4imprint Group plc – Annual report – 31 December 2016

Industry: advertising

Financial Review (extract)

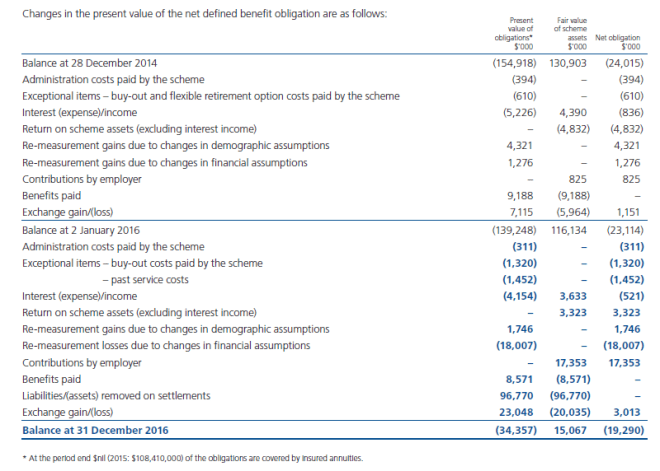

Defined benefit pension scheme

The Group sponsors a legacy defined benefit pension scheme which has been closed to new members and future accruals for several years.

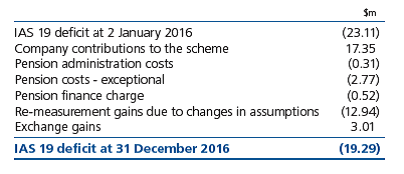

At 31 December 2016, the deficit of the scheme on an IAS 19 basis was $19.29m, compared to $23.11m at 2 January 2016.

The change in deficit is analysed as follows:

During the year, the previously bought-in benefits of the majority of pensioner members were successfully converted to buy-out status. This resulted in a remaining pension obligation that is considerably smaller, moving from around 1,600 members (1,100 pensioners and 500 deferred pensioners) in December 2015, to around 420 mainly deferred members at the 2016 year end. Individual annuities were issued to the departing pensioner members under the terms of the contracts with the insurers.

In financial terms, this meant that gross liabilities of $94.79m, and the corresponding insured asset of the same amount, were removed from the Group’s balance sheet. In order to extinguish these liabilities fully, the old scheme is in the process of being wound up. A new scheme with equivalent benefits has been set up, and members not included in the buy-out have been transferred to this scheme, except for those with small pension entitlements who opted to depart the scheme by taking winding up lump sum payments, resulting in liabilities of $1.98m and assets of an equivalent amount being removed.

In order to facilitate the buy-out process and the establishment and funding of the new scheme, a one-off contribution of £10.0m ($14.5m) was paid in the first half of 2016, as previously agreed with the Trustee. The remainder of the $17.35m total contributions during the year were in respect of an interim deficit recovery arrangement agreed with the Trustee and the funding of some transfer values out of the scheme.

At 31 December 2016, gross scheme liabilities under IAS 19 were $34.36m, and assets were $15.07m, resulting in a net liability of $19.29m. This residual net liability is higher than expected. Two primary factors influenced this: (i) adverse movements in actuarial assumptions, particularly the discount rate which moved from 3.52% in 2015 to 2.68% at the end of 2016; and (ii) a gap between the actuarial estimates of the split of liabilities between insured and non-insured members (based initially on the last full valuation in 2013 and rolled forward since then), and the actual liabilities transferred to insurers.

A new deficit recovery contribution schedule will be agreed with the Trustee during 2017. In the meantime, the current interim contribution of around £2.3m per year will continue to be paid into the scheme.

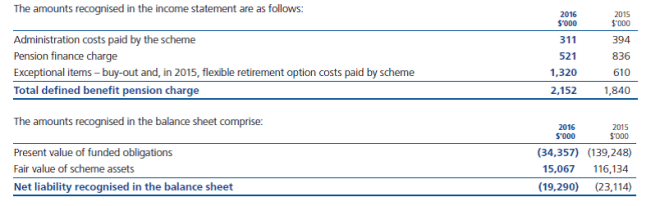

Exceptional items include $1,320,000 (2015: $610,000) incurred and paid by the defined benefit pension scheme, in respect of the buy-out and, in 2015, the flexible retirement option.

Direct cash expenditure by the Group in respect of the exceptional items in 2016 was $172,000 (2015: $248,000).

17 Employee pension schemes (extract 1)

The Group also sponsors a UK defined benefit pension scheme which is closed to new members and future accrual.

During the year, the buy-in of the benefits of the majority of pensioner members was converted to a buy-out and liabilities and assets (the latter being the insurance policies purchased on buy-in) of $94.79m have been removed from the balance sheet. To facilitate the buy-out it was necessary to initiate the process of winding up the existing defined benefit scheme and to create a new defined benefit scheme, with equivalent benefits, for pensioner and deferred members not included in the buy-out. These members were transferred to this new scheme, except for those with small value pension pots who opted to take winding up lump sum payments of their pension entitlement ($1.98m of assets and liabilities removed).

17 Employee pension schemes (extract 2)