Asahi Group Holdings, Ltd. – Annual report – 31 December 2016

Industry: Food and drink

- Disclosures regarding the Transition to IFRS

These are the Group’s first consolidated financial statements in accordance with IFRS. The accounting policies set out in “5. Significant Accounting Policies” have been applied in preparing the consolidated financial statements for the current year (ended December 31, 2016) and the previous year (ended December 31, 2015), and the consolidated statement of financial position as of the transition date (January 1, 2015).

Exemptions in accordance with IFRS 1

An entity that adopts IFRS for the first time is required to apply the requirements under IFRS retrospectively. However, IFRS 1 “First-time Adoption of International Financial Reporting Standards” allows certain exemptions. The exemptions used by the Group are as follows:

(a) Business Combinations

The Group elected not to apply IFRS 3 “Business Combinations” retrospectively to business combinations that occurred prior to the transition date. These business combinations are accounted for under the previous GAAP (Japanese GAAP). As a result, goodwill arising from business combinations prior to the transition date is recognized at its carrying amount under Japanese GAAP.

Such goodwill was tested for impairment at the transition date, irrespective of whether or not there was any indication that the goodwill may be impaired.

(b) Deemed Cost

The Group used fair value at the transition date as deemed cost for certain items of property, plant and equipment.

(c) Cumulative Translation Difference on Foreign Operations

The Group deemed cumulative translation difference on foreign operations to be zero at the transition date.

(d) Share-based Payment

The Group did not apply IFRS 2 “Share-based Payment” to equity instruments vested prior to the transition date.

(e) Designation of Financial Instruments Recognized prior to the Transition Date

Classification under IFRS 9 is based on facts and circumstances as of the transition date, and equity instruments are designated as equity instruments measured at fair value through other comprehensive income.

Reconciliation from Japanese GAAP to IFRS

Reconciliation that is required to be disclosed on first-time adoption of IFRS is shown in the schedule below. The figures under Japanese GAAP at the transition date reflect effects of application of the “Accounting Standard for Retirement Benefits” (ASBJ Statement No. 26, May 17, 2012), “Guidance on the Accounting Standard for Retirement Benefits” (ASBJ Guidance No. 25, March 26, 2015), “Accounting Standard for Business Combinations” (ASBJ Statement No. 21, September 13, 2013), “Accounting Standard for Consolidated Financial Statements” (ASBJ Statement No. 22, September 13, 2013) and “Accounting Standard for Business Divestitures” (ASBJ Statement No. 7, September 13, 2013).

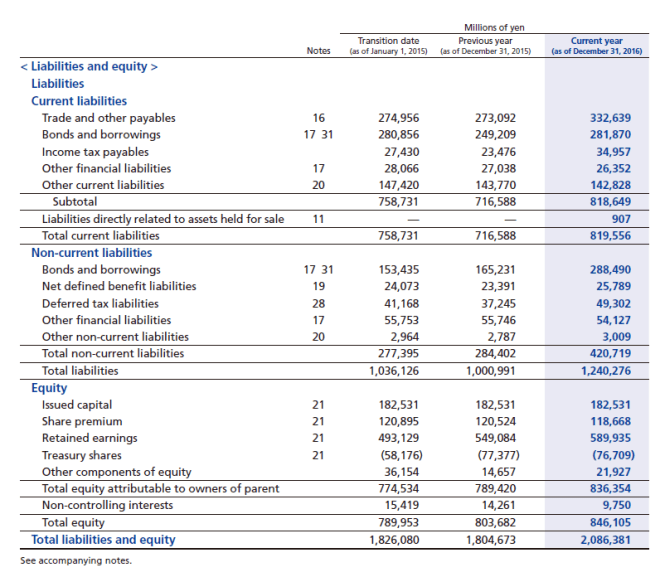

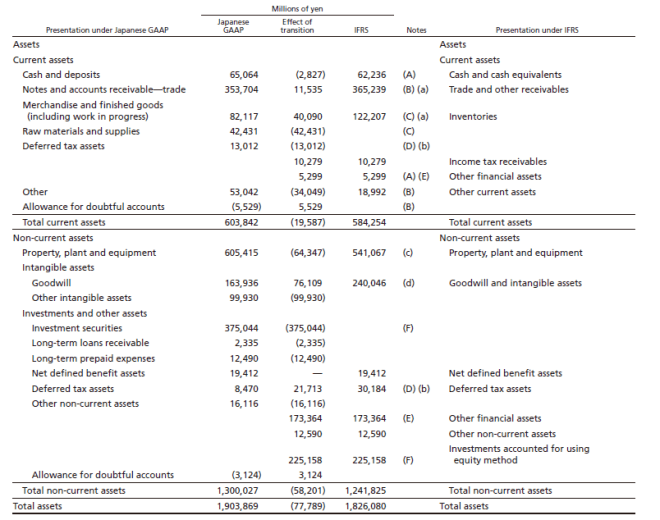

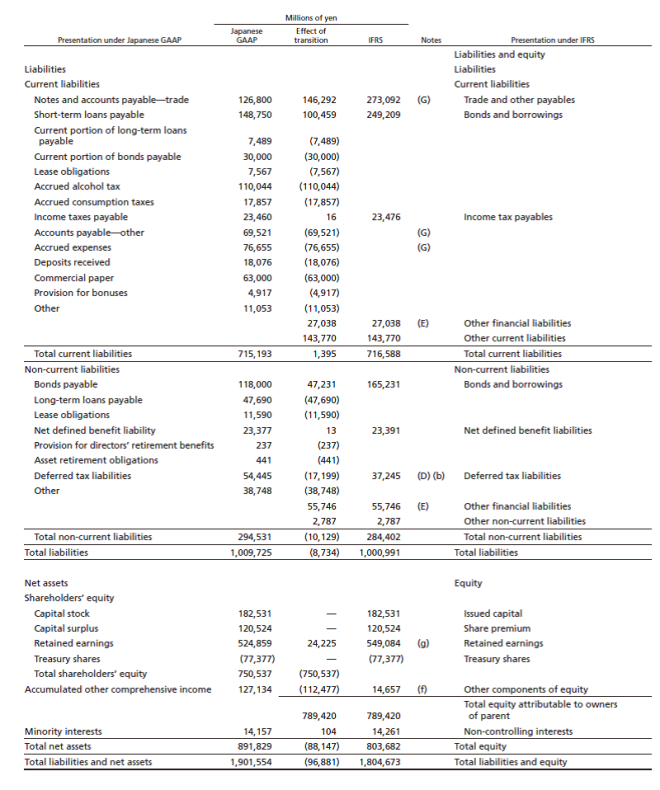

Reconciliation of Equity as of January 1, 2015 (Transition Date)

Notes to the Reconciliations as of January 1, 2015 (Transition Date)

(1) Reclassification of Presented Items

(A) Cash and Cash Equivalents

Fixed deposits with maturities exceeding three months were reclassified from “Cash and deposits” under Japanese GAAP to “Other financial assets” under IFRS.

(B) Trade and Other Receivables

“Notes and accounts receivable—trade” and “Allowance for doubtful accounts” which are presented separately and other receivables included in “Other” under Japanese GAAP are presented as “Trade and other receivables” under IFRS.

(C) Inventories

“Merchandise and finished goods (including work in progress)” and “Raw materials and supplies” which are presented separately under Japanese GAAP are presented as “Inventories” under IFRS.

(D) Deferred Tax Assets and Deferred Tax Liabilities

“Deferred tax assets” and “Deferred tax liabilities” which are presented separately under current assets and current liabilities under Japanese GAAP are presented under non-current assets and non-current liabilities under IFRS.

(E) Other Financial Assets and Other Financial Liabilities

“Other financial assets” and “Other financial liabilities” are presented separately based on the presentation requirements of IFRS.

(F) Investments accounted for using Equity Method

“Investments accounted for using equity method” which is included in “Investment securities” under Japanese GAAP is presented separately under IFRS.

(G) Trade and Other Payables

“Notes and accounts payable—trade,” “Accounts payable—other,” “Accrued expenses” and other payables which are presented separately under Japanese GAAP are presented as “Trade and other payables” under IFRS.

(2) Differences in Recognition and Measurement

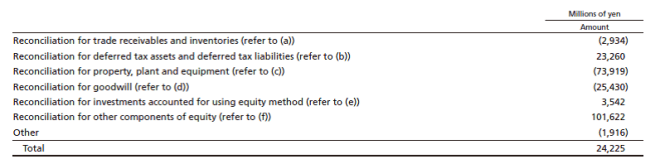

(a) Trade Receivables and Inventories

The Group recognizes revenue upon delivery of goods to customers under IFRS whereas revenue from certain types of sales of goods had been previously recognized upon shipment under Japanese GAAP. The Group recognizes expenses when it purchases goods to be kept mainly for advertisement or sales promotion whereas it had recognized those kinds of goods as inventories under Japanese GAAP. Adjustments due to those differences have been reflected in retained earnings.

(b) Deferred Tax Assets and Deferred Tax Liabilities

Deferred tax assets increased after reconsidering future taxable income which temporary deductible differences will be utilized for in accordance with IFRS. The tax effect as well as those arising from differences in accounting between Japanese GAAP and IFRS has been recognized in retained earnings.

(c) Property, Plant and Equipment

The Group recognizes certain items as property, plant and equipment which had been recognized as expenses when purchased because they are individually immaterial under Japanese GAAP, and it resulted in an increase in property, plant and equipment under IFRS. The useful lives were reconsidered upon transition to IFRS and it resulted in a decrease in accumulated depreciation of property, plant and equipment. The effect has been recognized in retained earnings. As to certain items of property, plant and equipment, the Group elected to use the fair value at the transition date as their deemed cost, and it resulted in a decrease in their value. The carrying amount of these items of property, plant and equipment under Japanese GAAP was ¥166,468 million, and their fair value was ¥88,391 million.

(d) Goodwill

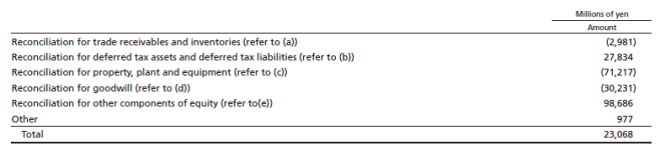

The Group recognized impairment losses as a result of impairment testing for goodwill at the transition date and deducted them from retained earnings. Impairment losses amounted to ¥15,397 million for the soft drink business in Malaysia and ¥14,833 million for the dairy product business in Malaysia, respectively, due to future cash flows that were initially expected could no longer be expected under Overseas segment which the Malaysian businesses belong to.

The recoverable amounts were based on their value in use and amounted to ¥15,748 million and ¥16,788 million, respectively. The value in use is calculated by discounting the estimated cash flows to present value, which are based on business plans and growth rates that reflect previous experience and external information and have been approved by management. Growth rates are determined with reference to factors such as inflation rates in the markets which the cash-generating units belong to. Discount rates are determined with reference to the pre-tax weighted average cost of capital for the cash-generating units. The average discount rates used in the calculation of value in use are 14.0% and 14.8% for the soft drink business and the dairy product business in Malaysia, respectively.

(e) Other Components of Equity

Cumulative translation difference on foreign operations presented in accumulated other comprehensive income under Japanese GAAP at the transition date has been fully reclassified to retained earnings since the Group has applied the exemption on transition to IFRS. Also, the Group has recognized actuarial differences arising from defined benefit plans in other comprehensive income and immediately reclassified all of them to retained earnings under IFRS, whereas actuarial differences had been subsequently reclassified to profit or loss over a certain period of time beginning from the following year in which they arise under Japanese GAAP.

(f) Retained Earnings

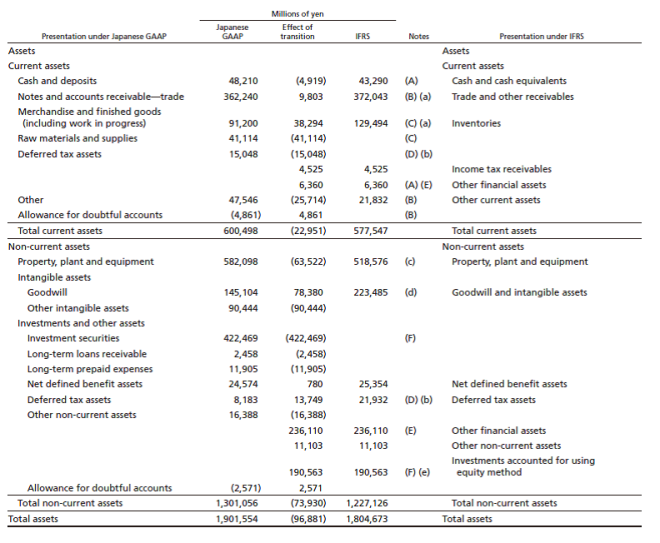

Reconciliation of Equity as of December 31, 2015

Notes to the Reconciliations as of December 31, 2015

(1) Reclassification of Presented Items

(A) Cash and Cash Equivalents

Fixed deposits with maturities exceeding three months were reclassified from “Cash and deposits” under Japanese GAAP to “Other financial assets” under IFRS.

(B) Trade and Other Receivables

“Notes and accounts payable—trade” and “Allowance for doubtful accounts” which are presented separately and other receivables included in “Other” under Japanese GAAP are presented as “Trade and other receivables” under IFRS.

(C) Inventories

“Merchandise and finished goods (including work in progress)” and “Raw materials and supplies” which are presented separately under Japanese GAAP are presented as “Inventories” under IFRS.

(D) Deferred Tax Assets and Deferred Tax Liabilities

“Deferred tax assets” and “Deferred tax liabilities” which are presented separately under current assets and current liabilities under Japanese GAAP are presented under non-current assets and non-current liabilities under IFRS.

(E) Other Financial Assets and Other Financial Liabilities

“Other financial assets” and “Other financial liabilities” are presented separately based on the presentation requirements of IFRS.

(F) Investments accounted for using Equity Method

“Investments accounted for using equity method” which is included in “Investment securities” under Japanese GAAP is presented separately under IFRS.

(G) Trade and Other Payables

“Notes and accounts payable—trade,” “Accounts payable—other,” “Accrued expenses” and other payables which are presented separately under Japanese GAAP are presented as “Trade and other payables” under IFRS.

(2) Differences in Recognition and Measurement

(a) Trade Receivables and Inventories

The Group recognizes revenue upon delivery of goods to customers under IFRS whereas revenue from certain types of sales of goods had been previously recognized upon shipment under Japanese GAAP. The Group recognizes expenses when it purchases goods to be kept mainly for advertisement or sales promotion whereas it had recognized those kinds of goods as inventories under Japanese GAAP. Adjustments due to those differences have been reflected in retained earnings.

(b) Deferred Tax Assets and Deferred Tax Liabilities

Deferred tax assets increased after reconsidering future taxable income which temporary deductible differences will be utilized for in accordance with IFRS. The tax effect as well as those arising from differences in accounting between Japanese GAAP and IFRS has been recognized in retained earnings.

(c) Property, Plant and Equipment

The Group recognizes certain items as property, plant and equipment which had been recognized as expenses when purchased because they are individually immaterial under Japanese GAAP, and it resulted in an increase in property, plant and equipment under IFRS. The useful lives were reconsidered upon transition to IFRS and it resulted in a decrease in accumulated depreciation of property, plant and equipment. The effect has been recognized in retained earnings. As to certain items of property, plant and equipment, the Group elected to use the fair value at the transition date as their deemed cost, and it resulted in a decrease in their value. The carrying amount of these items of property, plant and equipment under Japanese GAAP was ¥166,468 million, and their fair value was ¥88,391 million.

(d) Goodwill

The Group recognized impairment losses as a result of impairment testing for goodwill at the transition date and deducted them from retained earnings. Impairment losses amounted to ¥30,231 million for a business in the Overseas segment which related goodwill had been allocated to, due to future cash flows that were initially expected could no longer be expected (Please refer to (2) (d) of “Notes to the Reconciliations as of January 1, 2015 (Transition Date)” for details). Goodwill had been amortized over the estimated useful lives under Japanese GAAP, but will no longer be amortized under IFRS on and after the transition date. The effect has been recognized in retained earnings.

(e) Investments accounted for using Equity Method

Goodwill included in investments accounted for using the equity method had been amortized over the estimated useful lives under Japanese GAAP, but will no longer be amortized under IFRS on and after the transition date. The effect has been recognized in such investments.

(f) Other Components of Equity

Cumulative translation difference on foreign operations presented in accumulated other comprehensive income under Japanese GAAP at the transition date has been fully reclassified to retained earnings since the Group has applied the exemption on transition to IFRS. Also, the Group has recognized actuarial differences arising from defined benefit plans in other comprehensive income and immediately reclassified all of them to retained earnings under IFRS, whereas actuarial differences had been subsequently reclassified to profit or loss over a certain period of time beginning from the following year in which they arise under Japanese GAAP.

(g) Retained Earnings

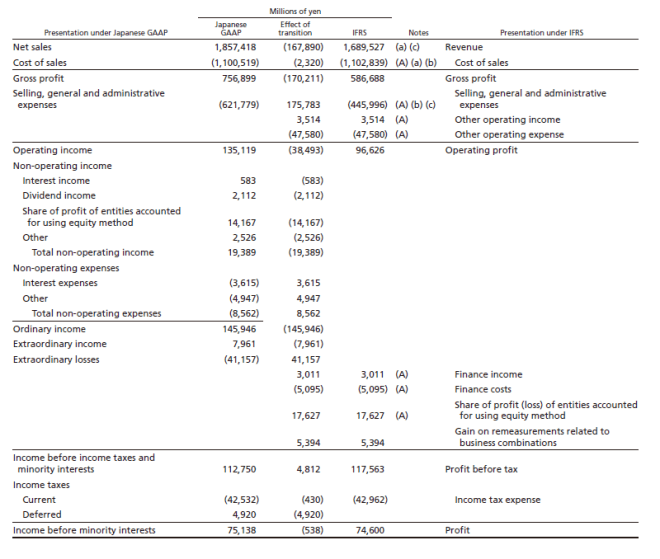

Reconciliation of Comprehensive Income for the Year ended December 31, 2015

Notes to the Reconciliations of Comprehensive Income for the Year ended December 31, 2015

(1) Reclassification of Presented Items

(A) Cost of sales, other operating income (expense), selling, general and administrative expenses, share of profit (loss) of entities accounted for using equity method, finance income, and finance costs

Items presented as non-operating income, non-operating expenses, extraordinary income, and extraordinary losses under Japanese GAAP are presented as finance income and finance costs for finance-related items, and as cost of sales, other operating income (expense), selling, general and administrative expenses, and share of profit (loss) of entities accounted for using equity method for the other items under IFRS.

(2) Differences in Recognition and Measurement

(a) Revenue and cost of sales

Net sales are recognized primarily upon shipment under Japanese GAAP, whereas revenue is recognized primarily upon delivery of goods. In addition, certain rebates and some other items were presented in selling, general and administrative expenses under Japanese GAAP, whereas they are deducted from revenue under IFRS.

(b) Cost of sales, selling, general and administrative expenses, and remeasurements of defined benefit plans

Under Japanese GAAP, actuarial gains and losses on defined benefit plans are amortized over a certain period of time, beginning from the year following the year they are incurred. However, all actuarial gains and losses are recognized in other comprehensive income and immediately reclassified to retained earnings under IFRS.

(c) Selling, general and administrative expenses

Under Japanese GAAP, certain rebates and some other items were presented as selling, general and administrative expenses, whereas they are deducted from revenue under IFRS. In addition, goodwill was amortized over the estimated useful lives under Japanese GAAP, but is not amortized under IFRS.

Reconciliation of Cash Flows for the Year ended December 31, 2015

There are no material differences between the consolidated statements of cash flows that were disclosed in accordance with Japanese GAAP and that in accordance with IFRS.