Toyota Industries Corporation – Annual report – 31 March 2025

Industry: manufacturing

3. Material Accounting Policies (extract)

(16) Impairment Losses (extract)

(i) Financial assets

Financial assets measured at amortized cost are assessed for impairment losses based on expected credit losses. At the end of the reporting period, if credit risk has not increased significantly after initial recognition, the amount of loss allowance is calculated based on the expected credit losses resulting from default events that are possible within 12 months after the reporting date (12-month expected credit losses). On the other hand, at the end of the reporting period, if credit risk has increased significantly after initial recognition, the amount of loss allowance is calculated based on the expected credit losses resulting from all possible default events over the life of the financial instrument (lifetime expected credit losses).

However, regardless of the above, lifetime expected credit loss measurement always applies to trade receivables and lease investment assets without a significant financing component.

For details, see “30. Financial Instruments (2) Matters concerning risk management”.

6. Trade Receivables and Other Receivables

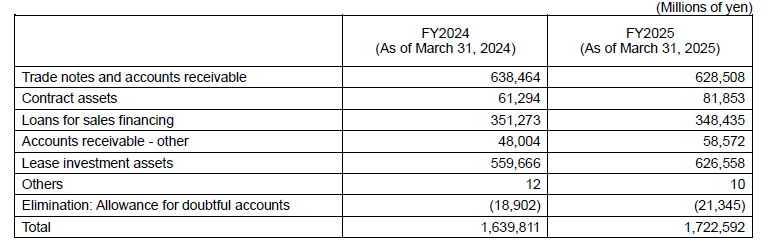

Trade receivables and other receivables consist of the following.

These receivables are mainly financial assets measured at amortized cost.

Amounts by collection or settlement period consist of the following.

30. Financial Instruments (extract)

i) Credit risk

The main receivables of Toyota Industries such as accounts receivable, lease investment assets and loans receivable related to the sales financing business have credit risk (risk concerning non-performance of an agreement by the counterparty). In accordance with internal rules including the treasury policy, Toyota Industries strives to promptly identify and reduce concerns about collection due to a deterioration in the financial conditions and others of its main counterparties by regularly monitoring their situation based on their financial statements, ratings and others, and conducting due date management and balance management. Collection risk of lease investment assets is minimal because their ownership is not transferred and due date management and balance management are conducted. Toyota Industries has no material concentrations of credit risk with any counterparty.

When using derivative transactions, Toyota Industries mainly deals with only financial institutions evaluated as highly creditworthy by rating agencies to mitigate the counterparty risk.

Regarding accounts receivable, lease investment assets and loans receivable related to the sales financing business, if all or part of them cannot be collected or are deemed to be extremely difficult to collect, they are regarded as non-performing.

The total carrying amount of financial assets represents the maximum exposure to credit risk.

(Measuring expected credit loss for accounts receivable and lease investment assets)

Because there is no material financing component in accounts receivable, the loss evaluation allowance is calculated as lifetime expected credit losses until collection of accounts receivable. For lease investment assets, the loss evaluation allowance is calculated as lifetime expected credit losses until collection of lease investment assets. With regard to accounts receivable and lease investment assets of debtors who have no material problems in their business conditions, the expected credit loss rate is measured collectively, taking into account the past track record of bad debts and other factors. If there are material effects of changes in economic and other conditions, the loan loss provision ratio based on the past track record of bad debts will be adjusted and reflected in the forecast of present and future economic situations.

(Measuring expected credit loss for loans receivable related to the sales financing business)

If credit risk has not increased significantly since initial recognition, the loss evaluation allowance for loans receivable related to the sales financing business is calculated as of the end of the fiscal year by collectively estimating the expected credit loss rate for the following 12 months based on the past track record of bad debts and other factors. If there are material effects of changes in economic and other conditions, the loan loss provision ratio based on the past track record of bad debts will be adjusted and reflected in the forecast of present and future economic situations. On the other hand, if credit risk has increased significantly as of the end of the fiscal year since the initial recognition, the loss evaluation allowance for financial instruments is calculated by individually estimating the lifetime expected credit losses of collecting financial instruments based on the past track record of bad debts and the collectible amount in the future among other factors. Assets that are regarded as non-performing are recorded as credit impaired financial assets.

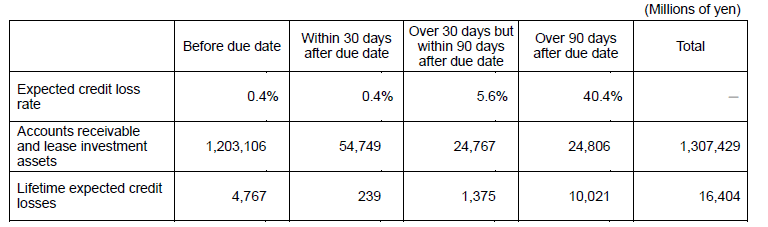

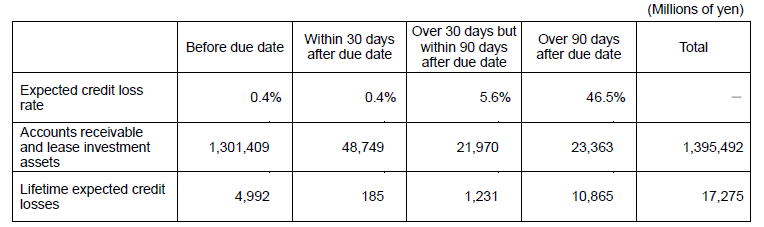

Expected credit loss of accounts receivable and lease investment assets for which simplified approaches are applied consist of the following.

FY2024 (As of March 31, 2024)

FY2025 (As of March 31, 2025)

Among financial assets, the general approach is applied mainly to loans receivable related to the sales financing business. The carrying amount of loans receivable related to the sales financing business, categorized by credit risk for its measurement, consists of the following.

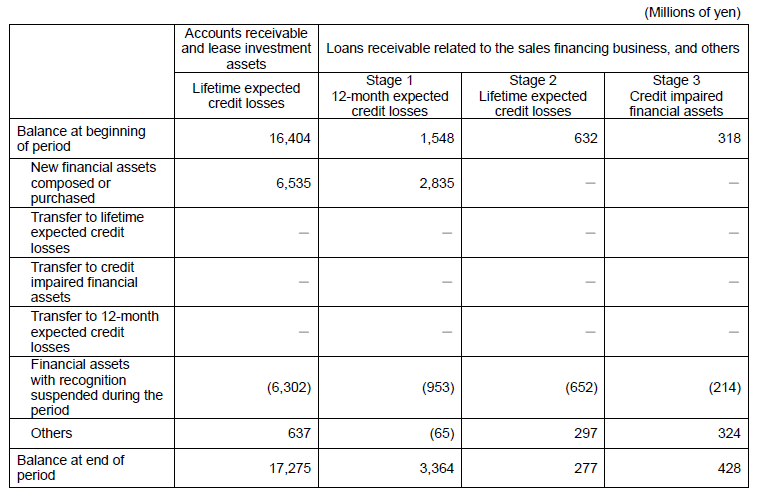

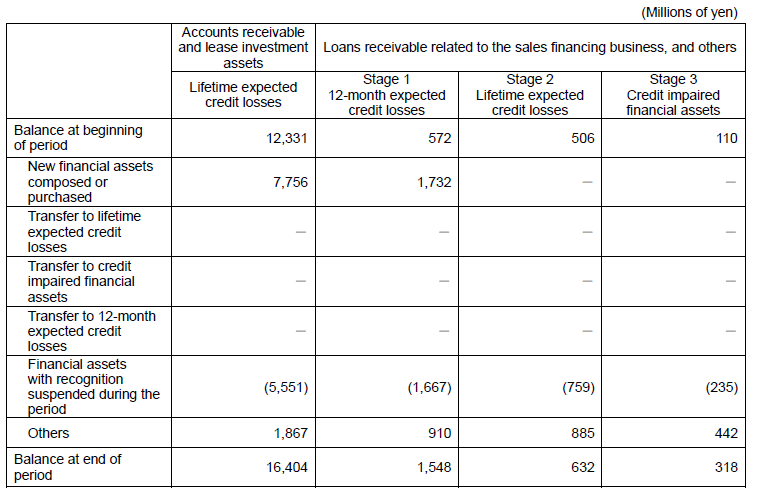

Changes in expected credit loss consist of the following.

FY2024 (As of March 31, 2024)

FY2025 (As of March 31, 2025)