated on the assumption that an unforeseen event outside of the Group’s control (for example, an event of nature or terror) does not inhibit the Company’s ability to manufacture for a sustained period.