Barloworld Limited – Annual report – 30 September 2021

Industry: manufacturing, distribution

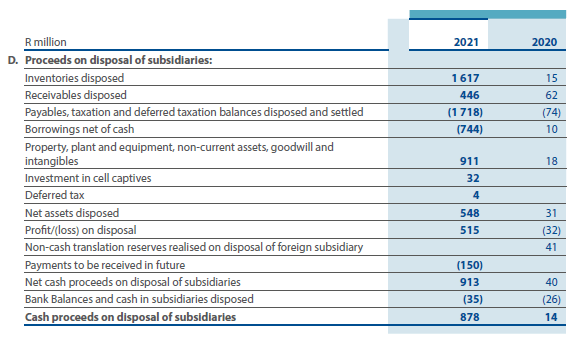

Notes to the consolidated cash flow statement (extract)

for the year ended 30 September 2021

Effective 1 June 2021 the group divested in the Motor Retail businesses to NMI Durban South Motors. Refer to note 22 for more detail.

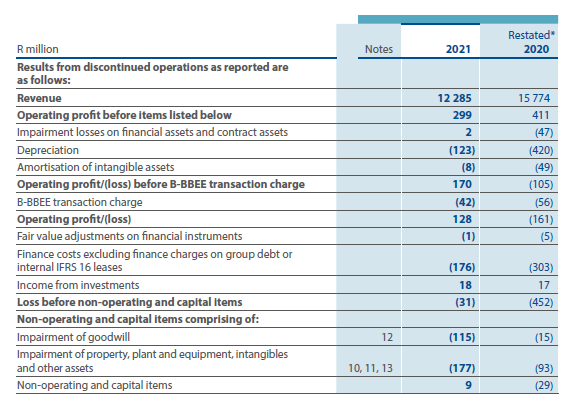

22.1 Discontinued operations

In January 2021 Barloworld announced that the Motor Retail business will be sold to NMI-DSM effective 1 June 2021 and in February 2021 the board took a firm decision to dispose of the Logistics business. Motor Retail and Logistics represents significant lines of business and have therefore been disclosed as discontinued operations at 30 September 2021, with the comparative September 2020 restated for the income statement and cash flow information only. The prior year statement of financial position is not restated in terms of IFRS 5 non-current assets held-for-sale and discontinued operations. The disposal of 50% of Motor Retail to NMI-DSM was concluded on the 1st of June 2021 and therefore 8 months of trading is reported in the discontinued operations for Motor Retail. Further details regarding the progress of the Logistics disposal are disclosed in note 42.

* The restatement is due to Motor Retail and Logistics being classified as discontinued operations (Refer to note 36).

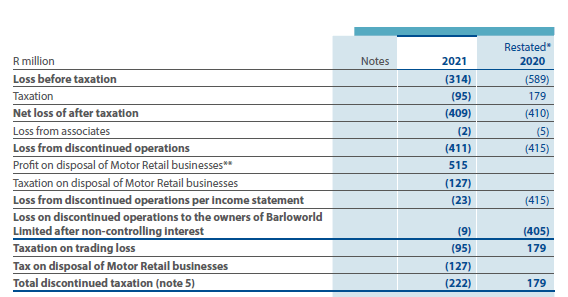

** On 1 June 2021 all conditions precedent to the disposal of Motor Retail to NMI had been fulfilled or waived. The total proceeds of the Disposal, subject to customary closing mechanics, was R1 062 million. Of this amount, R912 million was paid in various tranches until 31 July 2021. A further R150 million will be paid in two tranches, in equal instalments of R75 million each, on the first and second anniversary of the closing date of the disposal on 1 June each year. The net profit on disposal includes R12 million that relates to the recycling of the foreign currency translation reserves since acquisition.

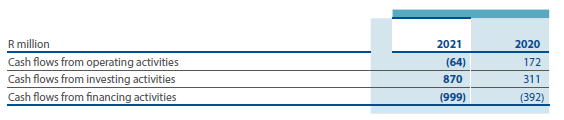

The cash flows from the discontinued operation are as follows:

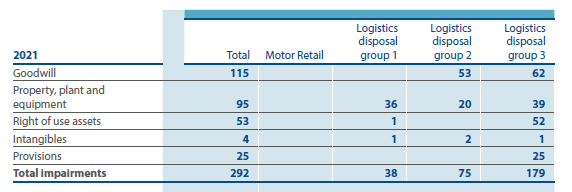

When entering into the sale of Logistics management believed they could sell the businesses as a whole as a going concern. The disposal process commenced with a broad set of interested parties. Non-binding proposals from the interested parties were received however due to the riots in July the overall sale of the business as a whole were impacted. Subsequently, management have identified three separate transactions to different buyers. Strong buyer interest has emerged through the process for the underlying discrete businesses. Each of the disposal group’s have a single coordinated plan to dispose of the businesses in Logistics. The table below depicts the disposal groups reported at 30 September.

The impairments related to the fair value less costs to sell the business are listed below:

The valuation techniques used to determine the fair value less costs to sell is a combination of the discounted cashflows, market multiple technique and offer prices received.

Logistics disposal group 1: Refrigerated transport business Logistics disposal group 2: Manline and Timber transport business that run the hazardous fuel, chemicals and forestry industry Logistics disposal group 3: Conglomerate of the warehouse and distribution, managed solutions, industrial projects and global solutions businesses.

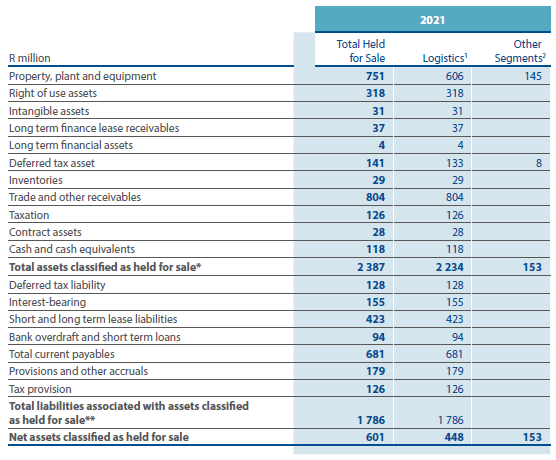

22.2 Assets classified as held for sale

The major classes of assets and liabilities classified as held for sale are as follows:

Note 1. This represents the assets and liabilities of the Logistics business classified as held for sale and a discontinued operation.

Note 2. The assets held for sale within the Other segments related to various properties that are in the process of being sold.

* Includes financial assets of R 990 million.

** Includes financial liabilities measured at amortised cost of R1 352 million

The valuation techniques used to determine the fair value less costs to sell is a combination of the discounted cashflows, market multiple technique and offer prices received. In terms of the valuation techniques the fair value of assets held for sale will be classified as level 3 as the valuation techniques are based on unobservable market data and adjusted for based on management’s experience and knowledge of the business. Management have considered and concluded that no reasonable change in the significant unobservable inputs would result in a material change in the fair value.

9. Earnings and headline earnings per share (extract)

9.1 Diluted weighted average number of shares

* The restatement is due to Motor Retail and Logistics being classified as discontinued operations (Refer to note 36).

9.2 Earnings per share

8. Taxation (extract)

3. Operating profit (extract)

# includes other B-BBEE charges related to the Khula Sizwe transaction of R3 million (FY2020: R13 million).

* The amortisation amount includes R62 million relating to customer relationship arising from the acquisition of Ingrain on 31 October 2020.

^ The restatement is due to Motor Retail and Logistics being classified as discontinued operations (Refer to note 22 and 36).

* The restatement is due to Motor Retail and Logistics being classified as discontinued operations (Refer to note 36).

2. Revenue (extract)

^ The restatement is due to Motor Retail and Logistics being classified as discontinued operations (Refer to note 22 and 36).

* Variable Leasing income earned mainly relates to excess kilometres and additional maintenance costs invoiced.

14. Investment in associates and joint ventures (extracts)

DETAILS OF MATERIAL ASSOCIATES

During the current year the Motor Retail business was sold to NMI Durban South Motors (Pty) Ltd. Refer note 22 and notes to the cash flow statement.