Stellantis N.V. – Annual report – 31 December 2021

Industry: automotive

Merger of Groupe PSA and FCA

Timeline of the merger and business combination date

On December 17, 2019, FCA and PSA entered into a combination agreement providing for the combination of FCA and PSA through a cross-border merger, with FCA as the surviving legal entity in the merger (“Stellantis”).

On September 14, 2020, FCA and PSA agreed to amend the combination agreement. According to the combination agreement amendment, the FCA Extraordinary Dividend, to be paid to former FCA shareholders was reduced to €2.9 billion, with PSA’s 46 percent stake in Faurecia planned to be distributed to all Stellantis shareholders promptly after closing following approval of the Stellantis board and shareholders.

On January 4, 2021, PSA and FCA held their respective extraordinary general shareholder meetings in order to, among other matters, approve the merger transaction. The respective shareholder meetings approved the merger. Following the respective shareholder approvals and receipt of the final regulatory clearances, FCA and PSA completed the legal merger. The conditions agreed to as part of the regulatory clearance will not have a material impact on the cash flows or financial positions for Stellantis.

On January 17, 2021, the board of directors was appointed, the Stellantis articles of association became effective and the combined company was renamed Stellantis On this date, the Stellantis management and board of directors collectively obtained the power and the ability to control the assets, liabilities and operations of both FCA and PSA. As such, under IFRS 3, January 17, 2021 is the acquisition date for the business combination (see the following paragraph “Accounting for the merger and Identification of the accounting acquirer” for further details on the accounting for the transaction).

On January 29, 2021, the approximately €2.9 billion extraordinary dividend was paid to holders of FCA common shares of record as of the close of business on Friday, January 15, 2021.

On March 22, 2021, the distribution by Stellantis to the holders of its common shares was completed of 53,130,574 ordinary shares of Faurecia and €302 million which are the proceeds received by PSA in November 2020 from the sale of ordinary shares of Faurecia, both net of shares and cash retained to serve the GM Warrants.

Primary reasons for the business combination

The following are the primary reasons for the merger:

- A New Industry Leader with resilience. The merger created a global automaker and mobility provider, with a balanced and profitable global presence with a portfolio covering all key vehicle segments.

- Greater Geographic Balance. The merger added scale and substantial geographic balance through leveraging FCA’s strength in North America and Latin America with PSA’s position in Europe, as well as creating opportunities to reshape the strategy in other geographic regions, primarily China;

- Stronger Platform for Innovation. The combined group is expected to be able to leverage its capabilities in new energy vehicles, sustainable mobility, autonomous driving and connectivity;

- Synergies. The merger synergies are planned to be achieved in the following four areas: technology, platforms and products, purchasing, selling, general and administrative expenses (SG&A) and all other functions, such as logistics, supply chain, quality and after-market operations.

Accounting for the merger and identification of the accounting acquirer

The merger has been accounted for by Stellantis using the acquisition method of accounting in accordance with IFRS 3, which requires the identification of the acquirer and the acquiree for accounting purposes. Based on the assessment of the indicators under IFRS 3 and consideration of all pertinent facts and circumstances, management determined that PSA was the acquirer for accounting purposes and as such, the merger has been accounted for as a reverse acquisition. In identifying PSA as the acquiring entity, notwithstanding that the merger was effected through an issuance of FCA shares, the most significant indicators were (i) the composition of the combined group’s board, which is composed of eleven directors, six of whom were to be nominated by PSA, PSA shareholders or PSA employees, or were current PSA executives, (ii) the combined group’s first CEO, who was vested with the full authority to individually represent the combined group, and was the president of the PSA Managing Board prior to the merger, and (iii) the payment of a premium by pre-merger shareholders of PSA.

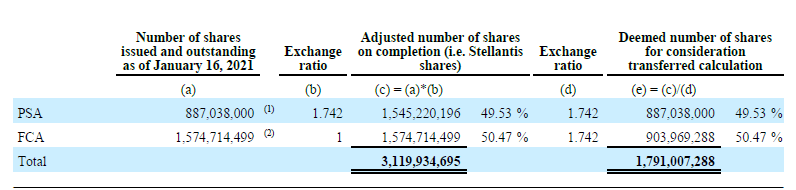

Computation of the consideration transferred

PSA shareholders received 1.742 FCA common shares for each PSA ordinary share held immediately prior to the merger as consideration in connection with the merger, which represented 1,545,220,196 shares. However, as required by IFRS 3, the consideration transferred is calculated as if PSA, as the accounting acquirer, issued shares to the shareholders of the accounting acquiree, FCA. The value of the consideration transferred has been measured based on the closing price of PSA’s shares of €21.85 per share on January 15, 2021, which was the final share price of PSA prior to the acquisition date. The number of PSA shares that PSA is deemed to issue to FCA shareholders under reverse acquisition accounting provides the former FCA shareholders with the same ownership in the combined group as obtained in the merger. Based on the number of shares of FCA and PSA that are issued and outstanding as of January 16, 2021, the respective percentages of ownership of PSA and the former FCA shareholders are as follows:

(1) Number of shares as of January 16, 2021, net of 7,790,213 treasury shares.

(2) The number of shares as of January 16, 2021 includes 7,195,225 shares that vested during 2020 in connection with FCA’s Equity Incentive Plan

In addition to the above, in line with the guidance in IFRS 2 – Share-based payment and IFRS 3 – Business combinations, included within consideration transferred is a portion of the fair value of the share-based awards to former FCA employees. As a result of the merger, each outstanding FCA Performance Share Units (“PSU”) award and each outstanding FCA Restricted Stock Units (“RSU”) award has been replaced by Stellantis RSU awards, which will continue to be governed by the same terms and conditions, including service-based vesting terms. Both the FCA PSU Adjusted EBIT and PSU Total Shareholder Return (“TSR”) awards were deemed to be satisfied at target upon conversion to Stellantis RSU awards. The portion of the fair value of the share-based payment awards that is included in the consideration transferred has been determined by multiplying the fair value of the original FCA awards as of January 16, 2021 by the portion of the requisite service period that elapsed prior to the merger divided by the total service period.

The computation of the consideration transferred under reverse acquisition accounting is summarized as follows:

Calculation of Goodwill

Goodwill arising from the acquisition was determined as follows:

Goodwill recognized on the acquisition relates to the expected growth, synergies, know-how and the value of FCA’s workforce, which cannot be separately recognized as an intangible asset. This goodwill has been allocated to the Company’s operating segments and is not expected to be deductible for tax purposes.

Purchase Accounting

The IFRS 3 acquisition method of accounting applies the fair value concepts defined in IFRS 13 – Fair Value Measurement (“IFRS 13”) and requires, among other things, the assets acquired and the liabilities assumed in a business combination to be recognized by the acquirer at their fair values as of the acquisition date, with certain exceptions. As a result, the acquisition method of accounting has been applied and the assets and liabilities of FCA have been recorded at their respective fair values, with limited exceptions as permitted by IFRS 3. The excess of the consideration transferred over the fair value of FCA’s assets acquired and liabilities assumed has been recorded as goodwill. PSA’s assets and liabilities together with PSA’s operations will continue to be recorded at their pre-merger historical carrying values for all periods presented in the consolidated financial statements of Stellantis. Following the completion of the merger, the earnings of the combined group reflect the impacts of purchase accounting adjustments, including changes in amortization and depreciation expense for acquired assets.

The identifiable assets acquired and identifiable liabilities assumed of FCA, as detailed below, have been measured at their acquisition date (January 17, 2021) fair value, with limited exceptions as permitted by IFRS 3. The fair values assigned to the assets acquired and liabilities assumed are final.

Intangible assets

The fair value of brands (Jeep, Ram, Dodge, Fiat, Maserati, Alfa Romeo and Mopar) was determined through an income approach based on the relief from royalty method, which requires an estimate of future expected cash flows. The useful life associated with the brands is determined to be indefinite.

For capitalized development expenditures, fair values have been assessed according to a multi-criteria approach based on relief from royalty method and an excess-earning method. The fair value for the Dealer network has been assessed using the replacement cost method.

Property, plant and equipment

The fair value of property, plant and equipment was determined primarily through the replacement cost method, which requires an estimation of the physical, functional and economic obsolescence of the related assets. A market approach, which requires the comparison of the subject assets to transactions involving comparable assets, was applied to determine the preliminary fair value of land. The fair value of certain assets was determined through an income approach.

Equity method investments

The fair value of equity method investments was determined based on quoted market prices, where available, or through a combination of the dividend discount model, the trading multiples method and the regression analysis method.

Deferred taxes

Deferred tax assets and liabilities were calculated on the fair values using the statutory tax rates applicable in the relevant jurisdictions where the related temporary differences are expected to reverse in future periods. Recognized deferred tax assets were limited to the amount of deferred tax liabilities and taxable profits expected in the foreseeable future. The tax impacts which are directly linked to the merger and migration of Stellantis N.V. tax residency from the UK to the Netherlands have been reflected in goodwill.

Inventories

The fair value of work-in-process and finished goods Inventories was determined as the estimated selling prices, less the sum of (i) the cost to complete work-in-process, (ii) the cost of disposal, (iii) a reasonable profit allowance for the selling effort, (iv) an implied brand royalty charge and (v) holding costs. The book value of certain precious metals has been adjusted to reflect their respective fair values using market prices as of the merger date. The book value of all other raw materials, which are measured at the lower of cost and net realizable value and which have a high turnover, are considered to approximate fair value.

Financial liabilities

Fair value of financial liabilities were based on quoted market prices for listed debt and based on discounted cash flow models for debt that is not listed.

The acquired lease liability was measured using the present value of the remaining lease payments at the acquisition date. The right-of-use assets were measured at an amount equal to the lease liabilities and adjusted to reflect the terms of certain leases relative to market terms.

Employee benefits

The present value of defined benefit obligations has been measured using actuarial techniques and actuarial assumptions by using the Projected Unit Credit Method. Plan assets have been measured at fair value.

Trade receivables and Receivables from financing activities

Included within the identifiable assets acquired were trade receivables with a fair value of €1,970 million and gross contractual amount of €2,181 million, of which €211 million was not expected to be collected. Included within the identifiable assets acquired were receivables from financing activities with a fair value of €1,888 million and gross contractual amount of €1,903 million, of which €15 million was not expected to be collected.

Contingent liabilities

As a result of the acquisition an incremental contingent liability of €163 million has been recognized for the potentially higher CAFE penalty base rate on vehicle shipments prior to the merger date. Refer to Note 26, Guarantees granted, commitments and contingent liabilities for additional information.

Although the specific timing of any outflow is uncertain, as a result of the acquisition, we have also recognized €141 million of contingent liabilities related to various matters, which are primarily related to indirect tax matters in Brazil.

Pro forma impact on revenues and net profit

From the acquisition date to December 31, 2021, the acquired business of FCA contributed revenues of approximately €100 billion and net profit of approximately €9 billion to the Company. If the acquisition had occurred on January 1, 2021, the Company’s consolidated revenues and consolidated net profit after tax for the year ended December 31, 2021 would have been €152 billion and €14 billion respectively.

Faurecia distribution and deconsolidation

Following agreement between FCA and PSA, PSA announced on October 29, 2020 the sale of approximately 9.7 million ordinary shares of Faurecia, representing approximately 7 percent of Faurecia’s outstanding share capital, with proceeds of approximately €308 million. This sale was recorded as a transaction with non-controlling interests. According to the combination agreement amendment, PSA’s 39.34 percent stake in Faurecia as well as the proceeds from the 7 percent sale were intended to be distributed to all Stellantis shareholders promptly after the closing of the merger. At December 31, 2020, Faurecia continued to be consolidated within continuing operations of PSA’s consolidated financial statements, as PSA concluded that Faurecia was not readily available for distribution until the merger was approved by PSA and FCA shareholders.

On January 12, 2021, PSA (i) converted the manner in which it held its remaining Faurecia ordinary shares resulting in the loss of the double voting rights attached to such Faurecia ordinary shares and (ii) caused its representatives on the board of directors of Faurecia to resign effective January 11, 2021. As a result of its loss of control over Faurecia on January 12, 2021, PSA discontinued the consolidation of Faurecia, recognizing a gain of €515 million after tax, with Faurecia being reported retrospectively as a discontinued operation in 2021 until Faurecia was distributed by Stellantis in March 2021. The remaining 39.34 percent investment in Faurecia has been accounted for as an investment in a non-consolidated entity measured at fair value under IFRS 9. During the year ended December 31, 2021, a gain of €475 million after tax was recognized up to the distribution.

On January 25, 2021, the extraordinary general meeting of shareholders (“EGM”) was convened, in order to approve the distribution by Stellantis to the holders of its common shares of up to 54,297,006 ordinary shares of Faurecia and up to €308 million which are the proceeds received by PSA in November 2020 from the sale of ordinary shares of Faurecia. The EGM was held on March 8, 2021 and the distribution occurred on March 22, 2021 resulting in 53,130,574 ordinary shares of Faurecia and €302 million in cash distributed.

The following table summarizes the operating results of Faurecia that were excluded from the Consolidated Income Statement for the years ended December 31, 2020 and 2019:

(1) Amounts presented are not representative of the income statement of Faurecia on a stand-alone basis; amounts are net of transactions between Faurecia and other companies of the Company.

The operating results of Faurecia during the period from January 1, 2021 to its deconsolidation on January 11, 2021 were not material and the loss of control was treated as having taken place on January 1, 2021.

Consolidated Statement of Financial Position

The following summarizes the impact of reclassifications made to align previously reported assets and liabilities of PSA to the presentation adopted by Stellantis:

The reclassifications made to align previously reported assets and liabilities of PSA to the presentation adopted by Stellantis are mainly driven by the following criteria:

- Certain assets and liabilities expected to be recovered or settled after more than twelve months and previously classified as “current” by PSA were reclassified as “non-current” to conform to the operating cycle criteria adopted by Stellantis.

- PSA presented separately certain financial assets and liabilities for “manufacturing and sales companies” and for “finance companies” whereas Stellantis presentation is on a group basis only. As a result of the alignment, Equity method Investments, Other non-current financial assets and Cash and cash equivalents have been aggregated into a single line for each item.

- PSA combined in the same line the intangible assets with indefinite useful lives and those with definite useful lives, while Stellantis presents the intangible assets with indefinite useful lives in combination with the Goodwill. A reclassification has been made on historical PSA presentation accordingly.

- In accordance with IFRS 3 – Business Combinations, as applied to a reverse acquisition, the share capital of Stellantis reflects the share capital of the legal acquirer, FCA N.V. with the difference between share capital of the legal acquirer and the accounting acquirer, PSA, being aggregated and shown as part of retained earnings and other reserves.

Consolidated Income Statement The following summarizes the impact of reclassifications made to align the previously reported results of PSA to the presentation adopted by Stellantis and the presentation of Faurecia as a discontinued operation in line with IFRS 5, Noncurrent Assets Held for Sale and Discontinued Operations:

The following reclassifications have been made to align PSA’s historical income statement for the years ended December 31, 2020 and 2019 with Stellantis’ presentation following the merger.

- Reclassification of warranty expense from Selling, general and administrative expenses to Cost of goods and services sold.

- (ii) Reclassification of impairment expense from Impairment of CGUs to Cost of revenues and Research and development expenses.

- (iii) Reclassification of Other operating income (expense) to Gain on disposal of investments, Cost of revenues and Selling general and other costs.

- (iv) Combination of Financial income and Financial expense into Net financial expenses.

- (v) Combination of Current taxes, Deferred taxes and Income Taxes into Tax expense.

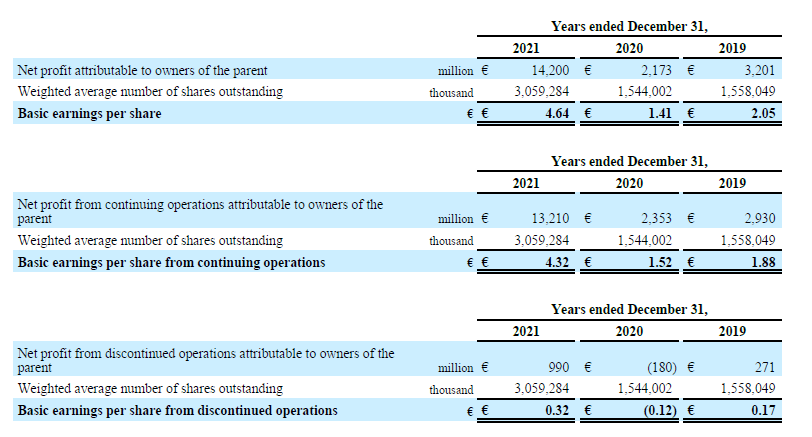

28. Earnings per share

Basic earnings per share

Basic earnings per share for the years ended December 31, 2021, 2020 and 2019 was determined by dividing the Net profit attributable to the equity holders of the parent by the weighted average number of shares outstanding during each period.

The following tables provide the amounts used in the calculation of basic earnings per share:

Diluted earnings per share

In order to calculate the diluted earnings per share, the weighted average number of shares outstanding was increased to take into consideration the theoretical effect of potential common shares that would be issued for the restricted and performance share units outstanding and unvested at December 31, 2021, 2020 and 2019 (Note 19, Share-based compensation), as determined using the treasury stock method. Additionally, the weighted average number of shares outstanding was increased to reflect the 39,727,324 GM warrants issued by PSA in 2017, that will become exercisable in July 2022.

2020 and 2019 weighted average number of shares of former PSA have been adjusted by the exchange ratio of 1.742 to provide comparability in accordance with IFRS 3 – Business Combinations.

There were no instruments excluded from the calculation of diluted earnings per share because of an anti-dilutive impact for the years ended December 31, 2021, 2020 and 2019 except for the calculation of diluted earnings per share from discontinued operations which reported a loss in 2020.

The following tables provide the amounts used in the calculation of diluted earnings per share: