Rio Tinto plc – annual report – 31 December 2025

Industry: mining

22 Leases

Recognition and measurement

IFRS 16 applies to the recognition, measurement, presentation and disclosure of leases. Certain leases are exempt from the standard, including leases to explore for or use minerals, oil, natural gas and similar non-regenerative resources. We apply the scope exemptions in paragraphs 3(e) and 4 of IFRS 16 and do not apply the standard to leases of any assets which would otherwise fall within the scope of IAS 38 “Intangible Assets”.

A significant proportion of our lease arrangements relate to dry bulk vessels and office properties. Other leases include land and non-mining rights, warehouses, ports, equipment and vehicles.

We recognise all lease liabilities and corresponding right-of-use assets on the balance sheet, with the exception of short-term (12 months or fewer) and low-value leases, where payments are expensed as incurred. Lease liabilities are recorded at the present value of fixed payments; variable lease payments that depend on an index or rate; amounts payable under residual value guarantees; and extension options expected to be exercised. Where a lease contains an extension option that we can exercise without negotiation, lease payments for the extension period are included in the liability if we are reasonably certain that we will exercise the option. Variable lease payments not dependent on an index or rate are excluded from the calculation of lease liabilities at initial recognition. Payments are discounted at the incremental borrowing rate of the lessee, unless the interest rate implicit in the lease can be readily determined. For lease agreements relating to vessels, ports and properties, non-lease components are excluded from the future lease payments and recorded separately within operating costs as services are being provided. The lease liability is measured at amortised cost using the effective interest method. The right-of-use asset arising from a lease arrangement at initial recognition reflects the lease liability, initial direct costs, lease payments made before the commencement date of the lease, and capitalised provision for dismantling and restoration of the underlying asset, less any lease incentives.

We recognise depreciation on right-of-use assets and interest on lease liabilities in the income statement over the lease term. Repayments of lease liabilities are separated into a principal portion (presented within financing activities) and an interest portion (which the Group presents in operating activities) in the cash flow statement. Payments made before the commencement date are included within financing activities unless they in substance represent investing cash flows, for example where pre-commencement cash flows are significant relative to aggregate cash flows of the leasing arrangement.

Other relevant judgements Accounting for renewable power purchase agreements

We have to apply judgement for certain contractual arrangements, such as renewable energy power purchase agreements (PPAs), in evaluating whether we have the right to obtain substantially all of the economic benefits from the use of the renewable energy assets, including the right to obtain physical energy these assets generate. Based on our evaluation, we determine whether an arrangement is a lease, an executory contract or a derivative. An immaterial amount was recognised as a lease at both 31 December 2025 and 31 December 2024 for a fixed component of the QMM renewable PPA. The Amrun and Jinbi renewable PPAs are leases which have not yet commenced, and are included in our decarbonisation capital commitments (note 37).

Lessee arrangements

We have made the following payments during the year associated with leases:

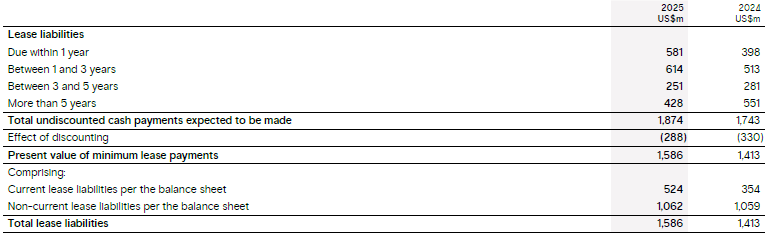

Lease liabilities

The maturity profile of lease liabilities recognised at 31 December is:

At 31 December 2025, commitments for leases not yet commenced were US$785 million (2024: US$405 million) and commitments relating to short-term leases which had already commenced were US$217 million (2024: US$182 million). These commitments are not included in the maturity profile table above.

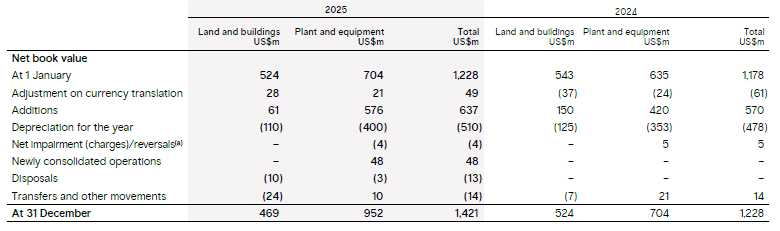

13 Property, plant and equipment (extract)

Right-of-use assets – leased

(a) Refer to note 4 for details.

The leased assets of the Group include land and buildings (mainly office buildings) and plant and equipment, the majority of which are marine vessels. Lease terms are negotiated on an individual basis and contain a wide range of terms and conditions. Right-of-use assets are depreciated on a straight line basis over the life of the lease, taking into account any extensions that are likely to be exercised.

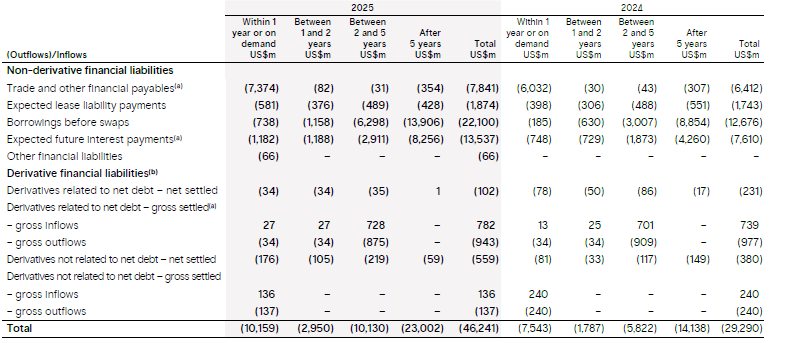

Our capital and liquidity (extract)

Financial liability analysis

In the table below, we summarise the maturity profile of our financial liabilities on our balance sheet based on contractual undiscounted payments as at 31 December. When the amount payable is not fixed, the amount disclosed is determined by reference to the conditions existing at the end of the reporting period. This will, therefore, not necessarily agree with the amounts disclosed as the carrying value.

a) The interest payable at the year end is removed from trade and other financial payables and shown within expected future interest payments and derivatives related to net debt. Interest payments have been projected using interest rates applicable at the end of the applicable financial year. Where debt is subject to variable interest rates, future interest payments are subject to change in line with market rates.

(b) The maturity grouping is based on the earliest payment date.

Our weighted average debt maturity including leases and derivatives related to debt was approximately 11 years (2024: 11 years).

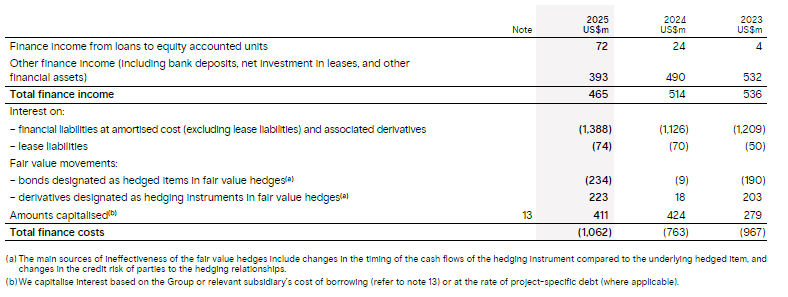

9 Finance income and finance costs

7 Net operating costs (excluding items disclosed separately)

(c) In 2025, other external costs includes US$1,059 million (2024: nil) of costs due to the impact of tariffs imposed on sales to the US, US$269 million (2024: US$217 million, 2023: US$269 million) of short-term lease costs and US$84 million (2024: US$46 million, 2023: US$40 million) of variable lease costs recognised in the income statement in accordance with IFRS 16 “Leases”. Refer to note 22.