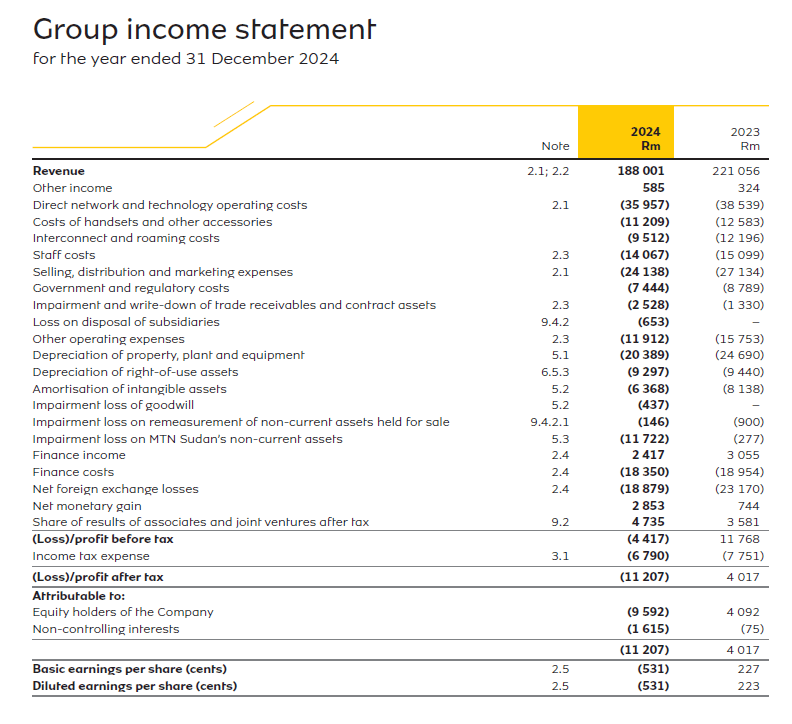

MTN Group Limited – Financial report – 31 December 2024

Industry: telecoms

7 FINANCIAL RISK (extracts)

7.1 Financial risk management and financial instruments (extracts)

Impairment

Under IFRS 9 the Group calculates its allowance for credit losses as ECLs for financial assets measured at amortised cost, debt investments at FVOCI and contract assets (unbilled handset component for contract). ECLs are a probability weighted estimate of credit losses. Credit losses are measured as the present value of all cash shortfalls (i.e. the difference between the cash flows due to the Group in accordance with the contract and the cash flows that the Group expects to receive). ECLs are discounted at the original effective interest rate (EIR) of the financial asset.

To calculate ECLs the Group segments/groups trade receivables by customer type i.e., interconnect, Enterprise Business Unit (EBU), mobile (billed handset and network services component for contracts) etc. The Group applies the simplified approach to determine the ECL for trade receivables and contract assets. This results in calculating lifetime ECLs for trade receivables and contract assets. ECLs for trade receivables is calculated using a provision matrix. For contract assets and mobile trade receivables relating to the South African operation, ECLs are determined using a simplified parameter-based approach. Refer to note 7.1.4 for more detail about ECLs and how these are calculated.

7.1.4 Credit risk

Credit risk, or the risk of financial loss to the Group due to customers or counterparties not meeting their contractual obligations, is managed through the application of credit approvals, limits and monitoring procedures. The Group’s maximum exposure to credit risk is represented by the carrying amount of the financial assets and contract assets that are exposed to credit risk.

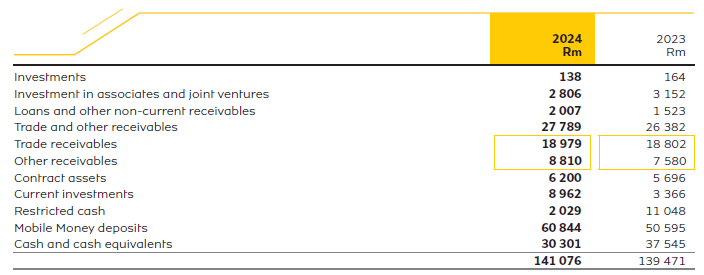

The Group considers its maximum exposure per class, without taking into account any collateral and financial guarantees, to be as follows:

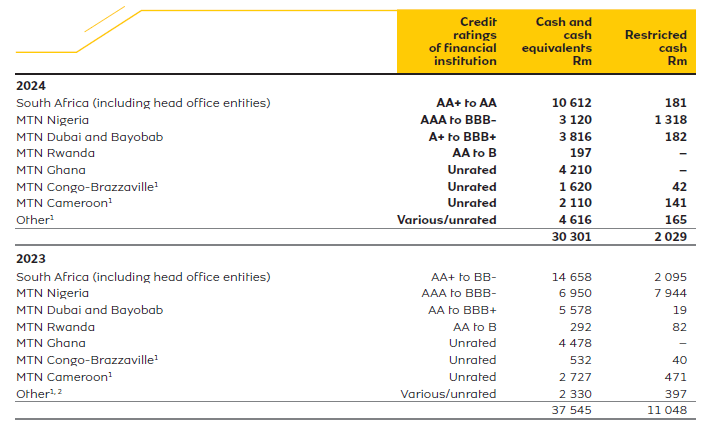

The local risk rating grade of cash and cash equivalents and restricted cash are set out below. Given these credit ratings, management does not expect any counterparty to fail to meet its obligations.

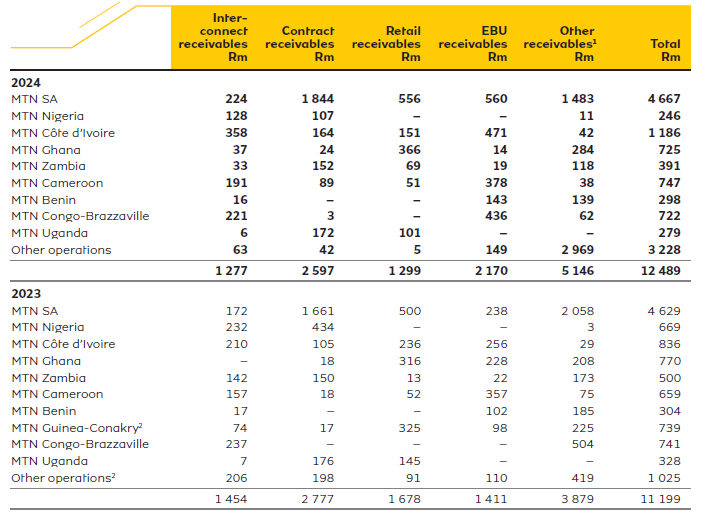

1 MTN Congo-Brazzaville and MTN Cameroon were previously included in other and have been disaggregated in the current year and comparative numbers have been re-presented accordingly.

2 Includes assets directly associated with non-current assets held for sale, refer to note 9.4.2.

The Group’s treasury bills and foreign currency deposits denominated in Nigerian naira and Rwandan franc respectively have local credit risk rating grade of B (2023: AAA to B).

Cash and cash equivalents, restricted cash and current investments

The Group determines appropriate internal credit limits for each counterparty. In determining these limits, the Group considers the counterparty’s credit rating established by an accredited ratings agency and performs internal risk assessments. The Group manages its exposure to a single counterparty by spreading transactions among approved financial institutions. The Group Treasury Committee regularly reviews and monitors the Group’s credit exposure.

Investment in insurance cell captives

The Group has exposure to the credit risk of the insurance company through its investment in preference shares in its cell captive arrangements.

MoMo deposits

MoMo deposits are balances that are held with banks for and on behalf of MoMo customers. Regulations in certain jurisdictions specify the types of permissible liquid instruments that these deposits may be invested in. MoMo deposits are spread among approved, reputable financial institutions based on internal risk assessments or guidance provided by regulators, to manage the concentration of credit risk to a single counterparty. Many risk mitigations are in place and banks are also obliged to pay insurance premiums to protect MoMo customer deposits (or a portion thereof) in the event of bank failure.

As a result of the uncertain and evolving legal and regulatory environment, the assessment of which party in a MoMo arrangement is exposed to a bank credit risk event, has become increasingly complex and dependent on legal interpretations that are largely untested in the respective markets in which the Group operates. Consequently, the assessment of the Group’s credit risk exposure with regards to MoMo remains subject to legal and regulatory developments.

The treatment of MoMo in the financial statements is not, and should not be construed as a waiver by members of the Group of any legal, contractual or statutory rights, remedies and defences they may have, or as an admission of liability enforceable against any of them in law or otherwise. The legal, contractual and statutory rights, remedies and defences of members of the Group are reserved.

Trade receivables and contract assets (unbilled handset component)

A large portion of the Group’s postpaid market revenues are generated in South Africa. There are no other significant concentrations of credit risk, since the other operations within the Group operate largely within the prepaid market. The Group has policies in place to ensure that retail sales of products and services are made to customers with an appropriate credit history. Before credit is granted to a customer, the Group performs credit risk assessments through credit bureaus. The Group insures some of its trade receivables in its South African operation, in which instance the credit risk assessments are performed by the credit insurer prior to the granting of credit by the Group. In terms of this arrangement R4.97 billion (2023: R6 billion) has been insured for which the Group’s risk is limited to R500 million (2023: R600 million). In addition, some entities within the Group require potential customers to obtain guarantees from banks before credit is granted. During the current year the Group did not recognise ECLs amounting to R22.5 million (2023: R36.9 million) as a result of collateral held.

The recoverability of interconnect receivables in certain international operations is uncertain; however, this is actively managed within acceptable limits and has been incorporated in the assessment of an appropriate revenue recognition policy (note 2.2) and the ECL of trade receivables where applicable. In addition, in certain countries there exists a right of set-off with interconnect parties to enable collection of outstanding amounts.

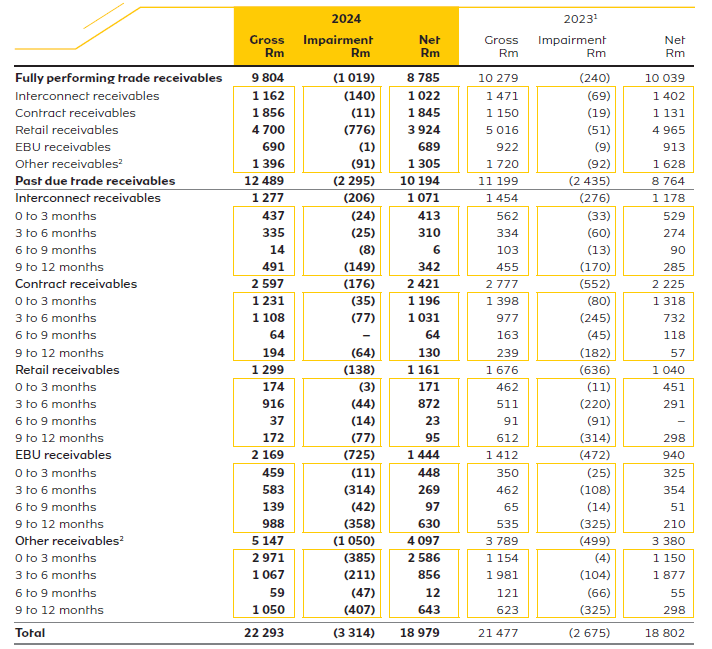

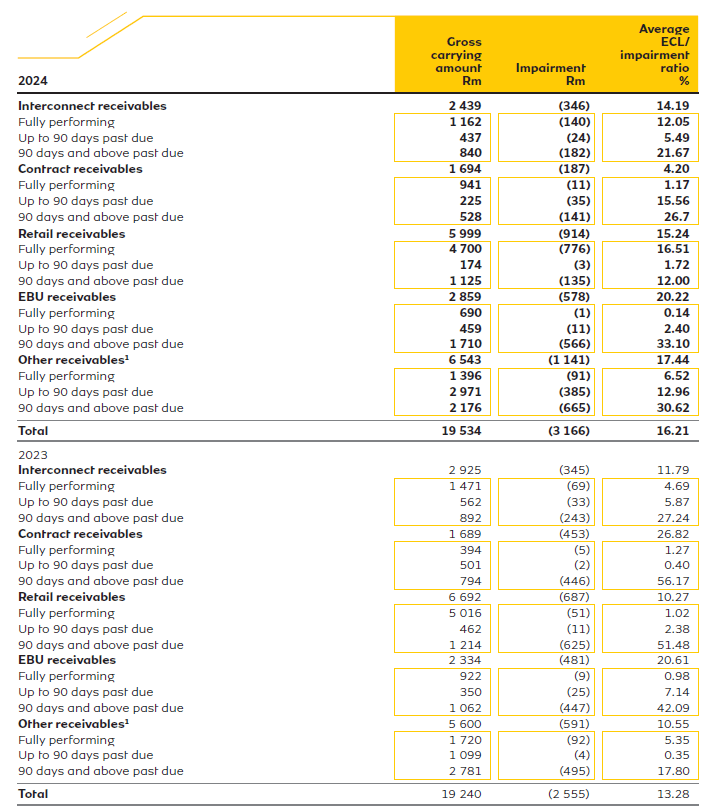

Ageing and impairment analysis

1 Includes assets directly associated with non-current assets held for sale, refer to note 9.4.2.

2 Other receivables includes both national and international roaming receivables.

Total past due per significant operation

1 Other receivables includes both national and international roaming receivables.

2 Includes assets directly associated with non-current assets held for sale, refer to note 9.4.2.

Expected credit losses

The Group has the following financial assets subject to the ECL model:

- Trade and other receivables.

- Contract assets.

- Loans and other non-current receivables.

- Debt investments carried at amortised cost.

- Treasury bills and foreign deposits carried at amortised cost.

- Cash and cash equivalents.

- Restricted cash.

- MoMo deposits.

Application of the ECL model had an immaterial impact on all financial assets except for contract assets and trade receivables.

Included in other receivables are amounts receivable from related parties (note 10.1) to which the Group has applied the general impairment model. The Group has considered the financial performance, external debt and future cash flows of the related parties and concluded that the credit risk relating to these receivables is limited and consequently the probability of default relating to these balances is low.

Provision matrix – ECLs are calculated by applying a loss ratio to the aged balance of trade receivables at each reporting date. The loss ratio is calculated according to the ageing/payment profile of sales by applying historical/proxy write-offs to the payment profile of the sales population. In instances where there was no evidence of historical write offs management used a proxy write-off. Trade receivable balances have been grouped so that the ECL calculation is performed on groups of receivables with similar risk characteristics and ability to pay. Similarly, the sales population selected to determine the ageing/payment profile of the sales is representative of the entire population and in line with future payment expectations. The historic loss ratio is then adjusted for forward-looking information (including forecast economic indicators) to determine the ECL for the portfolio of trade receivables at the reporting date to the extent that there is a strong correlation between the forward-looking information, and the ECL.

The Group used 12 – 36 months sales data to determine the payment profile of the sales. Where the Group has information about actual historical write-offs, actual write-offs have been used to determine a historic loss ratio. Alternatively, management has used a proxy write-off based on management’s best estimate. The Group has considered quantitative forward-looking information such as the core inflation rate. Qualitative assessments have also been performed, of which the impact was found to be immaterial.

The loss allowance for trade receivables to which the provision matrix has been applied is determined as follows:

1 Other receivables includes both national and international roaming receivables.

Simplified parameter-based approach – ECL is calculated using a formula incorporating the following parameters: Exposure at Default (EAD), Probability of Default (PD), Loss Given Default (LGD) discounted using the Effective Interest Rate (EIR) (i.e. PD x LGD x EAD = ECL). Exposures are mainly segmented by customer type i.e., corporate, consumer etc., ageing, device vs. SIM only contracts and months in contract. This customer segmentation occurs at MTN SA level and is not reported to Group key management personnel. This is done to allow for risk differentiation. The probability of a customer defaulting as well as the realised loss with defaulted accounts has been determined using historical data of 12 months. The EIR represents a weighted average rate which is representative of the portfolio of customers and incorporates a risk-free rate plus a risk premium on initial recognition of the trade receivables. A qualitative assessment of the impact of forward-looking information has been performed and found to be immaterial.

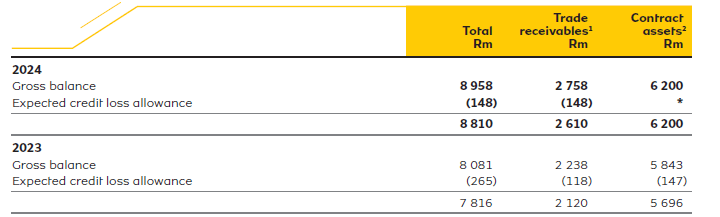

For corporate customers management rebutted the presumption that a customer is in default when 90 days past due and have determined default as 180 days past due. This is on the basis of billing disputes taking time to resolve resulting in a high-cure rate. Other than corporate customers, a customer is in default when 90 days past due. The balance of trade receivables and contract assets to which the simplified parameter-based approach has been applied is as follows:

1 Includes assets directly associated with non-current assets held for sale, refer to note 9.4.2.

2 Contract assets mainly relate to the South African operation.

* Amounts less that R1 million.

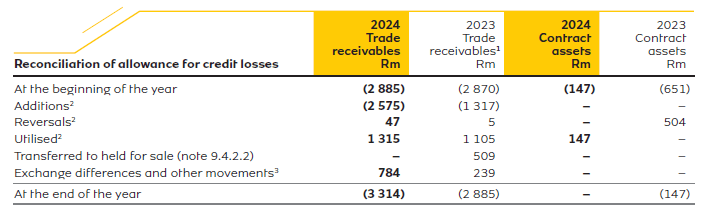

Trade receivables are written off when there is no reasonable expectation of recovery. An amount of R1 177 million (2023: R1 140 million) has been written off in the current year is subject to enforcement activity. This is assessed individually by each operation and includes for example where the trade receivables have been handed over for collection and remain outstanding or the debtor has entered bankruptcy.

1 Includes assets directly associated with non-current assets held for sale, refer to note 9.4.2.

2 A net impairment loss of R2 528 million (2023: R1 307 million) was recognised during the year.

3 Includes the effect of hyperinflation.

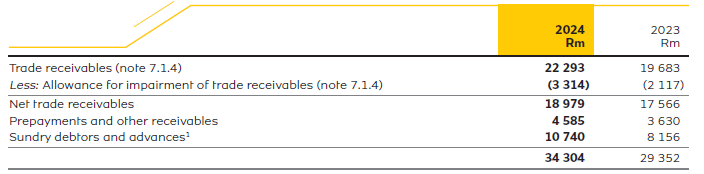

4.2 Trade and other receivables

Trade receivables are amounts due from customers for merchandise sold or services rendered in the ordinary course of business and are accounted for at amortised cost in accordance with the accounting policy disclosed in note 7.1.

Prepayments and other receivables are measured at their nominal values.

1 Sundry debtors and advances include advances to suppliers.

Impairment of trade receivables

An allowance for impairment of R2 528 million (2023: R1 312 million) was incurred in the current year. This amount is included in impairment and write-down of trade receivables and contract assets in profit or loss (note 2.3).

The Group’s exposure to credit and currency risk relating to trade and other receivables is disclosed in note 7.1.

Secured facilities and collateral

MTN Ghana has secured facilities through the pledge of its trade and other receivables amounting to R1 893 million (2023: R2 073 million) (note 6.1).

7.3 Loans and other non-current receivables

Loans and other non-current receivables are measured at amortised cost in accordance with the accounting policy disclosed in note 7.1.

Prepayments include costs paid relating to subsequent financial years and are stated at nominal value.

1 Includes prepayments relating to indefeasible right-of-use assets of R1 249 million (2023: R1 315 million) over capacity on international telecommunication cables.