Ørsted A/S – Annual report – 31 December 2025

Industry: manufacturing

Note 3.10

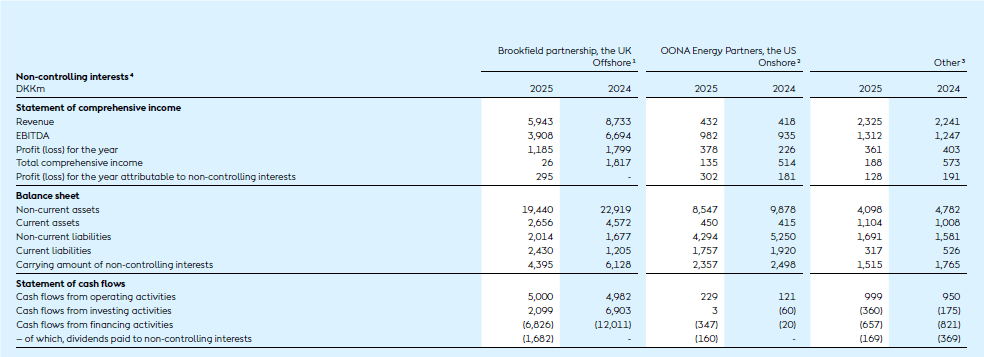

Non-controlling interests

In the table, we provide financial information for subsidiaries with significant non-controlling interests. The amounts stated are the consolidated accounting figures of the individual enterprises or groups, determined according to our accounting policies. Amounts are stated before intra-group eliminations.

1 In 2024, we divested a 24.9 % equity stake of our 50 % share (equivalent to a 12.45 % share) in four UK offshore assets: Hornsea 1, Hornsea 2, Burbo Bank Extension, and Walney Extension, each represented by an individual holding company taking in Brookfield as non-controlling owner. We retain a 37.55 % equity ownership stake in these wind farms.

2 In 2024, we divested an 80 % equity stake in four of our US onshore assets: Ford Ridge Wind, Sunflower Wind, Helena Wind, and Western Trail Wind to Stonepeak. We retain a 20 % equity ownership stake.

3 Primarily related to UK assets: Walney and Gunfleet Sands.

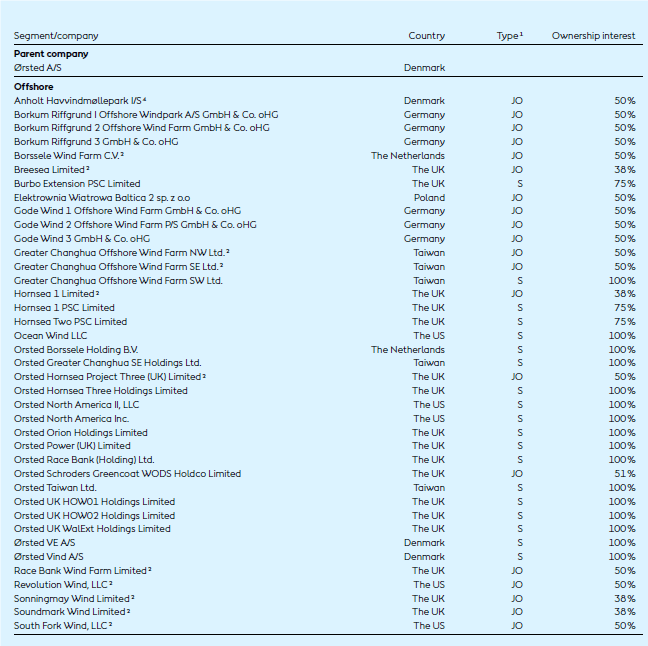

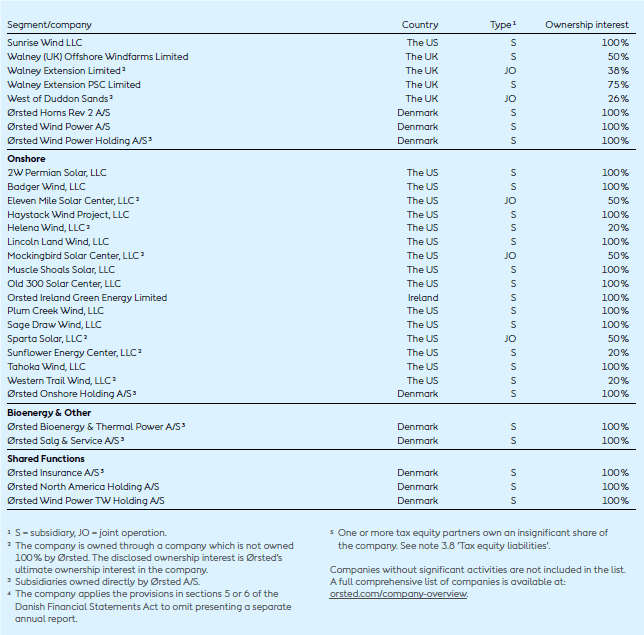

4 A complete list of all non-controlling interests, their company legal names, and country of registration can be found here: orsted.com/company-overview

Accounting policies

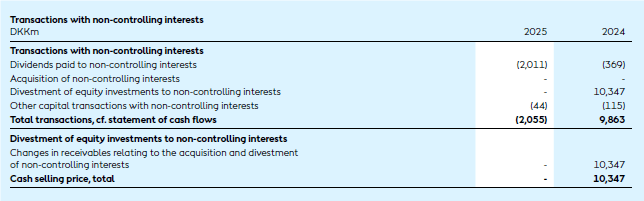

Transactions with non-controlling interests are accounted for as transactions with the shareholder base.

Gains and losses on the divestment of equity investments to non-controlling interests are recognised in equity when the divestment does not result in a loss of control. See ‘Consolidated statement of shareholders’ equity’ and note 5.2 ‘Equity’.

For a description of our ‘Key accounting judgements’ on ‘Consolidated method for partnerships’, see note 2.6 ‘Other operating income and expenses’.

Note 2.6

Other operating income and expenses (extract)

Key accounting judgements

Consolidation method for partnerships

On establishment of partnerships and in connection with any restructuring of existing partnerships, we perform an assessment to determine whether we control the investee. Significant judgements are applied to determine who controls the economically and operationally significant decisions in the partnership, and whether arrangements with partnerships are considered a non-controlling interest or a financial liability. Relevant items to consider typically involve decisions related to budget approval, sale of power, and decommissioning and repowering.

For joint arrangements, we subsequently assess whether they are joint ventures or joint operations.

In assessing joint operations, we consider:

- the corporate form of the operation

- whether we are only entitled to the net profit (loss) or to income and expenses resulting from the operation.

In addition, the fact that the parties buy or are assigned all output, for example the power generated, will lead to the structure being considered a joint operation if we have joint control.

The assessment of the consolidation method determines the recognition of gain or loss on divestments as either operating income in the income statement or as transactions with a non-controlling interest in equity.

Note 7.4

Company overview