Avon Rubber p.l.c. – Annual report – 30 September 2021

Industry: manufacturing

7.6 Post balance sheet events

On 12 November 2021 the Group announced the next-generation VTP ESAPI body armor product had failed first article testing. This followed a similar result in December 2020 for the legacy DLA ESAPI body armor product. It was also announced that the Group is experiencing further delays in achieving final product approval for the DLA ESAPI product following the successful completion of ballistic testing in August 2021, thereby pushing expected revenues from the second quarter into the third quarter of FY22. As a result, the Board conducted an in-depth strategic review of the armor business.

The failure of the VTP ESAPI body armor product is considered an adjusting event that provides evidence of conditions that existed at the end of the reporting period on the basis that the product was in its current condition for testing at the reporting date. As such the Group performed an impairment review of assets at 30 September 2021 removing all future revenue for VTP ESAPI body armor. The review also incorporated reduced revenue expectations for DLA ESAPI in line with minimum volumes for the base and two extension years, given the identified uncertainty of timing of the approval following the already experienced delays during FY21, and uncertainty over whether the customer would extend the contract. The DLA revenue assumed reflects the Group’s expectations at 30 September 2021, and is not related to post balance sheet events.

The review resulted in total non-current asset impairments of $45.1 million in respect of assets relating to the armor business acquired from 3M as part of the ballistic protection acquisition. In addition, inventory provisions of $1.7 million were recognised against VTP ESAPI armor materials. Offsetting these charges, a gain of $15.7 million was recognised to reduce the net present value of the contingent consideration payable to 3M as a result of the reduced revenue expectations from the DLA ESAPI body armor contract.

The strategic review of the armor business concluded it is in the best interests of our stakeholders as a whole to undertake an orderly wind-down of trading. As a result the Group expects to incur net cash costs of closure and right-sizing the retained organisation of between $3 to $5 million over the next two years. Given the strategic review concluded after the reporting period it is considered a non-adjusting event, and the provision for closure costs will therefore be charged in the 2022 financial year as an exceptional item.

Significant accounting judgements and estimates (extract)

Judgements and estimates (extract)

Development costs

The Group capitalises the development costs of new products and processes as intangible assets or property, plant and equipment. Initial capitalisation and any subsequent impairment are based on management’s judgement of technological and economic feasibility, including regulatory approvals required and forecast customer demand. In determining the amounts to be capitalised the Group makes estimates regarding the expected future cash generation of the project, discount rates to be applied and the expected period of benefits. If either technological or economic feasibility is not demonstrated then the capitalised costs will be written off to the income statement.

Significant judgements in the period included:

- A judgement on technical feasibility and therefore future successful first article testing and product approval for the next generation Integrated Head Protection System (‘IHPS’).

- A judgement that following the failure of first article testing on the DLA ESAPI body armor, it remained appropriate to continue recognising the previously capitalised costs and further costs to achieve final product approval were appropriate to capitalise.

- A judgement that it remained technically feasible to achieve first article testing and product approval for VTP ESAPI body armor, given the failure on the DLA ESAPI, and therefore continue to capitalise costs, prior to the failure in testing post year end.

Significant estimates made and sensitivity in respect of the assumptions used that could have a significant impact on the carrying value of assets in determining the carrying amount of development costs at the balance sheet date are disclosed in note 3.1.

Adjusting events

The Group considers when events after the end of the reporting period should be adjusted in the financial statements. Adjusting events are those providing evidence of conditions existing at the end of the reporting period, whereas non-adjusting events are indicative of conditions arising after the reporting period. The treatment of the VTP ESAPI body armor product failure as an adjusting event was considered a significant judgement in the period. See note 7.6 for further details and note 3.1 for the impact of this event.

3.1 Intangible assets (extract)

Armor related impairments

On 12 November 2021 the Group announced the next-generation VTP ESAPI body armor product had failed first article testing. This followed a similar result in December 2020 for the legacy DLA ESAPI body armor product. It was also announced that the Group is experiencing further delays in achieving final product approval for the DLA ESAPI product following the successful completion of ballistic testing in August 2021, thereby pushing expected revenues from the second quarter into the third quarter of FY22.

The failure of the VTP ESAPI body armor product is considered an adjusting event that provides evidence of conditions that existed at the end of the reporting period (see note 7.6). As such the Group’s impairment review of assets at 30 September 2021 included the removal of all future revenue for VTP ESAPI body armor. The impairment review also incorporated reduced revenue expectations for DLA ESAPI in line with minimum volumes for the base and two extension years, given the increased uncertainty of timing of the approval following the already experienced delays during FY21, and uncertainty over whether the customer would extend the contract. The DLA revenue assumed reflects the Group’s expectations at 30 September 2021, and is not related to post balance sheet events.

Impairment testing at 30 September 2021 for assets related to the armor business has been performed at multiple levels as these assets generate cash inflows along with assets in other parts of the Group. The levels the impairment testing has been performed as follows:

1) Product level – VTP ESAPI and DLA ESAPI are both separate products. Included in these CGUs are development expenditure, tangible assets related to the product group, inventory and acquired intangibles where associated with the development project.

2) At the armor business level – this includes the VTP ESAPI and DLA ESAPI CGUs, and other armor specific assets such as acquired intangibles as well as PPE (including Right of Use Assets) which solely relate to the entire armor business.

3) Ballistic level – this includes the armor business assets, and the assets related to the acquired Ceradyne helmet business.

4) Avon Protection business level – this includes ballistic assets and other assets that make up the Avon Protection operating segment, including goodwill relating to the Ceradyne acquisition (see below).

The impairment review resulted in total non-current asset impairment of $45.1 million in respect of assets relating to the Ceradyne armor business acquired from 3M as part of the ballistic protection acquisition – these arose at the individual product level and the armor business level. In addition, inventory provisions of $1.7 million were recognised against VTP ESAPI armor materials. Offsetting these charges, a gain of $15.7 million was recognised to reduce the net present value of the contingent consideration payable to 3M as a result of the reduced revenue expectations from the DLA ESAPI body armor contract.

The pre tax discount rates used in determining the value in use at each level were between 8.9% on the Avon Protection business level and 62.3% at the product level, reflecting the level of uncertainty associated with each of the asset groups reviewed for impairment.

There was no further impairment when subsequently testing Ballistic protection level assets and finally Avon Protection CGU assets against expected values in use. Goodwill relating to the Ceradyne acquisition of $28.0 million and the Ceradyne helmet intangible assets with a carrying value of $28.9 million have therefore been unaffected by the impairment review.

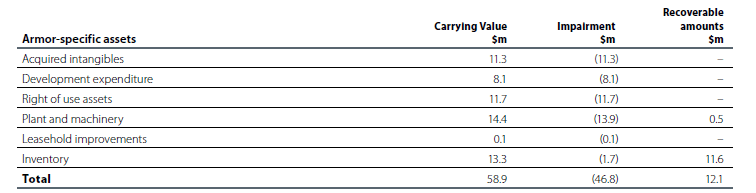

The impairments have fully written down armor assets to recoverable amounts. The overall armor asset base, impairments charged and remaining recoverable amounts are summarised as follows:

Recoverable amounts for plant and machinery are based on fair value less costs to sell. These are considered level 2 assets in a fair value hierarchy, valued based on market data for resale values on disposal. The recoverable amount for all other assets is based upon the relevant value in use. Remaining non-current assets have both fair value less costs to sell and value in use of nil.

Changes in the discount rate or growth rate utilised in the product level and armor level reviews would not materially change the total impairment. Impairments were recognised through general and administrative expenses in the Consolidated Statement of Comprehensive Income.

The failures in testing within the armor business do not impact respiratory and head protection products, and the Group remains confident future regulatory approvals will be obtained for these businesses as required.