Barratt Redrow plc – Annual report – 29 June 2025

Industry: real estate

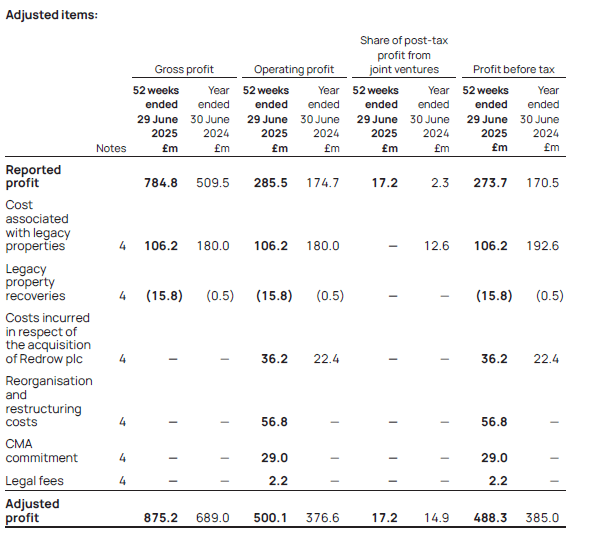

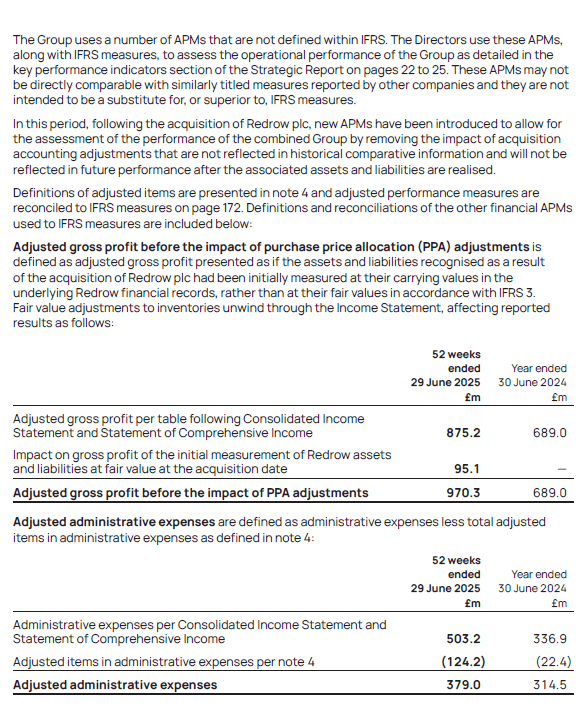

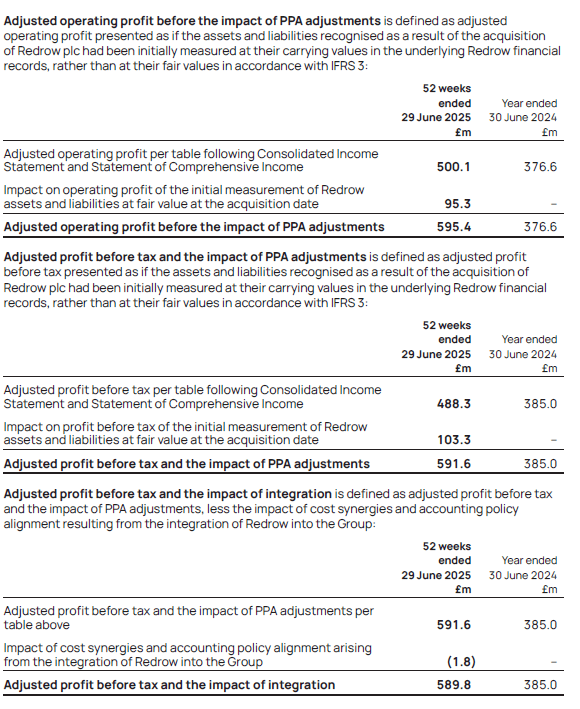

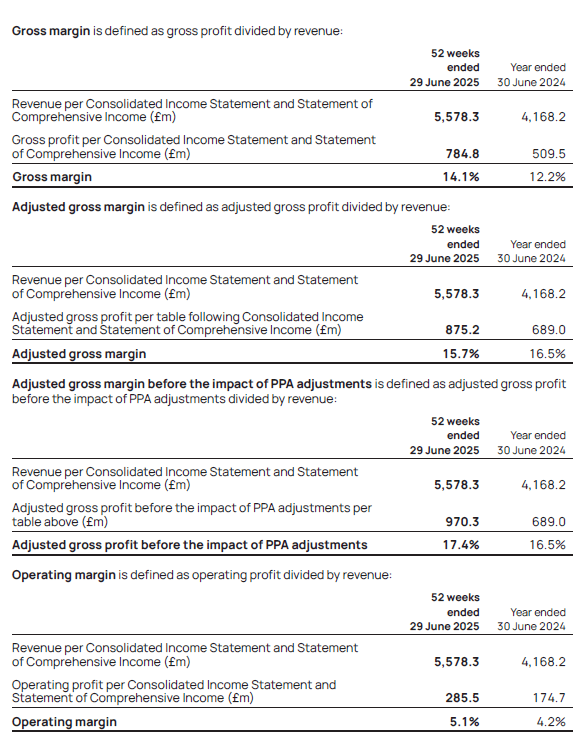

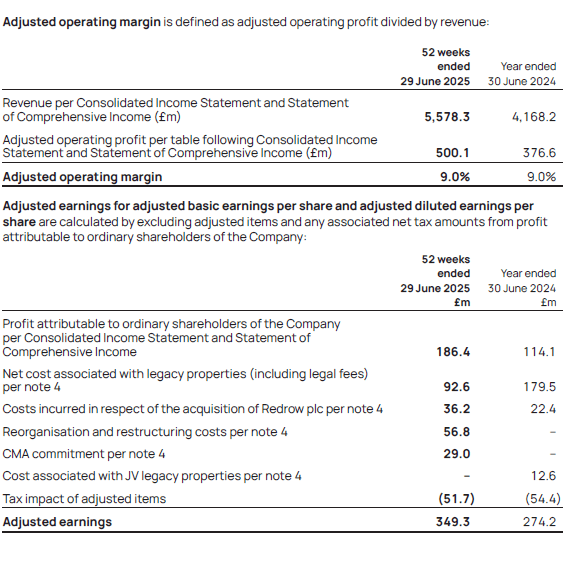

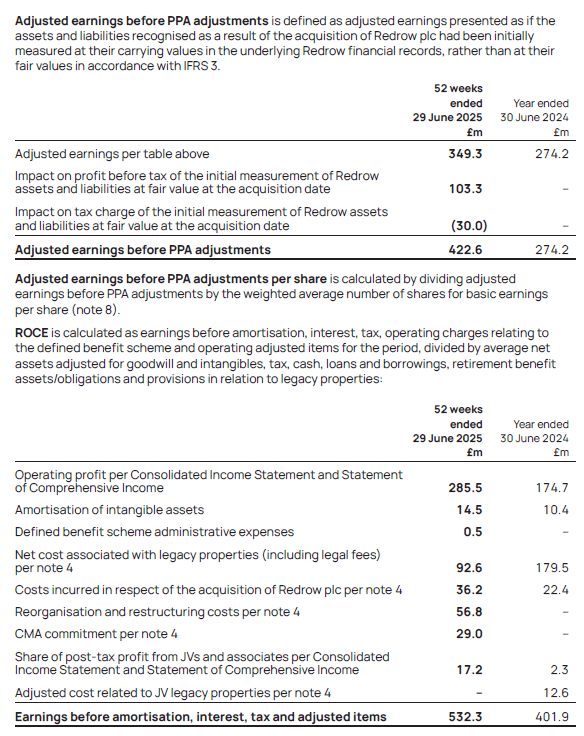

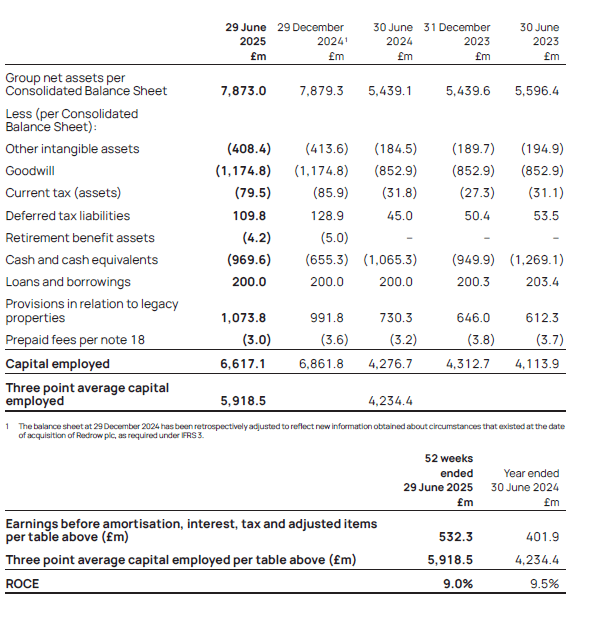

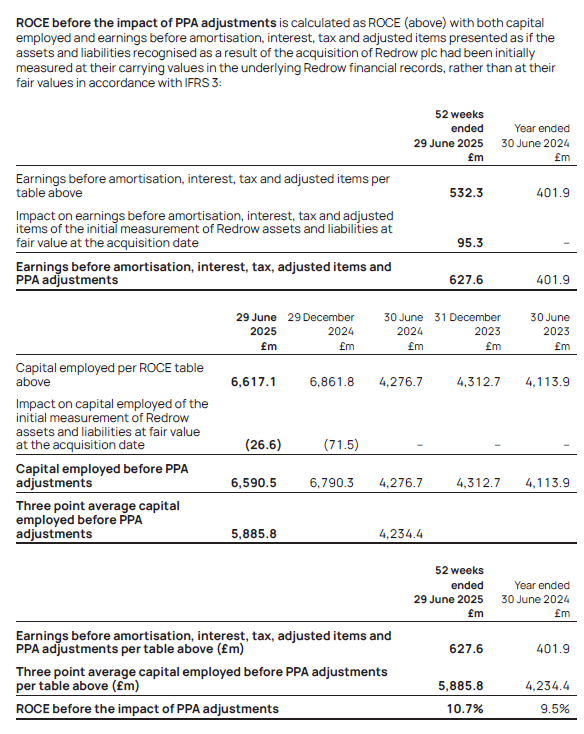

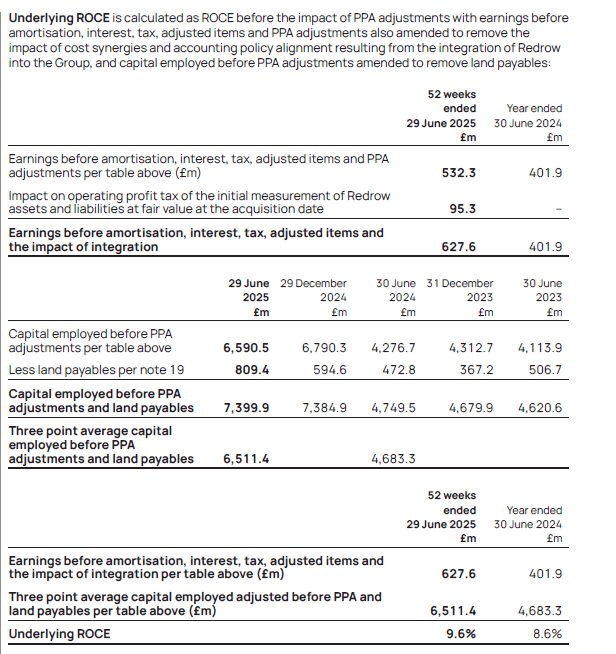

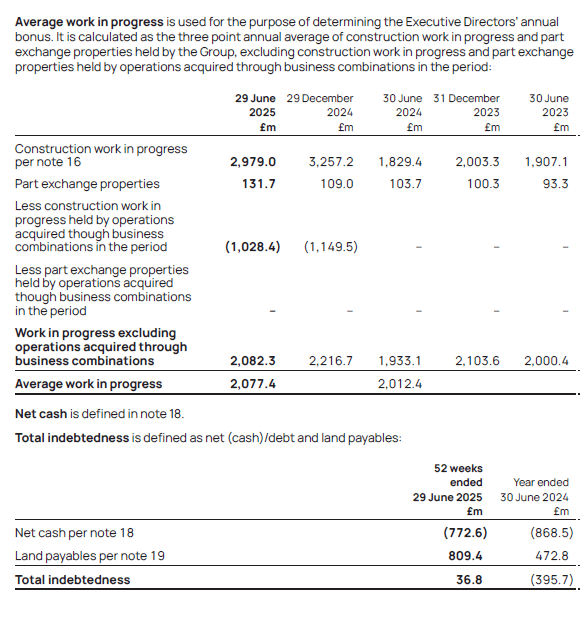

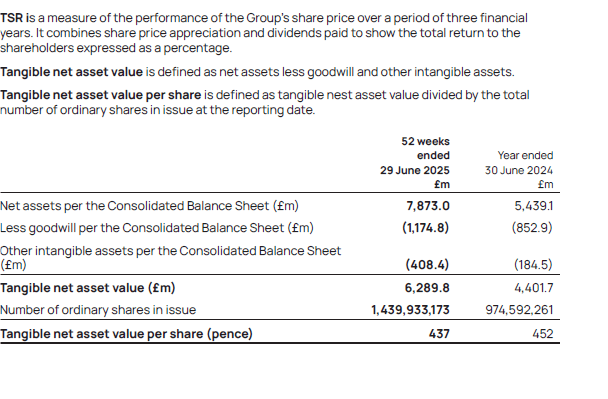

Definitions of alternative performance measures (APMs) and reconciliation to IFRS (unaudited)

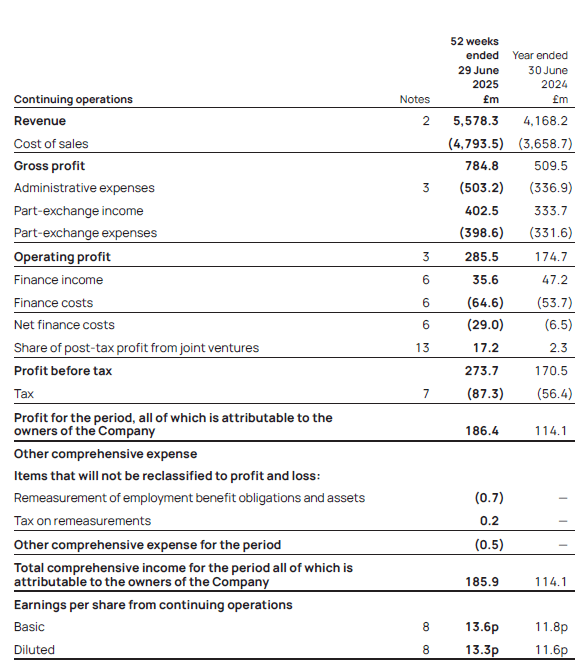

Consolidated Income Statement and Statement of Comprehensive Income

52 weeks ended 29 June 2025