Rio Tinto plc – Annual report – 31 December 2025

Industry: mining

13 Property, plant and equipment (extract 1)

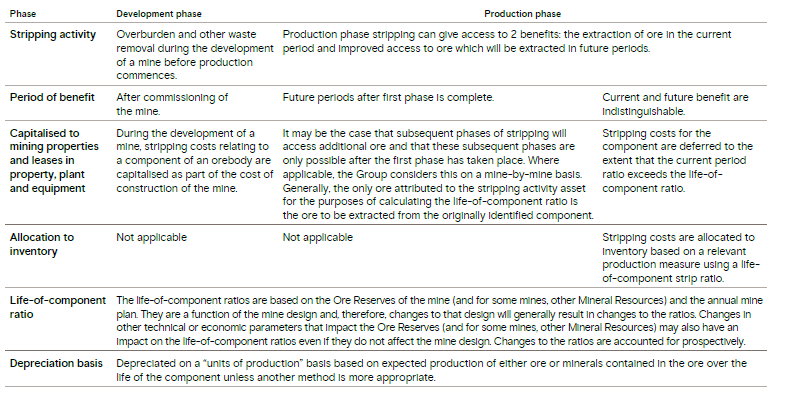

Deferred stripping

In open pit mining operations, overburden and other waste materials must be removed to access ore from which minerals can be extracted economically. The process of removing overburden and other waste materials is referred to as stripping. During the development of a mine (or, in some instances, pit; see below), before production commences, stripping costs related to a “component” of an orebody are capitalised as part of the cost of construction of the mine (or pit). A “component” is a specific section of the orebody that is made more accessible by the stripping activity. It will typically be a subset of the larger orebody that is distinguished by a separate useful economic life (for example, a pushback). These are then amortised over the life of the mine (or pit) on a units of production basis.

Where a mine operates several open pits that are regarded as separate operations for the purpose of mine planning, initial stripping costs are accounted for separately by reference to the ore from each separate pit. If, however, the pits are highly integrated for the purpose of mine planning, the second and subsequent pits are regarded as extensions of the first pit in accounting for stripping costs. In such cases, the initial stripping of the second and subsequent pits is considered to be production phase stripping (see below).

Key judgement Deferral of stripping costs

We apply judgement as to whether multiple pits at a mine are considered separate or integrated operations. This determines whether the stripping activities of a pit are classified as pre-production or production phase stripping and, therefore, the amortisation base for those costs. The analysis depends on each mine’s specific circumstances and requires judgement: another mining company could make a different judgement even when the fact pattern appears to be similar.

In order for production phase stripping costs to qualify for capitalisation as a stripping activity asset, 3 criteria must be met:

- it must be probable that there will be an economic benefit in a future accounting period because the stripping activity has improved access to the orebody

- it must be possible to identify the “component” of the orebody for which access has been improved

- it must be possible to reliably measure the costs that relate to the stripping activity.

Recognition and measurement of deferred stripping

13 Property, plant and equipment (extract 2)

(a) At 31 December 2025, the net book value of capitalised production phase stripping costs totalled US$2,506 million, with US$2,057 million within “Property, plant and equipment” and a further US$449 million within “Investments in equity accounted units” (2024: total of US$2,326 million, with US$1,947 million in “Property, plant and equipment” and a further US$379 million within “Investments in equity accounted units”). During the year, capitalisation of US$622 million was offset by depreciation of US$460 million, inclusive of amounts recorded within equity accounted units (2024: US$423 million offset by depreciation of US$580 million). Depreciation of deferred stripping costs in respect of subsidiaries of US$303 million (2024: US$411 million; 2023: US$216 million) is included within “Depreciation for the year”.