MTN Group Limited – Annual report – 31 December 2020

Industry: telecoms

11 CHANGE IN ACCOUNTING POLICIES

11.1 Release of foreign currency translation reserves

The Group implemented a voluntary accounting policy change relating to the release of FCTR.

In the first quarter of 2019, the Group announced that it will be optimising its portfolio through an asset realisation programme aimed at simplifying the Group, reducing risk and improving shareholder returns and in March 2020 the Group announced that this programme has been further expanded. The strategic intent to dispose of certain investments in subsidiaries and associates over the medium term has resulted in a review of the most appropriate approach in accounting for these disposals.

IAS 21 The Effects of Changes in Foreign Exchange Rates (IAS 21) requires that on the disposal of a foreign operation, the cumulative amount of the exchange differences relating to that foreign operation, recognised in OCI and accumulated in FCTR in equity, shall be reclassified from equity to profit or loss as a reclassification adjustment when the gain or loss on disposal is recognised. Two accepted methods exist for recycling FCTR where the investments are held by an intermediate parent with a different functional currency than the entity disposed of and the ultimate parent. These methods, that are referred to as part of the basis for conclusions (BC 35 – BC 39) in IFRIC 16 Hedges of a Net Investment in a Foreign Operation, are as follows:

- Step-by-step method – FCTR is recycled based on the appreciation or devaluation in the functional currency of the investment disposed of against the functional currency of the intermediate parent and translated into the functional currency of the ultimate parent.

- Direct method – FCTR is recycled based on the appreciation or devaluation in the functional currency of the investment disposed of against the functional currency of the ultimate reporting entity.

The Group has historically applied the step-by-step method on disposals to date. The functional currencies of some of the Group’s intermediate holding companies are US$ and, as a result, the FCTR reclassified on the step-by-step approach is determined based on the appreciation or devaluation of the currencies of the entities disposed of against the US$ and translated into the functional currency of the ultimate parent. As the Group’s functional and presentation currency is South African rand and the FCTR is based on the appreciation or devaluation of the South African rand against the equity of the underlying operations in the Group, the direct method provides a more reliable and relevant view of the gain or loss realised in the context of the Group’s South African rand (ZAR) functional currency. The Group has accordingly changed its accounting policy on the reclassification of FCTR on disposal of foreign operations held by an intermediate parent where the functional currency of the foreign operation and intermediate parent is different to that of the ultimate parent from the step-by-step method to the direct method.

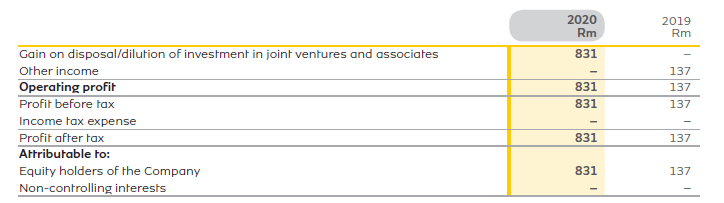

This change in accounting policy impacted the FCTR gains and losses reclassified to profit or loss in the current period on disposal of the Group’s investments in associates, Ghana InterCo and Uganda InterCo, and in the prior periods on disposal of the Group’s interest in foreign operations, as disclosed in the following tables.

11.1.1 Impact on financial statements

11.1.1.1 Consolidated income statement (extract)

11.1.1.2 Consolidated statement of comprehensive income (extract)

11.1.1.3 Consolidated statement of financial position (extract)

The impact of the change in policy on earnings per share is a 46 cents increase (2019: 7 cents increase) and diluted earnings a 46 cents increase (2019: 7 cents increase). The change in accounting policy had no impact on headline earnings or cash flows in the current or prior comparative period.