Telefonica S.A. – Annual report – 31 December 2015

Industry: telecoms

[Note: see also 2016 extract]

Note 23. Discontinued operations

As detailed in Note 21.b, Telefónica, S.A. reached an agreement with Hutchison for the acquisition of Telefónica’s operations in United Kingdom. At the date of issuance of these consolidated financial statements Telefónica owns 100% of the shares of the companies under the scope of the sale agreement.

These companies have been classified as a disposal group held for sale and its operations qualified as discontinued operations (see Note 2).

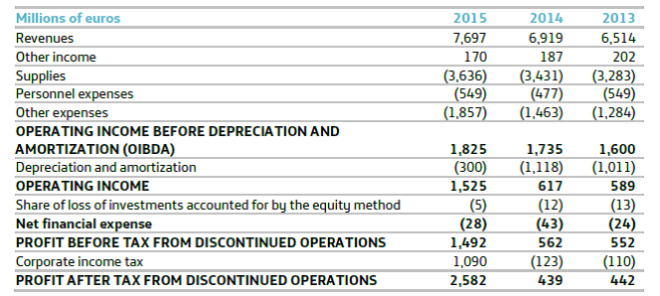

The following table provides additional information on our discontinued operations:

In 2015 the Group recognized, with a balancing entry in “Profit after tax from discontinued operations”, a deferred tax asset amounting to 1,789 million euros (see Note 17) resulting from the estimated difference in Telefónica, S.A. between the tax value and the agreed value in the sale of Telefónica’s operations in the United Kingdom, which are expected to materialize in a foreseeable future when the sale is executed. In accordance with IAS 12, a deferred tax asset shall be recognised for deductible temporary differences arising from subsidiaries to the extent that they will reverse in the foreseeable future and can be utilised. Being the sale of the Telefónica’s operations in United Kingdom highly probable, the Group understands that the tax loss will be materialized at the time of the sale (foreseeable future) and, at the same time, estimates that it will be utilised in the future (see Note 17). This impact was reduced by the amount corresponding to the tax amortization of goodwill generated in 2006 in the acquisition of the companies involved in the sale agreement and deducted until December 31, 2015, pending the final resolution in the European and Spanish courts on considering this incentive as State aid and / or deduction, amounting to 377 million euros (see Note 17).

“Other expenses” line in the above table includes the adjustment of the goodwill of Telefónica Digital Inc. amounting to 104 million euros (see Note 7).

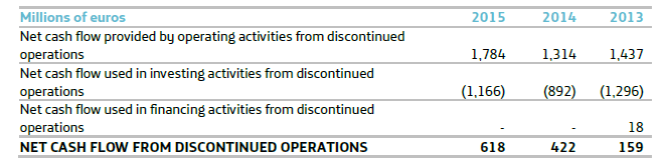

The detail of the cash flow from discontinued operations is as follows:

The detail of assets held for sale and associated liabilities, related to the sale agreement of Telefonica United Kingdom, is shown below:

Assets held for sale and associated liabilities shown in the table above are presented after intercompany eliminations with the other companies of Telefónica Group. Among intercompany eliminations in the consolidation process, is meaningful the liquidity deposited in Telfisa Global, B.V. amounting to 530 million euros as of December 31, 2015, and the loan granted by Telfin Ireland, Ltd. to O2 UK amounting to 804 million euros that could be capitalized before the closing of the transaction.

The following table summarizes the accumulated amounts (net of income tax impact) included in other comprehensive income:

Completion of the transaction is subject to, among other conditions, the approval of the applicable regulatory authorities and the obtaining of waivers to some contractual provisions affected by the sale, including those related to network alliances, as well as change of control provisions under certain contractual arrangements with third parties. The sale and purchase agreement establishes that the conditions must be satisfied by no later than June 30, 2016, this date may be extended until September 30, 2016 in specified circumstances (see Note 21).

Note 18. Revenue and expenses (extract)

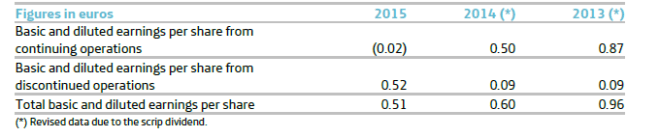

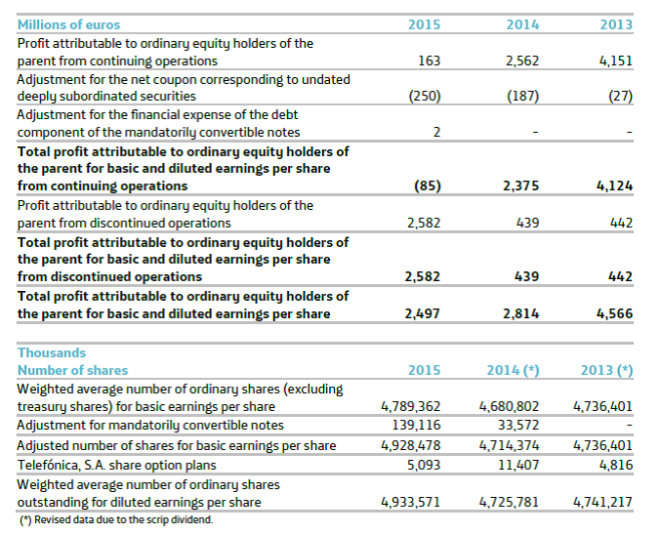

Earnings per share

Basic earnings per share amounts are calculated by dividing (a) the profit for the year attributable to equity holders of the parent, adjusted for the net coupon corresponding to the undated deeply subordinated securities and for the interest cost accrued in the period in relation to the debt component of the mandatorily convertible notes of the parent company issued in 2015 (see note 12) by (b) the weighted average number of ordinary shares outstanding during the year plus the weighted average number of ordinary shares that would be issued upon the conversion of the said mandatorily convertible notes from the date of their issuance.

Diluted earnings per share amounts are calculated by dividing the net profit for the year attributable to ordinary equity holders of the parent, adjusted as described above, by the weighted average number of ordinary shares adjusted as described in the preceding paragraph, plus the weighted average number of ordinary shares that would be issued on the conversion of all the dilutive potential ordinary shares into ordinary shares.

Both basic and diluted earnings per share attributable to equity holders of the parent are calculated based on the following data:

For the purposes of calculating the earnings per share ratios (basic and diluted), the weighted average number of shares outstanding is retrospectively adjusted for transactions that have changed the number of shares outstanding without a corresponding change in equity, as if such transactions had occurred at the beginning of the earliest period presented. For instance, the bonus share issues carried out to meet the scrip dividends paid in 2015 and 2014 have been taken into account (see Note 12). Basic and diluted earnings per share attributable to equity holders of the parent are as follows: