Toyota Motor Corporation – Annual report – 31 March 2025

Industry: automotive

3. Material accounting policies (extract)

Liabilities for quality assurance –

Toyota generally warrants its products against certain manufacturing and other defects. Provisions for product warranties are provided for specific periods of time and/or usage of the product and vary depending upon the nature of the product, the geographic location of the sale and other factors. The accrued warranty costs represent management’s best estimate at the time of sale of the total costs that Toyota will incur to repair or replace product parts that fail while still under warranty. The amount of accrued estimated warranty costs is primarily based on historical experience of product failures as well as current information on repair costs. An estimate of warranty claims accrued for each fiscal year is calculated based on the estimate of warranty claims per unit. The estimate of warranty claims per unit is calculated comprehensively by dividing the actual amounts of warranty claims by the number of sales units for the fiscal year.

Toyota accrues for costs of recalls and other safety measures, as well as product warranty cost described above. Toyota generally measures such “liabilities for recalls and other safety measures” at the time of vehicle sales comprehensively by aggregate sales of various models in a certain period by geographical regions. However, when circumstances warrant, Toyota measures “liabilities for a particular recall or other safety measures” using an individual model when they are probable and reasonably estimable.

The portion of “liabilities for recalls and other safety measures” recorded in the consolidated statement of financial position is calculated comprehensively based on the “expected liability for the cost of recalls and other safety measures” in consideration of the “accumulated amount of repair cost paid”. As such, this liability is evaluated every period based on new data and is adjusted as appropriate. Toyota calculates these liabilities for units sold in the current period and each of the past 10 fiscal years, and aggregates such liabilities in determining the final liability amount.

The “expected liability for the cost of recalls and other safety measures” is calculated by multiplying the “sales unit” by the “expected average repair cost per unit”. The “expected average repair cost per unit” is calculated based on dividing the “accumulated amount of repair cost paid per unit” by the “pattern of payment occurrences”. The “pattern of payment occurrence” represents a ratio that shows the measure of payment occurrence over 10 years based on actual payments with regard to units sold within 10 years.

Factors that may cause a difference between the amount accrued comprehensively at the time of vehicle sale and actual payment on individual recalls and other safety measures mainly include actual cost of recalls and safety measures during the period being significantly different from the accumulated amount of repair cost paid per unit (generally comprised of parts and labor) and the actual pattern of payment occurrence during the period being significantly different from the pattern of the payment occurrence in the past. Such differences are considered as part of our estimation process for future recalls and other safety measures.

Liabilities for product warranties and liabilities for recalls and other safety measures have been combined into “Liabilities for quality assurance” in the consolidated statement of financial position. Product warranty costs and costs of recalls and other safety measures are included in cost of products sold in the consolidated statement of income.

The foregoing evaluations are inherently uncertain, as they require material estimates as described above. Consequently, actual warranty costs may differ from the estimated amounts and could require additional warranty provisions. If these factors require a significant increase in Toyota’s accrued estimated warranty costs, it would negatively affect future operating results of the automotive operations.

4. Significant accounting judgments and estimates

The preparation of the consolidated financial statements in conformity with IFRS Accounting Standards requires management to make judgments, estimates, and assumptions that affect the application of accounting policies, the reported amounts of assets, liabilities, revenues and expenses, and the disclosure of contingent assets and liabilities. Actual results could differ from these estimates. These estimates and underlying assumptions are reviewed on a continuous basis. Changes in these accounting estimates are recognized in the period in which the estimates were revised and in any future periods affected.

Information about important estimation and judgments that have significant effects on the amounts recognized in the consolidated financial statements is as follows:

Scope of subsidiaries, associates, and joint ventures (Note 3 “Basis of consolidation”)

Intangible assets incurred by research and development (Note 3 “Intangible assets”)

Information about accounting estimates and assumption that affect the application of accounting policies and the reported amounts of assets and liabilities, and financial statements based on IFRS Accounting Standards is as follows:

Liabilities for quality assurance (Note 3 “Liabilities for quality assurance” and Note 24)

Allowance for credit losses on finance receivables (Note 3 “Allowance for credit losses on finance receivables” and Note 19 (2))

Impairment of non-financial assets (Note 3 “Impairment of non-financial assets” and Note 12) Employee benefit obligations (Note 3 “Employee benefit obligations” and Note 23)

Fair value measurements (Note 21)

Recoverability of deferred tax assets (Note 3 “Income taxes” and Note 15)

24. Liabilities for quality assurance

Toyota provides product warranties for certain defects mainly resulting from manufacturing based on warranty contracts with its customers at the time of sale of products. Toyota accrues estimated warranty costs to be incurred in the future in accordance with the warranty contracts. In addition to product warranties, Toyota initiates recalls and other safety measures to repair or to replace parts which might be expected to fail from products safety perspectives or customer satisfaction standpoints. Toyota accrues for costs of recalls and other safety measures based on the amount estimated from historical experience.

Liabilities for product warranties and liabilities for recalls and other safety measures have been combined into “Liabilities for quality assurance” in the consolidated statement of financial position due to the fact that both are liabilities for costs to repair or replace defects of vehicles and the amounts incurred for recalls and other safety measures may affect the amounts incurred for product warranties and vice versa.

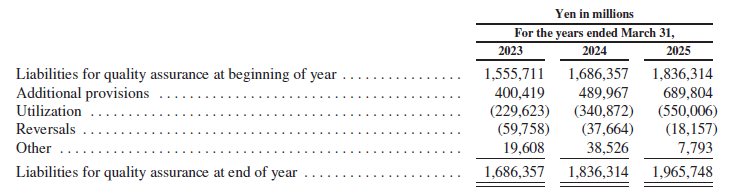

The net change in liabilities for quality assurance for the years ended March 31, 2023, 2024 and 2025 consist of the following:

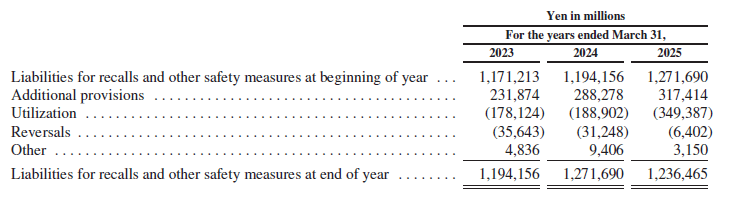

The table below shows the net changes in liabilities for recalls and other safety measures which are comprised in liabilities for quality assurance above for the years ended March 31, 2023, 2024 and 2025.