Premier Oil plc – Annual report – 31 December 2017

Industry: oil and gas

Audit and Risk Committee Report (extract)

Accounting for the refinancing

The Committee reviewed in detail the accounting for the refinancing which completed in 2017. The key judgement focussed on whether or not the modifications of the terms of each financing facility represented a substantial modification under the requirements of IAS 39 and, principally, whether the NPV of the revised cash flows discounted at the original effective interest rate were at least 10 per cent different from the discounted present value of the remaining cash flows of the original finance facility. This was assessed by management individually for each finance facility and the Committee reviewed the inputs and outputs of each assessment. The Committee was satisfied that the modified terms of the USPPs, SSL and convertible bond notes represented a substantial modification and that the modified terms of the RCF, Term Loan and retail bond notes did not represent a substantial modification. Details of the accounting for the refinancing are provided in note 15 to the financial statements on pages 150 to 153.

- Borrowings (extract)

Refinancing

In July 2017, Premier completed a comprehensive refinancing of its lending facilities (the ‘refinancing’) with all of the lenders under each facility.

Under the requirements of IAS 39, if an existing financial liability is replaced by another from the same lender, on substantially different terms, or the terms of an existing liability are substantially modified, such an exchange or modification is treated as a derecognition of the original liability and the recognition of a new liability, measured at its fair value, such that the difference in the respective carrying amounts together with any costs or fees incurred are recognised in profit or loss. IAS 39 regards the terms of exchanged or modified debt as ‘substantially different’ if the net present value of the cash flows under the new terms (including any fees paid net of fees received) discounted at the original effective interest rate is at least 10 per cent different from the discounted present value of the remaining cash flows of the original debt instrument. Where an exchange or modification of financial liabilities is not considered substantial, no gain or loss is recognised; the fees are capitalised against the carrying value of the liability and any changes to the cash flows are recognised as interest over the remaining term.

Completion of the refinancing also included a comprehensive security package, giving lenders collective security over materially all of the Group’s assets.

The RCF, Term Loan, USPPs and SSL (together the ‘Private Lenders’)

The refinancing included the following key amendments:

- Confirmation of total existing facilities of US$3.9 billion with drawn capacity preserved.

- Alignment of final maturity dates to 31 May 2021 for all facilities.

- Amendment of Premier’s financial covenants, such that the net debt to EBITDA cover ratio was 8.5x until the end of 2017 reducing to 5.0x at the end of 2018, before returning to 3.0x from the beginning of 2019.

- Interest cover ratio reduced to 1.5x before increasing to 3.0x in 2019.

- Covenant net debt (which includes issued letters of credit) to be less than US$2.95 billion at the end of 2018.

- A margin uplift of 1.5 per cent over existing pricing with an additional 1.0 per cent for the SSL lenders.

- Amendment fees of 1.0 per cent with an additional 0.5 per cent for the SSL lenders.

- Issuance of 67,234,316 equity warrants at an exercise price of 42.75 pence per share with a five-year term. In addition, 21,186,736 synthetic warrants have been issued, which have a four-year term.

- Crystallisation of the make-whole fees on the USPPs on the effective date of the refinancing totalling US$41.3 million, which was added to the principal.

The Group concluded that the amendments above represented a substantial modification of the USPPs and the SSL. The carrying values of the USPPs and the SSL have been recognised at fair value of the notes as of the completion date, which for the USPPs includes the make-whole fee added to the principal. The fair values were deemed to be equal to the principal amounts of the debt instruments, as the increase in the interest rate reflects the increased credit risk of the Group. The associated transaction costs were expensed.

The amendments are not considered to be a substantial modification to the RCF or Term Loan.

The retail bonds

Substantially the same economic terms were agreed with the retail bondholders as the Private Lenders. The key terms are:

- Maturity date extended by six months to 31 May 2021.

- Enhanced economics comprising an interest rate uplift of 1.5 per cent and amendment fees of 1.0 per cent.

- Issuance of 3,778,636 equity warrants at an exercise price of 42.75 pence per share with a five-year term. In addition, 189,116 synthetic warrants have been issued, which have a four-year term. These have been issued on the same terms as those issued to the Private Lenders.

The Group concluded that the amendments above did not represent a substantial modification to the retail bonds.

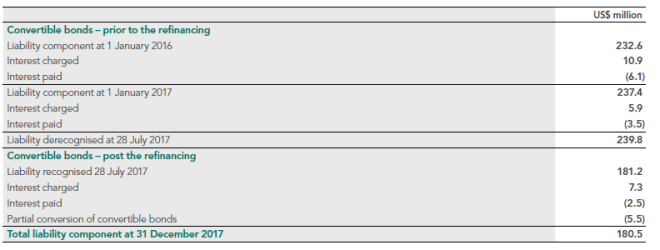

Convertible bonds

The terms of Premier’s US$245.3 million convertible bonds were also amended. The key terms are:

- Maturity date extended to 31 May 2022.

- Interest rate to remain at 2.5 per cent, to be paid, at the election of the Company, either in new shares, or from the proceeds of sale of new shares or in cash.

- Conversion price reset to 74.71 pence (from £4.21), with an exchange rate of £1:US$1.228.

- Issuance of 18,097,019 equity warrants at an exercise price of 42.75 pence per share, on the same terms as those issued to the Private Lenders.

- No cash amendment fee.

- Issuer right to require conversion at the conversion price at any time after one year if the value of Premier’s shares is at least 140 per cent of the conversion price for 25 consecutive dealing days.

The Group concluded that the above amendments represented a substantial modification to the convertible bonds. The original conversion option had no significant value, therefore the refinancing was accounted for as the settlement of the original liability component with the modified convertible, measured at its aggregate fair value. The carrying value of the debt and equity components prior to the refinancing have been derecognised from the balance sheet and new debt and equity components have been recognised at their revised fair value as of the completion date to reflect the amended terms and conversion price.

The US$58.7 million difference between the equity component of the convertible bonds prior to the completion of the refinancing and the revised fair value has been assigned to the equity reserves, giving a revised equity component of US$64.1 million.

The total interest charged on the new bonds has been calculated by applying an effective annual interest rate of 6.37 per cent pre-partial conversion and 6.23 per cent post-partial conversion to the liability component for the period since the new bonds were issued. The effective annual interest rate on the old bonds was 4.58 per cent. Subsequent to completion, by 31 December 2017 US$7.4 million of convertible bonds were converted by bondholders at 74.71 pence.

Loss on substantial modification

Costs and third-party fees, which include the USPP make-whole adjustment, amendment fees and adviser fees paid and recognition of the warrants at fair value, have been allocated to each facility as follows:

Of the total fees above, US$83.7 million in relation to the senior loan notes and convertible bonds have been expensed to the income statement in the year. The fees in relation to the bank loans and retail bonds of US$121.6 million have been capitalised against the carrying value of the debt, and are being amortised over the revised maturity of the facility.

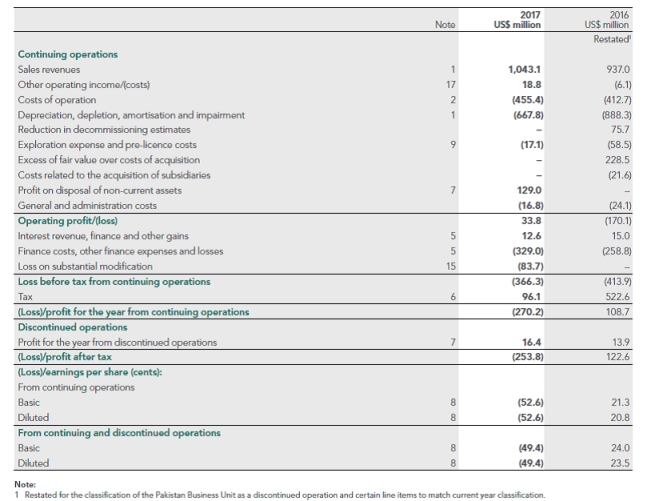

Consolidated Income Statement

For the year ended 31 December 2017