International Consolidated Airlines Group, S.A. – Annual report – 31 December 2025

Industry: airline

4 Impact of climate change on financial reporting

Significant transactions and critical accounting estimates, assumptions and judgements in the determination of the impact of climate change

As a result of climate change, the Group has designed and approved its Flightpath Net Zero climate strategy, which commits the Group to net zero emissions by 2050. While approved business plans currently have a duration of three years, the Flightpath Net Zero climate strategy impacts the short-, medium- and long-term operations of the Group.

The details regarding the inputs and assumptions used in the determination of the Flightpath Net Zero climate strategy include, but are not limited to, the following that are within the control of the Group:

- The additional cost of the Group’s commitment to increasing the use of Sustainable Aviation Fuel (SAF) to 10% by 2030 and to 70% by 2050;

- The cost of incurring an increase in the level of carbon offsetting and carbon capture schemes; and

- The impact of introducing more fuel-efficient aircraft and being able to operate these more efficiently.

In addition to these inputs and measures within the control of management, Flightpath Net Zero includes assumptions pertaining to consumers, governments and regulators regarding the following:

- The impact on passenger demand for air travel as a result of both passenger trends regarding climate change and government policies;

- Investment and policy regarding the development of SAF production facilities;

- Investment and improvements in air traffic management; and

- The price of carbon through the EU, Swiss and UK Emissions Trading Systems/Schemes (ETS) and the UN Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA).

The level of uncertainty regarding the impact of these factors increases over time. Accordingly, the Group has applied critical estimation and judgement in the evaluation of the impact of climate change on the recognition and measurement of assets and liabilities within the financial statements.

Critical accounting estimates, assumptions and judgements – cash flow forecast estimation

With the Flightpath Net Zero climate strategy assessing the impact over a long-term horizon to 2050, the level of estimation uncertainty in the determination of cash flow forecasts increases over time. For those assets and liabilities, where their recoverability is dependent on long-term cash flows, the following critical accounting estimates, assumptions and judgements, to the extent they can be reliably measured, have been applied:

a Long-term fleet plans and useful economic lives

The Group’s Flightpath Net Zero climate strategy has been developed in conjunction with the long-term fleet plans of each operating company. This includes the annual assessment of useful lives and the residual values of each aircraft type.

With the current aircraft fleet and the future committed delivery of 217 fuel-efficient aircraft as detailed in note 15, the Group considers the existing and future fleet assets align with the long-term fleet plans to achieve its Flightpath Net Zero climate strategy. All aircraft in the fleet, and those due to be delivered in the future, have the capability to utilise SAF in their operations without impediment. Accordingly, no impairment has arisen in the current or prior year, nor have the useful lives and residual values of aircraft been amended, as a result of the Group’s decarbonisation plans.

b Impairment testing of the Group’s cash-generating units

The Group applies discounted cash flow models for each cash-generating unit (CGU), derived from the cash flow forecasts from the approved three-year business plans. The Group’s Flightpath Net Zero climate strategy is long-term in nature and includes commitments that will occur at differing points over this time horizon. To the extent that certain of those commitments occur over the short term, they have been incorporated into the three-year business plans.

The Group adjusts the final year (being the third year) of these probability-weighted cash flows to incorporate the impacts of climate change from the Group’s Flightpath Net Zero climate strategy that are expected to occur over the medium term, being to 2035 (2024: through to 2030). These adjustments are limited to those that: (i) the Group can reliably estimate at the balance sheet date, with those costs subsequent to 2035 having such a high degree of uncertainty that they cannot be reliably estimated; (ii) only relate to the Group’s existing asset base in its current condition; and (iii) incorporate legislation and regulation that is expected to be required to achieve the Group’s Flightpath Net Zero climate strategy, and which is sufficiently progressed at the balance sheet date.

As a result, the Group’s impairment modelling incorporates the following aspects of the Group’s Flightpath Net Zero climate strategy through to 2035, after which time the level of uncertainty regarding timing and costing becomes insufficiently reliable to estimate: (i) an increase in the level of SAF consumption in the overall fuel mix; (ii) forecast cost of carbon, including SAF, ETS allowances and CORSIA units (all derived from externally sourced or derived information); (iii) the removal of existing free ETS allowances issued by EU member states, Switzerland and the UK; and (iv) assumptions regarding the ability of the Group to recover these incremental costs through increased ticket pricing.

In preparing the impairment models, the Group cash flow projections are prepared on the basis of using the current fleet in its current condition. The Group excludes the estimated cash flows expected to arise from future restructuring unless already committed and assets not currently in use by the Group. In addition, for the avoidance of doubt, the Group’s impairment modelling excludes the following aspects of the Group’s Flightpath Net Zero climate strategy: (i) the expected transition to electric and hydrogen aircraft, as well as future technological developments to jet engines and airframes; (ii) any savings from the transition to more fuel-efficient aircraft other than those either in the Group’s fleet or committed orders due to be delivered over the business plan period as replacement aircraft; (iii) the benefit of the development of carbon capture technologies and enhanced carbon offsetting mechanisms; (iv) the required beneficial reforms to air traffic management regulation and legislation; (v) the consumption of advanced SAF products that have not yet been proven to be technologically feasible; and (vi) the required government incentives and/or support across the supply chain.

As detailed in note 17, the Group applies a long-term growth rate to these adjusted probability weighted cash flows, per CGU, and each of the long-term growth rates includes a specific adjustment to reduce the rate to reflect the Group’s assumptions regarding the reduced demand and elasticity impact arising from climate change. These impacts are derived with reference to external market data, industry publications and internal analysis.

Given the inherent uncertainty associated with the impact of climate change, the Group has applied additional sensitivities in note 17 to reflect a more adverse impact of climate change than currently expected. This has been captured through both the downward sensitivities of the long-term growth rates, ASKs and operating margins, and the increased fuel price sensitivity.

c Valuation of employee benefit scheme assets

The Group’s employee benefit schemes are principally represented by the British Airways APS and NAPS schemes in the UK. The schemes are structured to make post-employment payments to members over the long term, with the trustees having established both return-seeking assets and liability-matching assets that mature over the long term to align with the forecast benefit payments.

The assets of these schemes are invested predominantly in a diversified range of equities, bonds and property. The valuation of these assets ranges from those with quoted prices in active markets, where prices are readily and regularly available, through to those where the valuations are not based on observable market data, and which therefore often require complex valuation models. The trustees of the schemes have integrated climate change considerations into their long-term decision-making and reporting processes across all classes of assets, actively engaging with all fund and portfolio managers to ensure that where unobservable inputs are required for valuation models, such valuation models incorporate long-term expectations regarding the impact of climate change.

d Recoverability of deferred tax assets

In determining the recoverable amounts of the Group’s deferred tax assets, the Group applies future cash flow projections for a period of up to 10 years derived from the approved three-year business plans. The Group applies a medium-term growth rate subsequent to the three-year business plans, specific to each operating company. In considering the impact of the Group’s Flightpath Net Zero climate strategy, management adjusts this medium-term growth rate, where applicable, to incorporate the assumed impacts on both revenue and costs to the Group.

e Provision recognition

Under Flightpath Net Zero, the Group has committed to reducing its net emissions to zero by 2050, and accordingly the Group has considered whether such a commitment gives rise to a provision at the balance sheet date. In order to recognise a provision, an entity must meet the following criteria: (i) the entity has a present obligation as result of a past event; (ii) it is probable that an economic outflow of resources will be required to settle the obligation; and (iii) a reliable estimate can be made of the amount of the obligation.

While the Group considers there will be an economic outflow of resources to meet its Flightpath Net Zero commitment, these commitments relate to the emissions arising in future reporting periods irrespective of when those commitments were announced. Accordingly, the Group does not consider that the Flightpath Net Zero commitments give rise to a present obligation as a result of a past event and no separate provisions have been recorded in relation to these commitments.

f The price of carbon

EU, Swiss and UK Emissions Trading Systems/Schemes

The EU, Swiss and the UK ETS were established to reduce greenhouse gas emissions cost effectively. Under these schemes the Group’s operating companies are required to buy emission allowances or are issued them under existing quotas. The Group is required to surrender these allowances to the relevant authorities annually dependent on the level of CO2 equivalent emitted within a 12-month period. Over time, the level of available emission allowances decreases in order to reduce total emissions, which has the effect of increasing the price of such allowances. The Group expects that the future price of such allowances will continue to increase and that the free allocation of emission allowances will cease. Given the relatively illiquid nature of the emission allowance market, there is uncertainty as to the future pricing of such allowances.

Carbon Offsetting and Reduction Scheme for International Aviation

In October 2016 the International Civil Aviation Organization adopted CORSIA, which aims to offset growth-related CO2 emissions in international air traffic from 1 January 2021, with the pilot phase running through to 31 December 2023. The first phase of the CORSIA implementation commenced on 1 January 2024 and will run through to 31 December 2026, after which the second phase will run through to 31 December 2035, measured in three-year reporting periods. The first phase of CORSIA is voluntary, and currently 126 States have agreed to participate.

The first phase of CORSIA utilises total CO2 emissions from international civil aviation over a baseline of 85% of the 2019 level of emissions (the Baseline Year) for all participating States. The offsetting requirements apply to CORSIA eligible flights, being all international flights between participating States, with the following flights excluded: (i) domestic flights; (ii) international flights between States where at least one State has not volunteered to participate in the first phase; and (iii) those flights subject to various ETS arrangements, to avoid duplication of emission charges. In addition, for those flights utilising SAF, the CORSIA offsetting requirement is reduced, but not eliminated, depending on the lifecycle carbon reductions of the SAF compared to conventional fossil jet kerosene.

The calculation and verification of the offsetting requirements in the first phase shall be determined by the sectoral approach annually, with companies retiring their obligations in 2028 (although retirements can occur earlier subject to agreement with national authorities). Under the sectoral approach, each of the Group’s operating companies will be required to offset an amount of CO2 emissions equivalent to the emissions generated on CORSIA eligible flights, multiplied by the Sector’s Growth Factor. The Sector’s Growth Factor is calculated based on total global aviation CO2 emissions arising on international air routes between all participating States in a given year divided by the total sectoral CO2 emissions in the Baseline Year for the same routes.

Voluntary offset schemes

The Group utilises certain voluntary offset schemes to offset certain CO2 emissions. The Group purchases offset certificates arising from a broad range of accredited projects. Periodically, the Group will retire these offset certificates from the registry.

Impact on financial reporting

As detailed in note 2, the Group accounts for the purchase of allowances as an increase in Carbon-related and other assets, which are measured at amortised cost. In addition, as the Group emits CO2 equivalent as part of its flight operations, a provision is recorded to settle the Carbon-related obligation. As the provision is recognised, a corresponding amount is recorded in the Income statement within Fuel costs and emission charges. For emissions for which the Group has already purchased Carbon-related assets, the provision is valued at the weighted cost of those allowances. Where the level of emissions exceeds the amounts of allowances held, this deficit is measured at the market price of such allowances at the balance sheet date.

For the year to, and at 31 December 2025, the Group has recorded the following within the financial statements:

Carbon-related assets (presented as part of Carbon-related and other assets in note 20) include the following amounts:

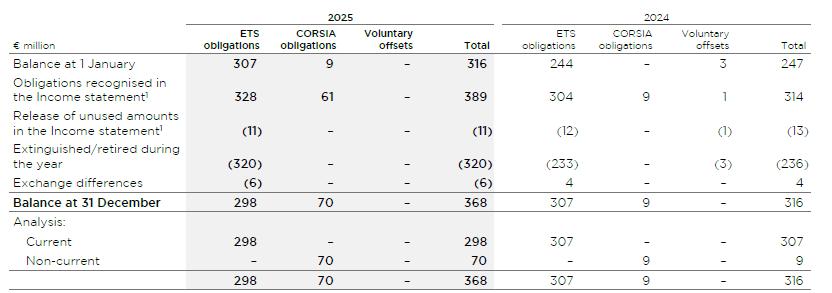

Carbon-related obligations (presented as part of Provisions in note 27) include the following amounts:

1 For the year to 31 December 2025, the total amount in the Income statement within Fuel costs and emission charges that related to emission allowances was €378 million (2024: €301 million). Refer to note 6.

See note 35 for details of the amounts recognised in the Cash flow statement for the years to 31 December 2025 and 31 December 2024.

At 31 December 2025 and 31 December 2024, the Group had acquired and committed to acquire, at fixed prices, the following percentages of its total emissions allowances forecast to be purchased over the three-year business plan periods: