Telkom SA SOC Limited – Annual report – 31 March 2017

Industry: Telcoms

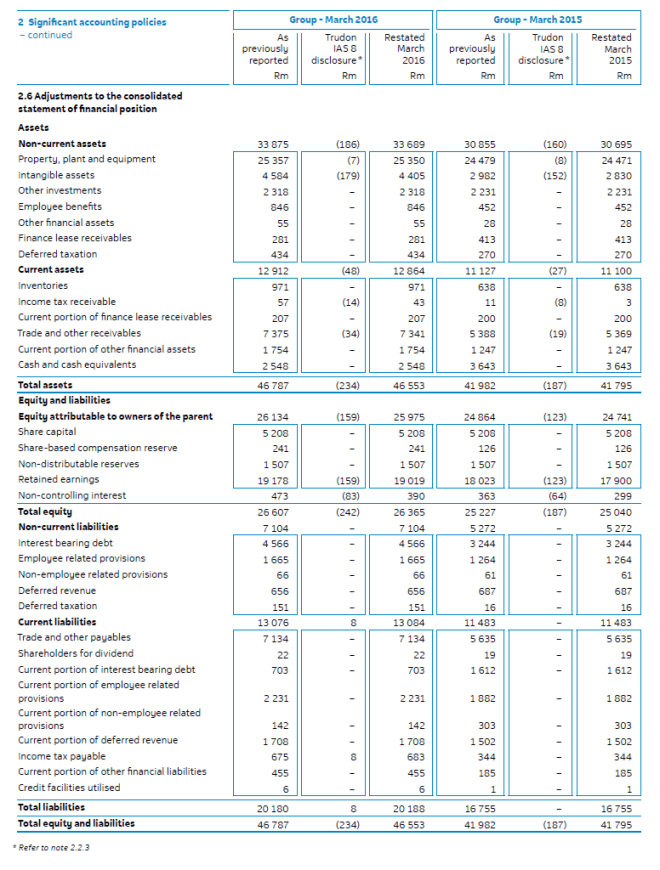

2 Significant accounting policies (extract 1)

2.2 Correction of prior period errors and change in accounting policies

Correction of prior period errors

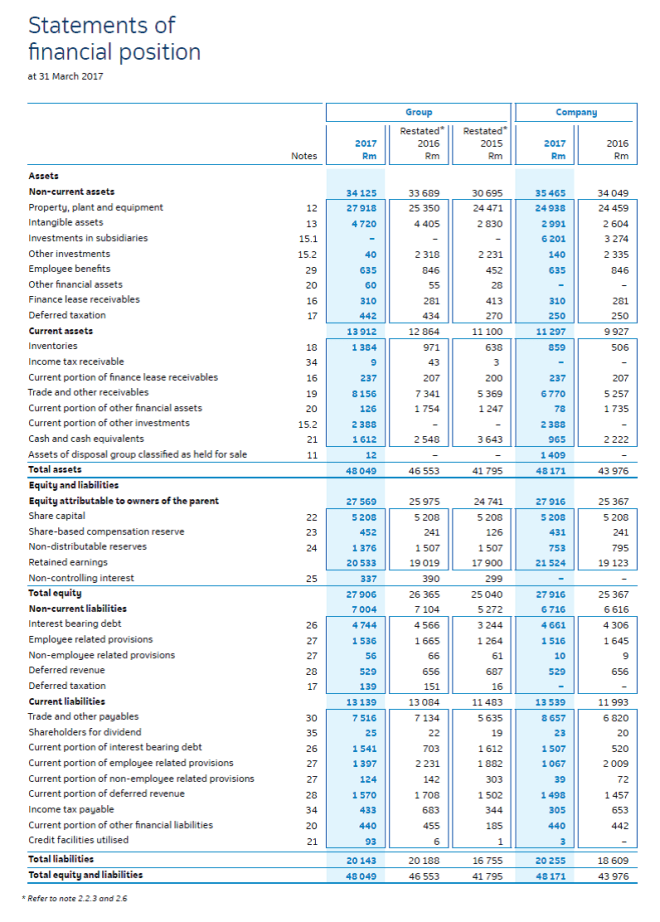

The consolidated financial statements provide comparative information in respect of the previous period. In addition, the group presents an additional statement of financial position at the beginning of the preceding period when there is a retrospective application of an accounting policy and a retrospective restatement. An additional statement of financial position as at 31 March 2015 is presented in these consolidated financial statements due to the retrospective correction of a prior period error.

2.2.1 Telkom Retirement Fund

During the 31 March 2016 reporting period, the group reported the restatement of the balances as a “Reassessment of the Telkom Retirement Fund (TRF) Defined Benefit Plan”. For classification purposes, it should be noted that the reassessment of the TRF constituted an error and not a change in accounting policy as previously stated. All relevant IAS 8 disclosures (nature, correction amounts and the amount of correction at the beginning of the year) regarding the error were appropriately disclosed in the March 2016 financial statements.

2.2.2 Fair value hierarchy

During the previous reporting periods, the group reported the fair value hierarchy of the TL20 bonds as level 1 instead of level 2 based on the fact that it could access the quoted price of the bonds. According to IFRS 13, bonds can only be level 1 if they are quoted on active market. The TL20 bonds are quoted on the market, however their transactions are not sufficiently frequent for the market to be regarded as liquid.

The group has corrected this disclosure by changing the TL20 fair value hierarchy from level 1 to level 2. The group has assessed that there has been no impact on the fair value of the TL20 bonds in the prior year as the quoted price is an adjusted market price, for perceived changes in risk as well as the time value of money. The group will continue to assess if the quoted price of the listed TL20 bonds is considered to be a level 1 or level 2 price and if further adjustment might be required.

2.2.3 Fraud – Trudon

During the current financial year, the group uncovered financial irregularities at one of its subsidiaries, Trudon, resulting in the termination of the services of the general manager IT.

An internal investigation into the financial irregularities was launched, which identified invoicing and accounting irregularities which led to the incorrect recognition and subsequent measurement of intangible assets over a period of several years. The investigation also identified the past practice of irregularly capitalising operating expenditure as intangible assets. The nature of the errors identified included:

- Intangible assets capitalised for which there was no evidence of a valid asset or expense as a result of the above financial irregularities

- Expenses capitalised to intangible assets which on re-evaluation of the nature of expense, based on the invoice detail, was deemed to not meet the recognition criteria of IAS 38 at date of capitalisation

- Identification of intangible assets which were no longer in use and which had been decommissioned in earlier periods but not de-recognised at time of decommissioning

- Income tax implications in relation to expenses and wear and tear allowances deducted in prior periods relating to invoices associated with financial irregularities which, based on senior counsel opinion, should not have been deducted for tax purposes

These issues identified constituted material prior period errors and have been corrected by restating each of the affected line items for the prior period as shown in the table 2.5 and 2.6 below.

2.2.4 Change in accounting policies

Cost of sales

The group has previously included all the expenses that can be directly linked to revenue received for services provided and goods sold to customers in the definition of cost of sales.

Following the sale of the Enterprise business to BCX in November 2016, the group elected to change its accounting policy for cost of sales to only include expenses directly linked to revenue from the sale of goods. This decision to change the accounting policy in the view of management will provide more reliable and relevant information to ensure consistent presentation across the group following the sale of Enterprise to BCX. Please refer to note 2.4.22 for the new accounting policy.

This change in policy has resulted in the reclassification of these line items in the comparative statement of profit or loss and other comprehensive income. Refer to note 2.5.

2 Significant accounting policies (extract 2)