Novartis AG – Financial report – 31 December 2023

Industry – pharmaceuticals

1. Accounting policies (extract)

Distribution of Sandoz Group AG to

Novartis AG shareholders

At the Extraordinary General Meeting (EGM) of Novartis AG shareholders, held on September 15, 2023, the Novartis AG shareholders approved a special distribution by way of a dividend in kind to effect the spin-off of Sandoz Group AG.

The September 15, 2023, shareholder approval for the spin-off required the Sandoz Division and selected portions of corporate activities attributable to Sandoz’s business, as well as certain expenses related to the spinoff (the “Sandoz business”) to be reported as discontinued operations.

The shareholder approval on September 15, 2023, for the spin-off the Sandoz business, required the recognition of a distribution liability at the fair value of the Sandoz business. Novartis policy is to measure the distribution liability at the fair value of the Sandoz business net assets taken as a whole. The distribution liability was recognized through a reduction in retained earnings. It was required to be adjusted at each balance sheet date for changes in its estimated fair value, up to the date of the distribution to shareholders through retained earnings. Any resulting impairment of the business assets to be distributed would have been recognized in the consolidated income statements in “Other expense” of discontinued operations, at the date of initial recognition of the distribution liability or at subsequent dates resulting from changes of the distribution liability valuation.

At the October 4, 2023, distribution settlement date, the resulting gain, which is measured as the excess amount of the distribution liability over the then-carrying value of the net assets of the business distributed, was recognized on the line “Gain on distribution of Sandoz Group AG to Novartis AG shareholders” within the income statement of discontinued operations.

The recognition of the distribution liability required the use of valuation techniques for the purposes of impairment testing of the Sandoz business’ assets to be distributed and for the measurement of the fair value of the distribution liability. These valuations required the use of management assumptions and estimates related to the Sandoz business’ future cash flows, market multiples, opening share price of Sandoz Group AG on the first day of trading its shares on the SIX Swiss Exchange, to estimate day one market value, and control premiums to apply in estimating the Sandoz business fair value. These fair value measurements are classified as “Level 3” in the fair value hierarchy. The section “—Goodwill and intangible assets other than goodwill” in this Note 1 provides additional information on key assumptions that are highly sensitive in the estimation of fair values using valuation techniques.

Transaction costs that are directly attributable to the Distribution (spin-off) of the Sandoz business to Novartis AG shareholders by way of a dividend in kind, and that would otherwise have been avoided, were accounted for as a deduction from equity (within retained earnings). Prior to the recognition of the distribution liability, these costs were recorded as prepaid expenses in the consolidated balance sheet.

For additional disclosures, refer to “Note 2. Significant transactions—Significant transactions in 2023—Completion of the spin-off of the Sandoz business through a dividend in kind distribution to Novartis AG shareholders,” and “Note 31. Discontinued operations.”

2. Significant transactions (extract)

Significant transactions in 2023

Completion of the spin-off of the Sandoz business through a dividend in kind distribution to Novartis AG shareholders

On July 18, 2023, Novartis announced that its Board of Directors had unanimously endorsed the proposed separation of the Sandoz business to create an independent company by way of a spin-off and to seek shareholder approval for the spin-off of the Sandoz business into a separately traded standalone company, following the complete structural separation of the Sandoz business into a standalone company (the Sandoz business or Sandoz Group AG) and subject to the satisfaction of certain conditions and Novartis AG shareholders’ approval.

At the EGM held on September 15, 2023, Novartis AG shareholders approved a special distribution by way of a dividend in kind to effect the spin-off of Sandoz Group AG, subject to the completion of certain conditions precedent to the distribution. Upon shareholder approval, the Sandoz business was reported as discontinued operations and the distribution liability was recognized at its fair value, which exceeded the carrying value of the Sandoz business net assets.

The conditions precedent to the spin-off were met and on October 3, 2023 the spin-off of the Sandoz business was effected by way of a distribution of a dividend in kind of Sandoz Group AG shares to Novartis AG shareholders and American Depositary Receipt (ADR) holders (the Distribution). Through the Distribution, each Novartis AG shareholder received 1 Sandoz Group AG share for every 5 Novartis AG shares and each Novartis ADR holder received 1 Sandoz ADR for every 5 Novartis ADR that they held at the close of business on October 3, 2023. As of October 4, 2023, the shares of Sandoz Group AG have been listed on the SIX Swiss Exchange (SIX) under the stock symbol “SDZ”.

On September 18, 2023, the Sandoz business entered into financing arrangements with a group of banks under which on September 28, 2023, it borrowed a total amount of USD 3.3 billion. These borrowings consisted of a bridge loan in EUR (EUR 2.4 billion) and term loans in EUR (EUR 0.2 billion) and USD (USD 0.5 billion). In addition, the Sandoz business borrowed approximately USD 0.4 billion under a number of local bilateral facilities in different countries. This resulted in a total gross debt of USD 3.7 billion. These outstanding borrowings of the Sandoz business legal entities were recognized in the September 30, 2023 consolidated balance sheet within Liabilities related to discontinued operations and within financing activities cash flows from discontinued operations.

Prior to the Distribution on October 3, 2023, Sandoz business legal entities paid approximately USD 3.3 billion in cash to Novartis and its affiliates through a series of intercompany transactions.

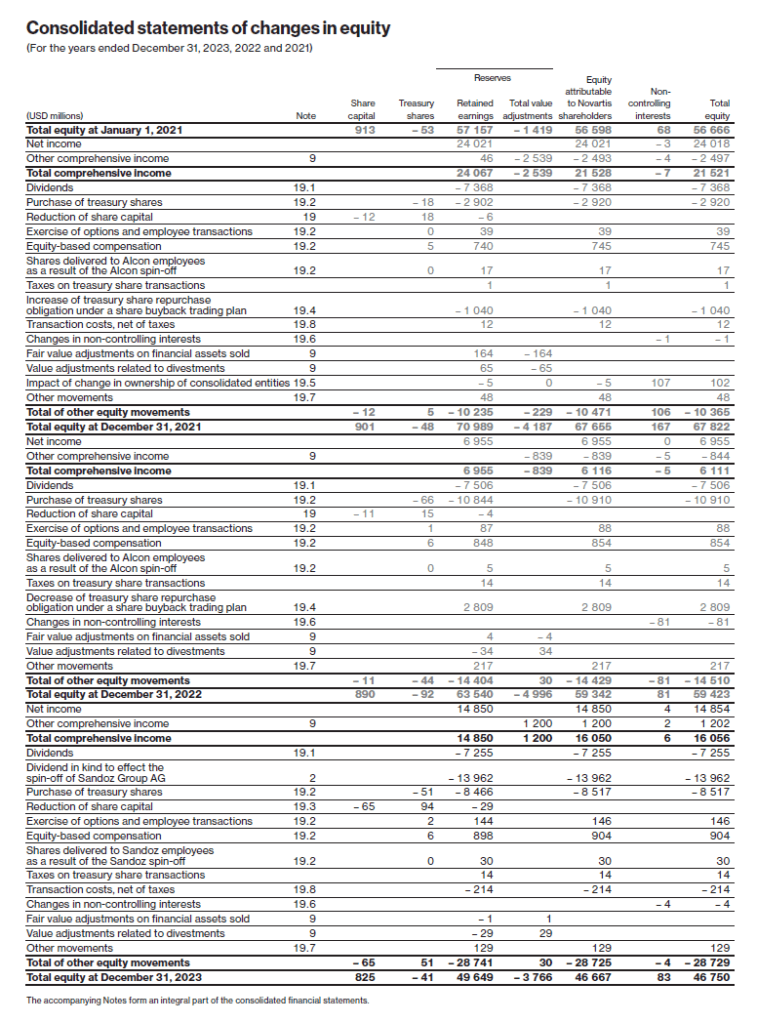

At the Distribution date on October 3, 2023, the dividend in kind distribution liability to effect the Distribution (spin-off) of the Sandoz business amounted to USD 14.0 billion, measured by reference to the October 4, 2023 opening Sandoz Group AG share price and applying a control premium. The dividend in kind distribution liability was recorded as a reduction to equity (retained earnings) and remained in excess of the then carrying value of the Sandoz business net assets, which amounted to USD 8.6 billion (see Note 31).

Certain consolidated foundations own Novartis AG dividend-bearing shares that restricts their availability for use by Novartis. These Novartis AG shares are accounted for as treasury shares. Through the Distribution, these foundations received Sandoz Group AG shares representing an approximate 4.31% equity interest in Sandoz Group AG. Upon the loss of control of Sandoz Group AG through the Distribution on October 3, 2023, the financial investment in Sandoz Group AG was recognized at its initial fair value based on the opening traded share price of Sandoz Group AG on October 4, 2023 (a Level 1 hierarchy valuation). At initial recognition, on October 4, 2023, the Sandoz Group AG financial investment had a fair value of USD 0.5 billion, and was reported in the fourth quarter of 2023 on the consolidated balance sheet as a financial asset. Management has designated this investment at fair value through other comprehensive income.

The total non-taxable, non-cash gain recognized at the Distribution date of the spin-off of the Sandoz business amounted to USD 5.9 billion, which consists of:

1 See Note 31 for additional information.

For additional disclosures on discontinued operations, refer to Note 31.

31. Discontinued operations

Discontinued operations include the operational results from the Sandoz generic pharmaceuticals and biosimilars division and certain corporate activities attributable to the Sandoz business, as well as certain other expenses related to the spin-off. Included in 2023 is also the IFRS Accounting Standards non-cash, non-taxable net gain on the distribution of Sandoz Group AG to Novartis AG shareholders (refer to Notes 1 and 2 for further details).

The Sandoz business operates in the off-patent medicines segment and specializes in the development, manufacturing, and marketing of generic pharmaceuticals and biosimilars. The Sandoz business is organized globally into two franchises: Generics and Biosimilars.

Net income from discontinued operations

1 The net income from discontinued operations for 2023 is for the period from January 1, 2023, to the October 3, 2023, Distribution date.

2 The tax rate in 2023 was impacted by non-recurring items such as tax benefits arising from intercompany transactions to effect the spin-off of the Sandoz business, net decreases in uncertain tax positions of the Sandoz business and the favorable settlement of a tax matter related to the Alcon business, which was spun-off in 2019. Excluding these impacts, the tax rate would have been 31.2% in 2023, compared to 24.1% and 30.7% in 2022 and 2021, respectively. The tax rate in 2023 is higher than 2022 primarily due to a change in profit mix between years.

3 See Note 2 for further details on the non-taxable, non-cash gain on distribution of Sandoz Group AG to Novartis AG shareholders.

Net assets derecognized

The following table presents the Sandoz business net assets derecognized as at October 3, 2023 Distribution (spin-off) date:

Supplemental disclosures related to discontinued operations

Revenue

In addition to the elements of variable consideration listed in the revenue accounting policy described in Note 1, the Sandoz business grants shelf stock adjustments to customers to cover the inventory held by them at the time a price decline becomes effective. Revenue deduction provisions for shelf stock adjustments are recorded when the price decline is anticipated, based on the impact of the price decline on the customer’s estimated inventory levels.

Significant transactions in 2021

On February 10, 2021, Sandoz entered into an agreement with certain subsidiaries of GlaxoSmithKline plc (GSK) for the acquisition of the GSK’s cephalosporin antibiotics business.

Under the agreement, Sandoz acquired the global rights to three established brands (Zinnat®, Zinacef® and Fortum®) in more than 100 markets. It excluded the rights in the US, Australia and Germany to certain of those brands, which were previously divested by GSK, and the rights in India, Pakistan, Egypt, Japan (to certain of the brands) and China, which will be retained by GSK. The transaction closed on October 8, 2021.

The purchase price consisted of a USD 350 million upfront payment paid at closing and potential milestone payments up to USD 150 million, which GSK is eligible to receive upon the achievement of certain annual sales milestones for the portfolio.

The fair value of the total purchase consideration was USD 415 million. The amount consisted of a payment of USD 351 million, including purchase price adjustments, and the fair value of contingent consideration of USD 64 million, which GSK is eligible to receive upon the achievement of specified milestones. The purchase price allocation resulted in net identifiable assets of USD 308 million, consisting of USD 292 million intangible assets and USD 16 million deferred tax assets. Goodwill amounted to USD 107 million.

The 2021 results of operations since the date of acquisition were not material.

Net income from discontinued operations

Included in net income from discontinued operations are:

1 2023 amounts are for the period from January 1, 2023, to the October 3, 2023, Distribution date.

In 2023, 2022 and 2021, there were no reversals of impairment charges on right-of-use assets or on intangible assets of discontinued operations.

Balance sheet

The following table shows for discontinued operations the additions to property, plant and equipment, right-of-use assets and to goodwill and intangible assets:

1 The additions for 2023 are for the period from January 1, 2023, to the October 3, 2023, Distribution date.

Financial debt

The Sandoz business entered into financing agreements with a group of banks under which it borrowed on September 28, 2023 a total amount of USD 3.3 billion. See Note 2 for further disclosures.

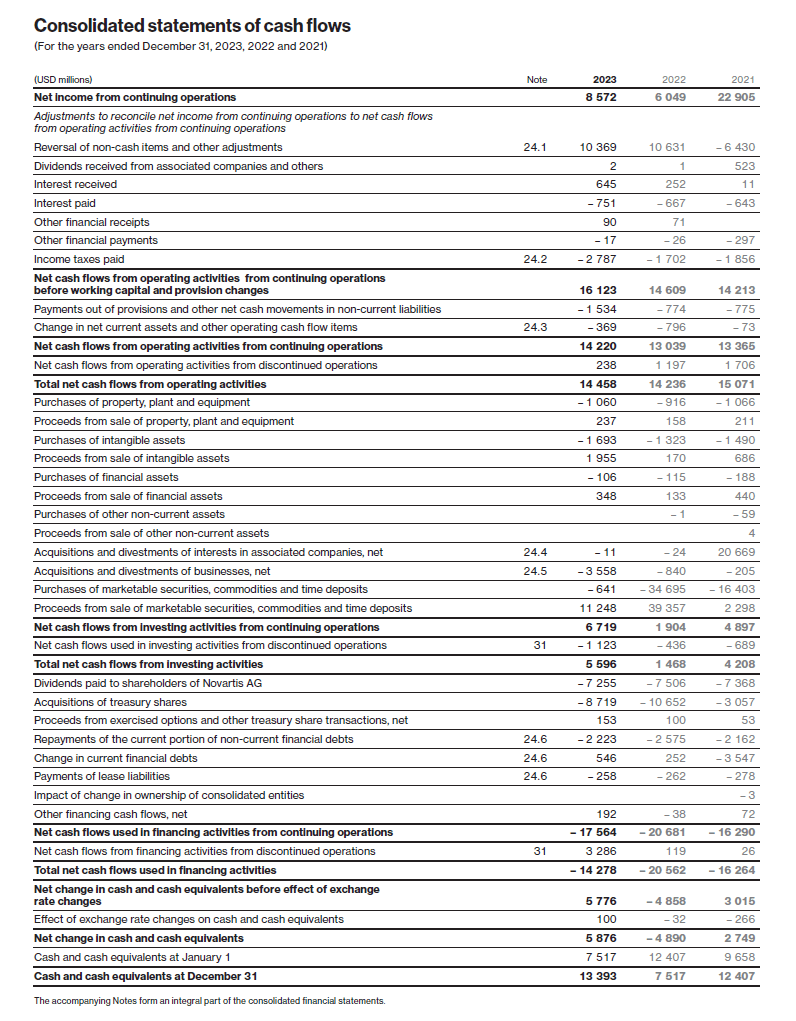

Net cash flows used in investing activities from discontinued operations

Net cash flows used in investing activities from discontinued operations include the investing activities of the Sandoz business. In 2023, other cash flows used in investing activities, net includes cash outflows of USD 22 million (2022: USD 39 million, 2021: USD 362 million, including the acquisition of GSK’s cephalosporin antibiotics business) for the acquisitions and divestments of business, net.

Net cash flows from financing activities from discontinued operations

In 2023, the net cash inflows from financing activities from discontinued operations of USD 3.3 billion (2022: USD 119 million, 2021: USD 26 million) were mainly driven by USD 3.6 billion cash inflows from bank borrowings (including the USD 3.3 billion Sandoz business borrowings from a group of banks on September 28, 2023) in connection with the Distribution (spin-off) of the Sandoz business to Novartis AG shareholders, partly offset by transaction cost payments of USD 0.2 billion (2022: nil, 2021: nil) directly attributable to the Distribution (spinoff) of the Sandoz business (see Notes 1 and 2). For additional information related to the October 3, 2023 Distribution (spin-off) of the Sandoz business to Novartis AG shareholders, effected through a dividend in kind distribution of Sandoz Group AG shares to Novartis AG shareholders and ADR holders, refer to Note 1 and Note 2.