Veolia Environnement – Annual report – 31 December 2016

Industry: utilities

NOTE 5 OPERATING ACTIVITIES (extract 1)

Environmental management services provided by Veolia include drinking water treatment and distribution services, waste water and sanitation services, and waste management and Energy business. They also encompass the design, construction and, where applicable, funding of necessary facilities to supply such services which are provided to industrial and service sector companies, public authorities and private individuals.

The range of business models used by the Group results in a variety of contractual forms specific to each business and adapted to local jurisdiction constraints and the nature and needs of customers (public or private).

The Group primarily conducts its activities under concession, construction (non-concession), lease and operation and maintenance contracts.

Concession arrangements (IFRIC 12)

In the conduct of activities, Veolia provides collective general interest services (distribution of drinking water and heating, household waste collection and/or treatment, etc.). These services are generally managed by Veolia under contracts entered into at the request of public sector bodies, which retain control over these collective services.

Concession arrangements involve the transfer of operating rights for a limited period, under the control of the local authority, using dedicated facilities built by Veolia, or made available to it for or without consideration:

- These contracts define “public service obligations” in return for remuneration. The remuneration is based on operating conditions, continuity of service, price rules and obligations with respect to the maintenance/replacement of installations. The contract determines the conditions for the transfer of installations to the local authority or a successor at its term;

- Veolia can, in certain cases, be responsible for a given service as it holds the service support network (water/heat distribution network, wastewater treatment network). Such situations are the result of full or partial privatizations. Provisions impose public service obligations and the means by which the local authority may recover control of the concession holder.

These contracts generally include price review clauses. These clauses are mainly based on cost trends, inflation, changes in tax and/or other legislation and occasionally on changes in volumes and/or the occurrence of specific events changing the profitability of the contract.

In addition, the Group generally assumes a contractual obligation to maintain and repair facilities managed under public service contracts.

The nature and extent of the Group’s rights and obligations under these different contracts differ according to the public services rendered by the different Group businesses: Water, Waste, Energy.

WATER

Veolia manages municipal drinking water and/or waste water services, which are described in Chapter 1 Section 1.3 of the Registration Document.

In France, these services are primarily rendered under public service delegation “affermage” contracts with a term of 8 to 20 years. They can use specific assets, such as distribution or wastewater treatment networks and drinking water or wastewater treatment plants, which are generally provided by the concession grantor and returned to it at the end of the contract.

Abroad, Veolia renders its services under contracts which reflect local legislation, the economic situation of the country and the investment needs of each partner. These contracts generally have a term of between 7 and 40 years. Contracts can also be entered into with public entities in which Veolia purchased an interest on their partial privatization. The profitability of these contracts is not fundamentally different from other contracts, but operations are based on a partnership agreement with the local authority.

WASTE

Both in France and abroad, the main concession arrangements entered into by Veolia concern the treatment and recovery of waste in sorting units, landfills and incineration. These contracts have an average term of 10 to 30 years.

ENERGY

Veolia has developed a range of energy management activities: heating and cooling networks, thermal and multi-technical services, industrial utilities, installation and maintenance of production equipment, and integration services for the comprehensive management of buildings.

The main contracts concern the management of heating and air-conditioning networks under urban concessions or on behalf of local authorities.

In Eastern Europe, Veolia provides services under mixed partial privatizations or through public-private partnerships with local authorities responsible for the production and distribution of thermal energy.

The characteristics of these contracts vary significantly depending on the country and activities concerned.

“Financial asset model”

The Group applies the financial asset model for the accounting recognition of these concession arrangements, when the concession grantor contractually guarantees the payment of amounts specified or determined in the contract or the shortfall, if any, between amounts received from users of the public service and amounts specified or determined in the contract.

Financial assets resulting from the application of IFRIC 12 are recorded in the Consolidated Statement of Financial Position under the heading “Operating financial assets” and recognized at amortized cost.

Unless otherwise indicated in the contract, the effective interest rate is equal to the weighted average cost of capital of the entities carrying the assets concerned.

Cash flows relating to these operating financial assets are included in Net cash from (used in) investing activities in the Consolidated Cash Flow Statement.

Pursuant to IAS 39, an impairment loss is recognized if the carrying amount of these assets exceeds the present value of future cash flows discounted at the initial EIR.

Revenue associated with this financial model includes:

- revenue recorded on a completion basis, in the case of construction operating financial assets (in accordance with IAS 11);

- the remuneration of the operating financial asset recorded in Revenue from operating financial assets (excluding principal payments);

- service remuneration.

“Intangible asset model”

The intangible asset model applies where the Group is paid by the users or where the concession grantor has not provided a contractual guarantee in respect of the recoverable amount. The intangible asset corresponds to the right granted by the concession grantor to the operator to charge users of the public service in remuneration of concession services provided by the operator under the concession arrangement.

Financial assets resulting from the application of IFRIC 12 are recorded in the Consolidated Statement of Financial Position under the heading “Concession intangible assets”, as described in note 1.2.4, and generally amortized on a straight-line basis over the term of the agreement.

Cash outflows, that is disbursements, relating to the construction of infrastructures under concession arrangements accounted using the “intangible asset model” are presented in Net cash from (used in) investing activities in the Consolidated Cash Flow Statement, while cash inflows are presented in Net cash from operating activities.

Under the intangible asset model, Revenue includes:

- revenue recorded on a completion basis for assets and infrastructure under construction (in accordance with IAS 11);

- service remuneration.

“Mixed or bifurcation model”

The choice of the financial asset or intangible asset model depends on the existence of payment guarantees granted by the concession grantor.

However, certain contracts may include a payment commitment on the part of the concession grantor covering only part of the investment, with the remaining balance covered by the remuneration from services charged to users.

Where this is the case, the investment amount guaranteed by the concession grantor is recognized under the financial asset model and the residual balance is recognized under the intangible asset model.

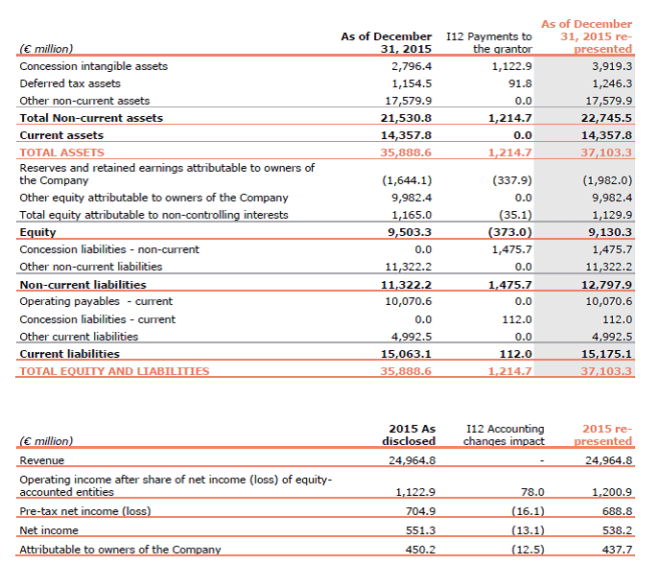

1.2.4 IFRIC 12 clarification

On July 12, 2016, the IFRS Interpretations Committee issued clarifications to IFRIC 12, Service Concession Arrangements, concerning the treatment of payments made by an operator to a grantor.

Where payments made by an operator to a grantor do not give a right to a distinct good or service or a right of use that meets the definition of a lease, and where the intangible asset model is applied, fixed payments to be made under the concession arrangement are recognized as an intangible asset representing the right to charge users of the public service through a concession liability, in the amount of the present value of amounts payable over the term of the concession arrangement.

On the publication of these clarifications the Group launched an inventory and analysis of its concession arrangements in order to identify the existence of any payments concerned by the clarifications to IFRIC 12.

The main concession arrangements identified by this review are located in the Czech Republic and Slovakia, and particularly in the Water businesses and concern contracts accounted for using the intangible asset model. IFRIC 12 clarification has no impact on contracts managed by the Group and relating to financial asset model.

The Group consolidated financial statements for the year ended December 31, 2015 were therefore re-presented to take account of the amendments resulting from these new provisions and two new balance sheet headings were created to reflect the debt resulting from the application of this clarification : non-current and current liabilities.

As a reminder, the impact on equity as of January 1, 2015 totals €351.5 million.

The impacts can be summarized as follows:

NOTE 5 OPERATING ACTIVITIES (extract 2)

5.4 Non-current and current operating financial assets

Operating financial assets comprise financial assets resulting from the application of IFRIC 12 on accounting for concession arrangements and from the application of IFRIC 4 on accounting for leases.

Concession arrangements

Pursuant to IFRIC 12, when the operator has an unconditional right to receive cash or another financial asset from the grantor in remuneration for concession services, the financial asset model applies. In this context, the infrastructures managed under these contracts cannot be recorded in assets of the operator as property, plant and equipment, but are recorded as financial assets.

Investment grants received in respect of concession arrangements are generally definitively earned and, therefore, are not repayable. In accordance with the option offered by IAS 20, these grants are presented as a deduction from intangible assets or financial assets depending on the applicable model following an analysis of each concession arrangement (IFRIC 12). Under the financial asset model, investment grants are equated to a means of repaying the operating financial asset.

During the construction phase, a financial receivable is recognized in the Consolidated Statement of Financial Position and revenue in the Consolidated Income Statement, in accordance with the percentage of completion method laid down in IAS 11 on construction contracts.

Financial receivables are initially measured at the lower of fair value and the sum of discounted future cash flows and subsequently recognized at amortized cost using the effective interest method.

After a review of the contract and its financing, the implied interest rate on the financial receivable is based on either the Group financing rate and /or the borrowing rate associated with the contract.

Leases

IFRIC 4 seeks to identify the contractual terms and conditions of agreements which, without taking the legal form of a lease, convey a right to use a group of assets in return for payments included in the overall contract remuneration. It identifies in such agreements a lease contract which is then analysed and accounted for in accordance with the criteria laid down in IAS 17, based on the allocation of the risks and rewards of ownership between the lessor and the lessee.

The contract operator therefore becomes the lessor with respect to its customers. Where the lease transfers the risks and rewards of ownership of the asset in accordance with IAS 17 criteria, the operator recognizes a financial asset to reflect the corresponding financing, rather than an item of property, plant and equipment.

Movements in the net carrying amount of non-current and current operating financial assets during 2016 are as follows:

| (1) Impairment losses are recorded in operating income. |

| (2) New operating financial assets presented in the Consolidated cash flow statement equal new operating financial assets presented above €113.4 million, net of the relating acquisition debt €1.1 million as of December 31, 2016. |

The principal new operating financial assets in 2016 mainly concern the increase in financial receivables for pre-existing contracts, in particular in the following operating segments:

- Europe excluding France, in the amount of €59.5 million, primarily following investments in Germany under the Braunschweig contract of €20.4 million;

- Rest of the World, in the amount of €33.7 million, primarily following investments by Société d’Energie et d’Eau in Gabon of €27.9 million.

The principal repayments and disposals of operating financial assets in 2016 concern the following operating segments:

- Rest of the World in the amount of -€105.9 million;

- Europe excluding France, in the amount of -€64.1 million;

- France in the amount of -€28.8 million.

Foreign exchange translation gains and losses on current and non-current operating financial assets mainly concern movements in the pound sterling (-€73.5 million) and the Chinese renminbi (-€8.6 million) against the euro.

Operating financial assets held by the Group in countries considered high-risk by the International Monetary Fund are not material in amount.

Breakdown of operating financial assets by operating segment:

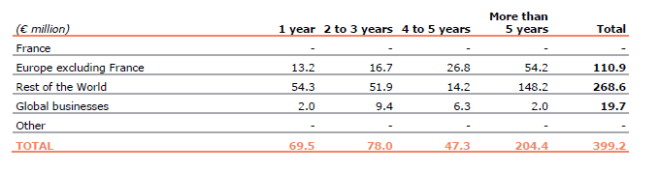

IFRIC 4 operating financial assets maturity schedule:

IFRIC 12 operating financial assets maturity schedule:

5.5 Concession liabilities

Concession financial liabilities result from the application of IFRIC12 on the accounting treatment of concessions (see Note 1.2.4).

Movements in non-current and current concession liabilities in 2016 break down as follows:

NOTE 7 GOODWILL, INTANGIBLE ASSETS AND PROPERTY, PLANT AND EQUIPMENT (extract)

7.2 Intangible assets (extract)

Intangible assets are identifiable non-monetary assets without physical substance. They mainly consist of certain assets recognized in respect of concession arrangements (IFRIC 12).

Intangible assets purchased separately are initially measured at cost in accordance with IAS 38. Intangible assets acquired through business combinations are recognized at fair value separately from goodwill. Subsequently, intangible assets are measured at cost less accumulated amortization and impairment losses. They are tested for impairment where there is indication of loss in value.

7.2.1 Concession intangible assets

Concession intangible assets correspond to the right of the concession holder to bill users of a public service in return for construction services provided by it to the concession grantor under public service contracts in accordance with IFRIC 12, Service Concession arrangements.

This concession holder right is equal to the fair value of the construction of the concession infrastructure plus borrowings costs recognized during the construction period. It is amortized over the contract term in accordance with an appropriate method reflecting the rate of consumption of the concession asset’s economic benefits as from the date the infrastructure is brought into service.

Investment grants received in respect of concession arrangements are generally definitively earned and, therefore, are not repayable. In accordance with the option offered by IAS 20, these grants are presented as a deduction from intangible assets and reduce the amortization charge in respect of the concession intangible asset over the residual term of the concession arrangement.

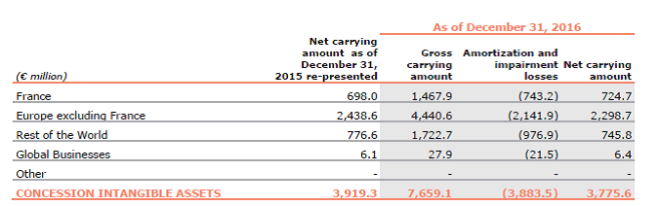

Movements in the net carrying amount of concession intangible assets during 2016 are as follows:

Additions mainly concern France (€151.6 million), Europe excluding France (€67.8 million) and the Rest of the World (€60.9 million).

Other movements mainly concern Europe excluding France in the amount of €135.5 million.

Foreign exchange translation gains and losses are primarily due to movements in the pound sterling (-€106.2 million), the US Dollar (+€5.9 million), the Chinese renminbi (-€4.0 million) and the Moroccan dirham (€4.7 million).

Concession intangible assets break down by operating segment as follows:

NOTE 10 PROVISIONS (extract)

Pursuant to IAS 37, Provisions, Contingent Liabilities and Contingent Assets, a provision is recorded when, at the year end, the Group has a current legal or implicit obligation to a third party as a result of a past event, it is probable that an outflow of resources embodying economic benefits will be required to settle the obligation and the amount of the obligation can be reliably estimated.

Provisions cover all losses that are considered probable, and that relate to litigation (taxation, employee or other) arising in the normal course of Veolia’s business operations.

As part of its obligations under public services contracts, Veolia generally has contractual obligations for the maintenance and repair of the installations it manages. The resulting maintenance and repair costs are analyzed in accordance with IAS 37 on provisions and, where necessary, a provision for contractual commitments is recorded where there are delays in work to be performed.

In the event of a restructuring, an obligation exists if, prior to the period end, the restructuring has been announced and a detailed plan produced or implementation has commenced. Future operating costs are not provided.

In the case of provisions for rehabilitation of landfill facilities, Veolia accounts for the obligation to restore a site as waste is deposited, recording a non-current asset component and taking into account inflation and the date on which expenses will be incurred (discounting). The asset is amortized based on its depletion.

Provisions for closure and post-closure costs encompass the legal and contractual obligations of the Group on the completion of operating activities at a site (primarily site rehabilitation provisions) and, more generally, expenditure associated with environmental protection as defined in the ethics charter of each entity (provision for environmental risks).

Provisions giving rise to an outflow after more than one year are discounted if the impact is material. Discount rates reflect current assessments of the time value of money and the risks specific to the liability. The unwinding of the discount is recorded in the Consolidated Income Statement in “Other financial income and expenses”.