Telenor ASA – Annual report – 31 December 2022

Industry: telecoms

NOTE 13

Cash flow information (extract)

Cash payments related to lease contracts

Repayments of the principal portion related to total lease liabilities in 2022 of NOK 8.1 billion (NOK 8.8 billion in 2021) include instalment payment of spectrum licences of NOK 2.5 billion (NOK 2.9 billion in 2021) and repayments of other leases of NOK 5.6 billion (NOK 6.0 billion in 2021). The instalment payments of spectrum licences in 2022 and 2021 were mainly in dtac, Norway and Pakistan. Lease payments related to other lease contracts were mainly in dtac, Sweden, Digi, Pakistan and Grameenphone in 2022 whereas in 2021 it was mainly in dtac, Sweden, Digi, Myanmar, Pakistan.

Repayments of the interest portion of total lease liabilities in 2022 of NOK 1.1 billion include repayments of interest related to spectrum licences of NOK 0.4 billion (NOK 0.3 billion in 2021) and repayments of interest related to other lease contracts of NOK 0.7 billion (NOK 0.7 billion in 2021).

Payments of variable, short term and low value leases of NOK 3.1 billion include variable lease payments of NOK 3.0 billion and payments of short term and low value leases of NOK 0.2 billion.

Prepayments of investing activities of NOK 0.8 billion in 2022 mainly related to payments made at or before acquisition of spectrum licences of NOK 0.3 billion in Norway for the bands of 2500-2690 MHz and 3400-3800 MHz and NOK 0.3 billion in Grameenphone for the bands 2.6 GHz.

NOTE 16

Right-of-use assets

Telenor has chosen to account for the right to use the spectrum as a lease, where the identified asset is the frequency band that is exclusive for Telenor in the lease period. Telenor also leases passive infrastructure such as towers and cables in addition to land and property. Refer to 29 for more information about lease liabilities.

Accounting policies

A lease liability and a right-of-use asset is recognised at commencement date in lease contracts where Telenor has the right to direct the use and obtains substantially all the economic benefits from the use of an identified asset. For spectrum contracts, Telenor has chosen to account for the right to use the spectrum as a lease, where the identified asset is the frequency band that is exclusive for Telenor during the lease period. Lease payments on short-term leases (less than 12 months) and low-value asset leases (mainly office equipment) are generally expensed on a straight-line basis over the lease term. The short-term exemption does not apply to spectrum leases or leases with purchase options.

The lease liability represents the net present value of lease payments over the lease period and include fixed payments, in-substance fixed payments, non-lease components, residual value guarantees and lease incentives. The lease payments also include the exercise price of a purchase option reasonably certain to be exercised and termination penalties when termination is expected. Variable lease payments such as licence payments based on revenue sharing arrangements are expensed as incurred.

The incremental borrowing rate generally used to determine the net present value is based on the respective country’s risk-free rate for the term corresponding to the lease term, adjusted for own credit risk. Subsidiaries with external financing use the external borrowing rate corresponding to the lease term.

The non-cancellable lease period is basis for the lease liability, and periods covered by options to extend or terminate the lease are included only when it is reasonably certain the lease period will be extended. The lease liability is remeasured if the lease term or lease payments change, or there are other modifications. Significant amounts paid up-front on spectrum and other lease contracts are recognised as prepayment until commencement date.

Right-of-use assets are measured at cost, less accumulated depreciation and impairments, and adjusted for any remeasurement of lease liabilities. The right-of-use asset includes estimated costs for dismantling and removing the underlying leased asset, restoring the site on which it is located or restoring the underlying leased asset to the condition required by the terms and conditions of the lease. Non-refundable value-added tax is included as initial direct cost. The right-of-use asset is depreciated on a straight-line basis over the shorter of its estimated useful life and the lease term. Right-of-use assets where it is reasonably certain that Telenor will exercise a purchase option at the end of the lease term are not depreciated.

Key judgments and estimates

Determining the lease term can involve significant judgment for lease contracts with extension or termination options, as an assessment of whether or not it is reasonably certain that the lease period will be extended is required. The broader economics of the contract and not only contractual termination payments are basis for such assessment. For lease of land for own towers or leasing of towers from tower companies or other operators, factors considered in particular for assessing the lease term are technology development and potential changes in business models. Based on an assessment of these factors, the lease term for Telenor’s leases relating to sites will normally be within a range of 4 to 7 years. This means that the lease term for sites with renewal options shall normally be the higher of a non-cancellable period or within a range of 4 to 7 years. Some sites may be in strategically important locations and it might be more than reasonably certain that the sites will be maintained beyond 7 years. In these exceptional cases, the lease term may be up to 10 years.

Right-of-use assets

Right-of-use assets are classified based on the nature of underlying assets as follow:

For lease of network passive infrastructure (lease of tower space in networks and lease of part of buildings for own towers), land for own sites or towers and lease of buildings for office spaces, equipment and retail stores, lease agreements generally contain termination options or renewal options. These options are used to limit the period to which Telenor is committed to individual lease contracts and to maximise operational flexibility in terms of dynamic network requirements. The remaining non-cancellable period for lease contracts under network passive infrastructure is 3 years on average. The non-cancellable period for lease contracts related to land is 2 years on average, which is mainly driven by non-cancellable lease agreements in Thailand.

As a result of deteriorating macro-economic situation in Pakistan, an impairment of NOK 963 million related to right-of-use assets was recognised in 2022. Please see note 18 for further information. In 2021, due to a worsening security and human rights situation in Myanmar, Telenor made an impairment of the right of use assets and at the same time reassessed the lease term of all the lease agreements in Myanmar, limiting the lease term to one year.

The additions of spectrum licences in 2022 were related to additional spectrum fee of NOK 1.7 billion in Pakistan, which is pursuant to the Supreme Court ruling there the detailed judgement is still awaited, see further below and note 23 for more information. Moreover, the additions were related to acquisition of spectrum under 3500 MHz in Norway, 2100 MHz in Denmark, and 2600 MHz in Grameenphone. The additions of spectrum licences in 2021 were primarily related to renewal of spectrum under the 900 MHz and 1800 MHz bands in Pakistan, acquisition of spectrum under 1800 MHz and 2100 MHz bands in Grameenphone, 3500 MHz band in Sweden and 3500 MHz and 26 GHz bands in Denmark.

In 2022, the additions in network passive infrastructure were mainly related to site leases from towercos in Grameenphone, contract renewal of CAT equipment lease in dtac, tower spaces and part of building for own towers Telenor Norway and Finland. The additions in cables were mainly in Sweden and Grameenphone. The additions in building were mainly related to Telenor Real Estate, Telenor South East Asia Investment Pte Ltd., Telenor Sweden and Telenor Denmark. The additions in land were mainly related to land for own sites in dtac and Pakistan.

In 2021, the additions in network passive infrastructure were mainly related to site leases from towerco in Grameenphone, CAT equipment in dtac, tower spaces and part of building for own towers in Digi and Telenor Norway. The additions in cables were mainly in Sweden. The additions in building were mainly related to dtac and Telenor Infra. The additions in land were mainly related to land for own sites in dtac, Digi and Pakistan.

For lease of spectrum, the agreements are generally non-cancellable. Telenor has not considered periods covered by renewal options even if in some agreements the option to renew exists, given the uncertainty around terms and conditions of renewal of licences.

The following table sets forth the spectrum licences that Telenor holds as of 31 December 2022:

Telenor Pakistan’s 900 MHz and 1800 MHz spectrum licence expired on 25 May 2019, and the renewal fee was set to NOK 4.0 billion (USD 449 million) by the Pakistan Telecommunication Authority (PTA) for an extension period of 15 years. Telenor Pakistan disagreed with the terms and conditions for renewal, primarily on the price. Telenor Pakistan is of the opinion that the renewal price should have been NOK 2.5 billion (USD 291 million), which was the same as for prior renewals for other operators. Accordingly, Telenor Pakistan challenged the terms and conditions for renewal of said licence in Islamabad High Court. On 19 July 2021, the High Court decided the case in Telenor’s disfavor. Telenor Pakistan appealed the case to the Supreme Court on 31 August 2021. In December 2021, Telenor Pakistan signed the licence under protest whilst waiting for the Supreme Court’s hearing of the case. On 25 May 2022, the Supreme Court rejected the appeal. The new spectrum price is considered a variable lease payment that has become in-substance fixed, and the right-of-use asset and lease liability has been adjusted accordingly. Telenor Pakistan is still waiting for the written Supreme Court decision and will assess to file a review petition. Telenor Pakistan has paid a total of NOK 2.8 billion (USD 314 million excl. interest) of the demanded licence renewal fees. See note 18 for further information about impairment of Pakistan following the Supreme Court ruling.

Lease expenses

Expenses recognised in the income statement related to lease contracts are presented below:

Variable lease expenses of NOK 2.3 billion (NOK 2.2 billion in 2021) recognised in other operating expenses include NOK 1.7 billion (NOK 1.8 billion in 2021) related to spectrum and NOK 0.4 billion (NOK 0.3 billion in 2021) related to other lease contracts. Variable lease expenses related to spectrum agreements vary mainly with revenue, as a significant part of the expenses are based on share of revenues under the agreements. Variable lease expenses related to other lease contracts of NOK 0.4 billion (0.3 billion NOK in 2021) represent energy charges paid to lessors as part of the lease agreements for some mobile sites, and the expenses vary with the consumption of energy on those mobile sites.

NOTE 27 Financial assets and non-interest-bearing liabilities (extract)

Lease receivables

In finance leases, a lease receivable is recognised based on future expected lease payments, and finance income is allocated using a constant periodic rate of return over the lease term. In a transaction for which an underlying asset is sub-leased to a third party, the sublease is classified as a finance or operating lease by reference to the right-of-use asset arising from the head lease. See note 3 for further information about operation lease revenue.

Finance lease receivables

Telenor has recognised receivables at present value of future lease payments to be received in lease arrangements where Telenor has transferred substantially all the risks and rewards incidental to ownership of the underlying assets to the lessee. Current finance lease receivables are included in Trade and other receivables (see note 19).

During 2022, the Group recognised interest income of NOK 60 million (NOK 73 million in 2021) (note 9) related to finance lease receivables.

Dtac has Tower Service Agreement with the National Telecom Public Company Limited (NT) and under the agreement, dtac transferred towers that dtac procured under the concession agreement to operate and to provide cellular telephonic service and entered into lease agreement to use the towers. The right to use towers from NT was recognised as right-of-use asset with corresponding lease liability. Under the agreement, dtac shall itself have lease agreements for the land with landowners and shall receive compensation from NT for this. dtac recognised lease agreements as a lessee with the landowners for the land related to transferred towers to NT with related lease liabilities. Right-of-use assets related to land was derecognised on 1 January 2019 based on the sublease arrangement with NT and a finance lease receivable was recognised with reference to the tenure of the agreement with NT. The Group entered into a long-term lease with UPC on 1 April 2017 for the lease of 9 transponders on Thor 6, where the final payment from UPC will be made in January 2025. According to the agreement, substantially all the risks and rewards related to Thor 6 are transferred to UPC, and accordingly a finance lease receivable was recognised at present value, which represents the deferred payments to be received until January 2025.

The following table sets forth the maturity analysis of lease receivables:

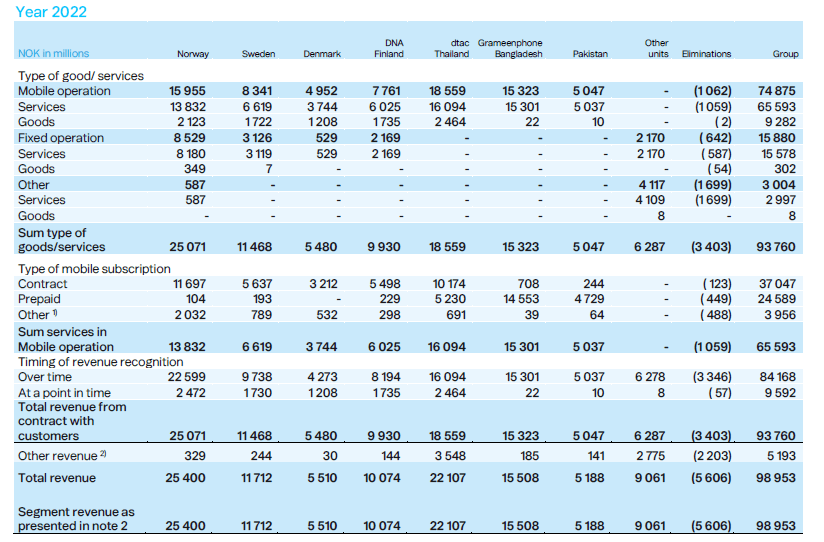

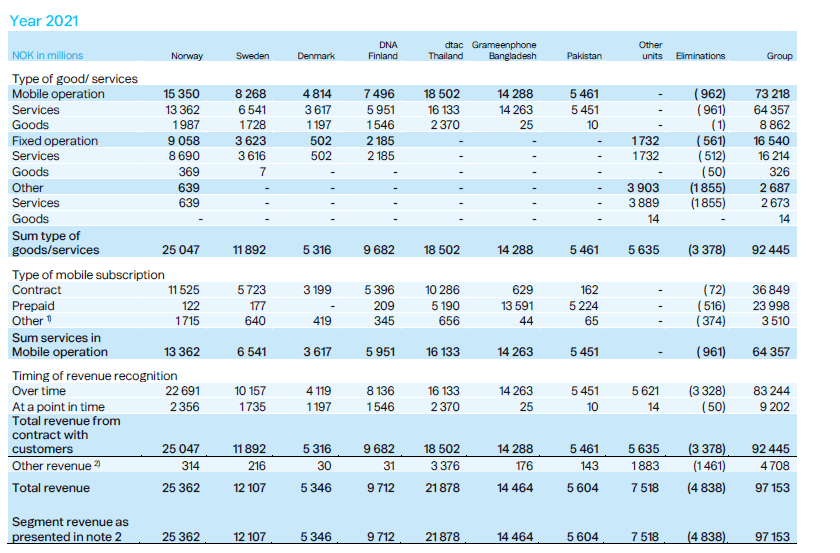

NOTE 3 Revenues (extract)

Accounting policies (extract)

Lease revenues (IFRS 16)

The Group has operating lease arrangements in which it is a lessor, mainly related to passive infrastructure sharing with other telecommunication operators. The Group has classified these leases as operating leases because they do not transfer substantially all the risks and rewards incidental to ownership of the underlying assets. Lease revenues are recognised on a straight-line basis over the lease term.

Disaggregation of revenues from contract with customers

Revenues are disaggregated by major revenue streams divided into the reportable segments as shown in note 2 in the table below.

1) Other includes revenues from other mobile and non-mobile services, refer to definitions on page 180.

2) Other revenue includes mainly lease revenue.

1) Other includes revenues from other mobile and non-mobile services, refer to definitions on page 180.

2) Other revenue includes mainly lease revenue.

Lease revenues

Other revenue of NOK 5.2 billion (NOK 4.7 billion in 2021) recognised in the income statement includes variable lease revenue of NOK 152 million (NOK 87 million in 2021) primarily relating to energy charges received from lessees based on the consumption.

The following table sets forth the maturity analysis of minimum lease payments to be received in nominal terms after the reporting date:

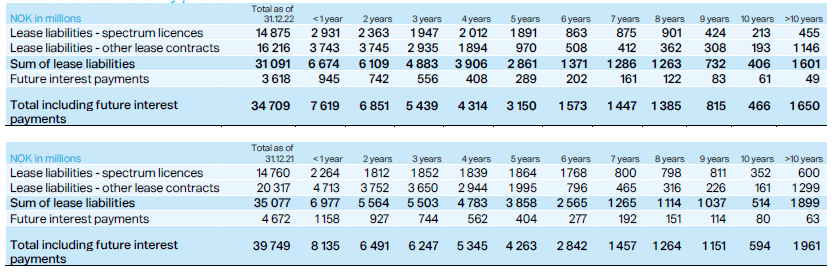

NOTE 29 Lease liabilities

This note gives further information about the lease liabilities of Telenor, such as lease liabilities per currency and subsidiary in addition to the maturity profile. Refer to note 16 for description of accounting policies and key judgments and estimates relating to lease liabilities and right-of-use assets.

Lease liabilities measured at amortised cost

Distribution of lease liabilities per currency and subsidiary as of 31 December 2022

Lease liabilities maturity profile