Impala Platinum Holdings Limited – Annual report – 30 June 2025

Industry: mining

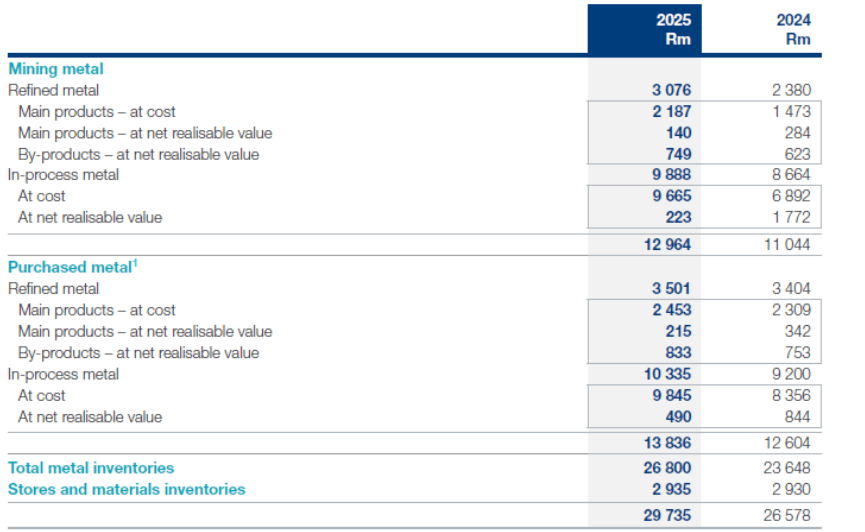

19. INVENTORIES

1 The fair value exposure on purchased metal was designated as a hedged item and is included in the calculation of the cost of inventories. The fair value exposure relates to adjustments made to commodity prices and US dollar exchange rates from the date of delivery until the final pricing date as per the relevant contract.

The net realisable value (NRV) adjustment included in the inventory value is impacted by the prevailing metal prices at the reporting date. The current year adjustment of R7 million (2024: R361 million) comprised R3 million (2024: R65 million) for refined metal and R4 million (2024: R296 million) for in-process metal.

Purchased metal consists of Impala Refining Services inventory.

Estimates and judgements

Inventory valuation

Metals classification between main and by-products is determined based on an assessment of the relative metal content for each segment. The relative metal content of Impala Canada, mining on the Canadian Shield, differs materially from what is mined in the Bushveld Complex in South Africa and the Great Dyke in Zimbabwe.

For purposes of inventory valuation, the southern African operations treat platinum, palladium, rhodium and nickel as main products and other precious and base metals produced, as by-products.

Impala Canada’s mining and processing activities do not form part of the southern African operations’ production process and its inventory is valued independently. Impala Canada classifies palladium as a main product and all other precious and base metals as by-products for inventory valuation purposes.

The average unit cost of normal pre-smelter production for mining metal is determined by dividing mining production cost with mining output on a 12-month rolling-average basis. The normal cost of purchased metal is measured based on the acquisition cost determined on a six-month rolling-average basis. The refining cost per unit (further conversion through smelter, base metal refinery and precious metal refinery) is determined by dividing normal refining costs with total output (both mining and purchased) on a 12-month rolling-average basis.

Refined ruthenium and iridium metal quantities on hand are valued using the lower of the actual stock quantity and three-months’ sales quantity.

In-process metal estimate adjustments

Quantities of recoverable metal are reconciled to the quantity and grade of ore input as well as the quantities of metal actually recovered (metallurgical balancing). The nature of this process inherently limits the ability to precisely monitor recoverability levels. As a result, the metallurgical balancing process is constantly monitored and the engineering estimates are refined based on actual results over time. The Group conducts periodic counts (usually annually) at the refineries to assess the accuracy of inventory quantities. Based on these counts, changes in engineering estimates of metal contained in-process resulted in a pre-tax increase in metal inventory of R858 million (2024: R968 million).

Tolerances of up to 2% of annual throughput of the main products are regarded as normal levels of estimation uncertainty in the measurement of work-in-progress quantities.

Accounting policy

Metal inventories

Costs incurred in the production process are appropriately accumulated as stockpiles, metal in-process and refined inventories.

In-process and refined inventories are carried at the lowest of its average cost of normal production and NRV. Costs relating to inefficiencies in the production process are charged to the income statement as incurred.

NRV tests are performed, at least, on each reporting date and represent the expected sales price of the product based on prevailing metal prices, less estimated costs to complete production and bring the product to sale.

The average cost of normal production includes total costs incurred on mining, smelting and refining, including depreciation, less net revenue from the sale of by-products at the point where by-products become separately identifiable, allocated to main products based on the relative sales value of main products sold. Stock values are adjusted for upstream intra-group transactions with subsidiaries and equity-accounted entities within the Group, eliminating intra-group profits in profit or loss and share of profit from equity-accounted entities, where applicable.

Refined by-products are valued at NRV and quantities of in-process metals are based on latest available assays. Recoverable metal quantities are continually tested for reasonableness by comparing the grade and quantity of ore input with the metal actually recovered. Engineering estimates are used to determine recoverable metal quantities and these estimates and the methodologies applied are improved on an ongoing basis. Metal quantity adjustments relating to prior years are adjusted without affecting production or impacting the calculation of unit cost per ounce produced during the current year.

Operating metal lease receipts are accounted for in profit or loss and the metal is carried as inventory.

Stores and materials

Stores and materials are valued at the lower of cost or NRV, on a weighted-average basis. Obsolete, redundant and slow-moving stores are identified and written down to NRV which is the estimated selling price in the ordinary course of business, less selling expenses.