Acacia mining plc – Annual report – 31 December 2018

Industry: mining

2. Significant accounting policies (extract)

In assessing the Acacia Group’s going concern status the Directors have taken into account the impact of the concentrate export ban on ongoing operations as well as the following factors and assumptions: the current cash position; the latest mine plans, the short-term gold price, and Acacia Group’s capital expenditure and financing plans. In addition, the Directors have considered a range of scenarios around the various potential outcomes for the resolution of the current operating challenges in Tanzania in the circumstances, including the cash flow impact of an extended concentrate export ban; and the potential impacts of the timing and final terms of any comprehensive settlement which might be approved by the Company which reflect key terms of the framework announcements made by Barrick and the Government of Tanzania (“GoT”) in October 2017, including the lifting of the concentrate export ban and staged payments of US$300 million relating to historical tax matters. In addition, the Directors have assumed that the Group will not be required to settle its current outstanding borrowing obligations and will repay these in accordance with the current terms of the relevant agreements. After making appropriate enquiries and considering the uncertainties described above, the Directors consider that it is appropriate to adopt the going concern basis in preparing the consolidated financial statement however have concluded that the combination of the above circumstances represents a material uncertainty that may cast significant doubt on the Group’s ability to continue as a going concern. The consolidated financial statement does not include any adjustments that would result if the Group was unable to continue as a going concern should the assumptions referred to above prove not to be correct.

6. Impairment assessment

In accordance with IAS 36 “Impairment of assets” and IAS 38 “Intangible Assets” a review for impairment of goodwill is undertaken annually, or at any time an indicator of impairment is considered to exist, and in accordance with IAS 16 “Property, plant and equipment” a review for impairment of long-lived assets is undertaken at any time an indicator of impairment is considered to exist.

At the end of the reporting period, there remained a number of potential triggers for impairment testing, including the ongoing uncertainty surrounding a potential resolution of the Company’s disputes with the GoT, the revised Bulyanhulu business model, the updated geological models at North Mara and Bulyanhulu and the fact that the Company’s market capitalisation has been lower than its carrying value during the current reporting period.

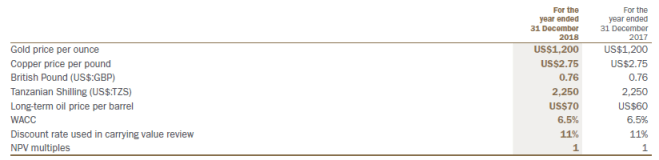

As a result, the Group has undertaken a carrying value assessment of its affected CGUs and long life intangible assets. The assessment compared the recoverable amount of CGU to the carrying value of the CGUs. The recoverable amount of an asset is assessed by reference to the higher of value in use (“VIU”), being the net present value (“NPV”) of future cash flows expected to be generated by the asset, and fair value less costs to dispose (“FVLCD”). The FVLCD of a CGU is based on an estimate of the amount that the Group may obtain in a sale transaction on an arm’s length basis. There is no active market for the Group’s CGUs. Consequently, FVLCD is derived using discounted cash flow techniques (NPV of expected future cash flows of a CGU), which incorporate market participant assumptions. Cost to dispose is based on management’s best estimates of future selling costs at the time of calculating FVLCD. Costs attributable to the disposal of a CGU are not considered significant.

For the purpose of carrying value assessments in accordance with applicable accounting standards, management has based its calculation of future cash flows of the affected CGUs by reference to the key terms of the Framework announcements by Barrick and by the GoT in October 2017. Based on Barrick’s announcements, and absent any changes in its position in discussions and exchanges with Acacia, Acacia understands that it remains Barrick’s belief that it will be able to agree with the GoT a detailed proposal for a comprehensive settlement of the situation, and that this will be in a form that Barrick could recommend to Acacia for review. Key assumptions applied in these calculations include a 50% economic share of future economic benefits for the GoT in the form of taxes, royalties and a 16% free carry interest in the CGUs, as well as a US$300 million payment in relation to historical tax claims paid in instalments as concentrate sales recommence. In addition the Framework announcements provided for Acacia to contribute certain monies to fund specific projects in Tanzania. With no updated information from Barrick, management has had to make a best estimate of what can reasonably be assumed for timing of conclusion of discussions between Barrick and the GoT and an agreement of a proposal to be put to the Company for review, with consequent timing for the commencement of concentrate sales and potential resumption of underground mining at Bulyanhulu. Management considers that it is reasonable for review purposes to assume a six month prolongation (to the end of H1 2019) to the discussions between Barrick and the GoT, and that in these circumstances there would be a further three to six months delay thereafter for the resumption of concentrate sales and exports, with concentrate revenues commencing in Q1 2020 and the resumption of production from underground mining at Bulyanhulu in late 2020. VAT refunds are assumed to recommence and historic carried forward tax losses are assumed to continue to be available to offset against future taxable profits from 1 January 2020.

Acacia has been providing support to Barrick to seek to ensure that they can have informed discussions with the GoT, but has not received for review a detailed proposal that has been agreed between Barrick and the GoT, and therefore no conclusions can be made by Acacia as to whether any particular terms of settlement would be approved by Acacia. In the meantime, Acacia continues to reserve its rights including under our Mineral Development Agreements, the disputes between Acacia and the GoT have not yet been resolved, and PML and BGML remain in international arbitration with the GoT. Acacia continues to prefer a negotiated resolution, but there remain a range of potential outcomes to the current situation.

Acacia considers that, in conducting the review of carrying values in accordance with applicable accounting standards as at 31 December 2018, the discount rate used should: (a) reflect the uncertainty around the final terms of any comprehensive settlement that might be agreed or whether settlement will be reached at all, and (b) best reflect the potential reduction in value as a result of the proposed 16% free carry interest for the GoT which cannot otherwise be included in calculations of value at a CGU level conducted on a 100% basis. Therefore, for the purposes of the carrying value review of the affected CGUs, we have kept a discount rate of 11% compared to Acacia’s calculated weighted average cost of capital of 6.5% (2017: 11%).

Using the latest information received and updated with the latest understanding of the framework agreement between Barrick and the GoT, the carrying values of all our assets are below the Company’s view of its recoverable values.

The carrying value for the Group is now approximately US$1.1 billion, made up of US$0.6 billion for Bulyanhulu, US$0.3 billion for North Mara and US$0.2 billion for Buzwagi.

During the year, OreCorp, Acacia’s JV partner in the Nyanzaga Project in Tanzania, executed its option under the earn-in agreement to increase its stake to 51% in the project through the payment of US$3 million to Acacia. Further to that, Acacia signed a completion agreement to sell its remaining 49% stake to OreCorp for US$7 million and a net smelter royalty capped at US$15 million based on future production. In line with the applicable accounting standard and driven by the uncertainty surrounding the current environment, management did not recognise an asset for the right to the royalty. As a result of the agreement, and management’s commitment to a sale, Acacia expects to recover the value of the asset through sale and not through value in use and as such has valued the asset at fair value less costs to sell of US$10 million and recorded an impairment charge of US$24.2 million and reclassified the associated non-current assets and liabilities to held for sale on the balance sheet.

In addition, as part of the year-end carrying value assessment we have impaired US$3.2 million of property plant and equipment mainly relating to previously capitalised drilling costs in Tanzania and US$1.5 million relating to other historical exploration assets.

The impairment charges recognised in the income statement for the periods ended 31 December 2018 and 31 December 2017 comprise the following:

1 The Nyanzaga exploration property & other exploration assets are located in Tanzania. Acquired mineral interests /exploration and evaluation assets are classified as intangible assets and have indefinite useful lives.

Management’s view is that the recoverable values are most sensitive to changes in the assumptions around gold prices, discount rates and the timing of the resolution of the export ban. As a result, sensitivity calculations were performed for these assumptions. The sensitivity analysis is based on a decrease in the long-term gold price of US$100 per ounce, and an increase in the discount rate of 1%, and a delay of resolution by 12 months.

Under these scenarios, a reasonably possible decrease in the gold price assumption of US$100 per ounce would result in an impairment charge, net of tax, of approximately US$17 million at Buzwagi while North Mara and Bulyanhulu remain unaffected.

A reasonably possible increase in discount rate of 1% would not result in any additional impairment charges.

A further delay of 12 months in the resolution of the export ban will also not result in any additional impairment charges.

Should a negotiated resolution of the current situation not eventuate, the recoverable values of the identified CGUs may be further impacted, and these will be reviewed at such time.

34. Commitments and contingencies (extract)

The Group is subject to various laws and regulations which, if not observed, could give rise to penalties. As at 31 December 2017, the Group has the following commitments and/or contingencies:

a) Legal contingencies

As at 31 December 2018, the Group was a defendant in a number of lawsuits. The plaintiffs are claiming damages and interest thereon for the alleged loss caused by the Group due to one or more of the following: unlawful eviction, termination of services and/or, non-payment for services, defamation, negligence by act or omission in failing to provide a safe working environment, unpaid overtime, public holiday compensation and various other commercial/project disputes. At present, Acacia considers the majority of cases to be without merit and therefore the likelihood of any material unfavourable outcome is remote and therefore no contingency is required.

b) Tax-related contingencies

The TRA has issued a number of tax assessments to the Group related to past taxation years from 2002-onwards. The Group believes that the majority of these assessments are incorrect and has filed objections and appeals accordingly in an attempt to resolve these matters by means of discussions with the TRA or through the Tanzanian appeals process. Overall, it is the current assessment that the relevant assessments and claims by the TRA are without merit. The claims include a TRA assessment to the value of US$41.3 million for withholding tax on certain historic offshore dividend payments paid by Acacia Mining plc to its shareholders in 2010 to 2013. Acacia is appealing this assessment on the substantive grounds that, as an English incorporated company, it is not resident in Tanzania for taxation purposes. The appeal is currently pending at the Court of Appeal. In addition, the Company has raised certain tax provisions amounting to US$300 million in aggregate, based on the potential impact of a comprehensive settlement of all outstanding tax disputes, including, according to Barrick, historic tax claims, reflecting the key terms of the Framework announcements by Barrick and the GoT in October 2017. Refer to note 9 for further information.

c) Regulatory contingencies

In 2018, and particularly during the final quarter of the year, the operating environment became increasingly challenging for Acacia with criminal charges brought by the GoT against three current Acacia employees and a former employee, three of whom continue to be held under non-bailable offences.

On 10 October 2018, one of the Group’s employees in Tanzania, a South African national, was charged by the Tanzanian Prevention and Combating of Corruption Bureau (PCCB) with an offence under the Tanzanian Prevention and Combating of Corruption Act. The employee pleaded not guilty and was granted bail. The charges related to the historical activities of a Land Task Force (LTF) conceived and agreed between the GoT and North Mara Gold Mine Limited (NMGML) in 2012 to create a transparent, safe, fair and inclusive process for valuing land that might be purchased by agreement around the North Mara mine, and which operated between 2013 and 2015. The allegations made by the PCCB are denied and the charges are being defended.

On 17 October 2018 a current and a former employee of the Company’s Tanzanian businesses, together with three individual companies, were charged by the PCCB with a number of different offences, including breaches of the Tanzanian Anti-Money Laundering Act. A total of 39 charges were brought, either against the current and former employee and/or against one or more of the Company’s operating subsidiaries in Tanzania, Pangea Minerals Limited (“PML”), Bulyanhulu Gold Mine Limited (“BGML”) and North Mara Gold Mine Limited (“NMGML”), as well as a Canadian company,

Explorations Minieres du Nord Ltd. On 23 October 2018, a senior manager of one of the Company’s Tanzanian businesses, a Tanzanian national, was also arrested and charged by the PCCB. The senior manager was charged as an additional accused to some (but not all) of the 39 criminal charges brought by the PCCB on 17 October. Each of the companies and the two current employees and the former employee pleaded not guilty to all charges. The Company notes with concern that under Tanzanian law, offences under the Anti-Money Laundering Act are not bailable, and, accordingly, the accused have not been released on bail. The majority of the 39 charges and allegations brought by the PCCB appear to relate to the historical structuring and financing of PML, BGML and NMGML dating back as far as 2008, prior to the creation of the Acacia Group. The charges are wide ranging and include: tax evasion; conspiracy; a charge under organised crime legislation; forgery; money laundering and corruption. The great majority of the allegations in the criminal proceedings by the GoT relate to matters already being considered in the arbitrations commenced by BGML and PML in July 2017 regarding their disputes with the GoT under their respective MDAs, which are progressing towards a hearing and in which the GoT are fully participating. These allegations and charges against the group and current and former employees are refuted and are being defended. Acacia considers the allegations to be without merit and that the likelihood of any material unfavourable outcome is remote, and no contingency has been made.

In addition, on 17 December 2018 the Company issued a news release noting media speculation claiming an investigation into the Company by the Serious Fraud Office (“SFO”). The Company confirmed that it was not aware that the SFO was investigating the Company, but that the Company had been in contact with the SFO about the allegations of corrupt activities which are the subject of criminal proceedings in Tanzania. This position remains unchanged. The Company has provided information to the SFO and will continue to do so, but has not been notified that the SFO has commenced a criminal investigation.

INDEPENDENT AUDITORS’ REPORT TO THE MEMBERS OF ACACIA MINING PLC (extract)

Emphasis of matter – Group and parent company – Impact of mineral concentrate export ban and negotiation with the Government of Tanzania

In forming our opinion on the group financial statements, which is not modified, we draw attention to Notes 2, 6 and 34 to these financial statements, which describe the material uncertainties related to the impact of the mineral concentrate export ban and negotiations with the Government of Tanzania on the Group’s and parent company’s assets, liabilities and cash flows. Our opinion is not modified in respect of these matters.

In forming our opinion on the group financial statements, which is not modified, we have considered the adequacy of the disclosure made in note 2 to the financial statements concerning the group’s ability to continue as a going concern.

The impact of the mineral concentrate export ban and negotiation with the Government of Tanzania, along with the other matters explained in note 2 to the financial statements, indicate the existence of a material uncertainty which may cast significant doubt about the group’s ability to continue as a going concern. The group financial statements do not include the adjustments that would result if the group was unable to continue as a going concern.

Explanation of material uncertainty

Note 2 to the financial statements details the directors’ disclosures of the material uncertainties relating to going concern. In addition, the disclosures included in Note 6 to the financial statements provide further detail relating to the status and potential impact of the ongoing mineral concentrate export ban and negotiation with the Government of Tanzania on the going concern status of the Group and parent company.

In forming their conclusions regarding going concern of the Group and parent company, and as described in Note 2, the directors have considered, but not limited to, the following matters:

– the impact of the ban on-ongoing operations;

– the current cash position;

– the latest mine plans and a range of scenarios around the various options under these circumstances, including the cash flow impact of an extended concentrate export ban; and the potential impacts of the timing and final terms of any comprehensive settlement which might be approved by the parent company, including the lifting of the concentrate export ban and staged payments of US$300 million relating to historical tax matters;

– the short-term gold prices and market expectations for the same in the medium-term; and

– Acacia Group’s capital expenditure and financing plans.

In addition, the directors have assumed that the Group will not be required to settle its current outstanding borrowing obligations and will repay these in accordance with the current terms of the relevant agreements. Given the risks associated with the impact of the mineral concentrate export ban and negotiations with the Government of Tanzania, the directors have drawn attention to this in disclosing a material uncertainty relating to going concern in the basis of preparation to the Annual Report.

RISK MANAGEMENT (extract)

Assessment of viability

In addition to annual risk management reviews, we also conducted additional reviews relating to business viability relevant to our assessment of Acacia’s ongoing viability and the related confirmations required to be made in this regard.

In assessing the viability of the business the Directors have taken into account the developments and trends across the Company’s principal risks and related ongoing uncertainties affecting our business and in particular the ongoing political, legal and regulatory developments affecting our operating environment, as explained in this Risk Management section and throughout this Annual Report.

In addition, the Directors’ consideration of viability is subject to all considerations and assumptions taken into account as part of the 2018 carrying value review outlined on page 81 and the going concern statement on page 55 of this Annual Report.

After making appropriate enquiries and considering the uncertainties described above, the Directors have a reasonable expectation that the Acacia Group will continue to operate and meet its liabilities, as they fall due, for the next three years should the operating environment not further deteriorate. However they have concluded that the combination of the above circumstances represents a material uncertainty that may cast significant doubt on the Group’s ability to remain viable.

We continue to assess viability over a three-year assessment period on the basis of the key components and criteria that continue to underpin the Acacia Group’s life of mine planning process. This process is built on a mine by mine basis using a detailed physical and financial model.

It makes certain assumptions as regards the ongoing gold price environment and the performance level of each mine. Each component of the plan is then stress tested for market sensitivities as part of ongoing reviews. The key components of the plans, associated principal risks and relevant scenario testing to this planning process are reviewed by the Directors at least annually.

In addition, the life of mine planning process is underpinned by regular Board briefings as part of ongoing periodic operational performance reviews and the discussion of any operational initiatives to be undertaken in the ordinary course of business. In addition to this and in light of the challenges faced in 2018 management has enhanced its liquidity assessments for going concern and viability purposes.