Auckland International Airport Limited – Annual report – 30 June 2025

Industry: transport

2. Summary of material accounting policies (extract)

(a) Basis of preparation (extract)

Measurement base

The financial statements have been prepared on a historical cost basis, except for investment properties, land, buildings and services, runway, taxiways and aprons, infrastructural assets and derivative financial instruments, which have been measured at fair value.

When the group applies fair value hedges to borrowings, the carrying value of the borrowings are adjusted for fair value changes attributable to the risk being hedged.

(g) Property, plant and equipment

Properties held for airport operations purposes are classified as property, plant and equipment.

Property, plant and equipment are initially recognised at cost.

Vehicles, plant and equipment are carried at cost less accumulated depreciation and impairment losses.

Land, buildings and services, runway, taxiways and aprons and infrastructural assets are carried at fair value, as determined by an independent registered valuer, less accumulated depreciation and any impairment losses recognised after the date of any revaluation. Land, buildings and services, runway, taxiways and aprons and infrastructural assets acquired or constructed after the date of the latest revaluation are carried at cost, which approximates fair value. Revaluations are carried out with sufficient regularity to ensure the carrying amount does not differ materially from fair value at the balance date.

Revaluations

Revaluation increases are recognised in other comprehensive income and accumulated as a separate component of equity in the property, plant and equipment revaluation reserve, except to the extent they reverse a revaluation decrease of the same asset previously recognised in the income statement, in which case the increase is recognised in the income statement.

Revaluation decreases are recognised in the income statement, except to the extent they offset a previous revaluation increase for the same asset, in which case the decrease is recognised in other comprehensive income and accumulated as a separate component of equity in the property, plant and equipment revaluation reserve.

Accumulated depreciation as at the revaluation date is eliminated against the gross carrying amounts of the assets and the net amounts are restated to the revalued amounts of the assets.

Revaluation surpluses are transferred from the property, plant and equipment revaluation reserve to retained earnings on derecognition of the asset or if the asset is transferred to investment properties.

Depreciation

Depreciation is calculated on a straight-line basis to allocate the cost or revalued amount of an asset, less any residual value, over its estimated useful life.

The estimated useful lives of property, plant and equipment are as follows:

Land (including reclaimed land) Indefinite

Buildings and services 5 – 50 years

Infrastructural assets 5 – 80 years

Runway, taxiways and aprons 12 – 40 years

Vehicles, plant and equipment 3 – 10 years

Leased assets

Space within the terminals and certain properties used for aeronautical purposes, where the group acts as a lessor, are leased to tenants under operating leases with rentals payable monthly. Lease payments for some contracts include CPI increases, sales-based concession fees and adjustments to rentals depending on the passenger numbers.

To manage credit risk exposure where considered necessary, the group may obtain bank guarantees for the term of the lease.

Although the group is exposed to changes in the residual value at the end of the current leases, the group typically enters into new operating leases and therefore will not immediately realise any reduction in residual value at the end of these leases. Expectations about the future residual values are reflected in the fair value of the properties.

3. Significant accounting judgements, estimates and assumptions (extract)

(b) Carrying value of property, plant and equipment

Judgement is required to determine whether the fair value of land, buildings and services, runway, taxiways and aprons and infrastructural assets has changed materially from the last independent revaluation. The determination of fair value at the time of the revaluation requires estimates and assumptions based on market conditions at that time. Changes to estimates, assumptions or market conditions subsequent to a revaluation will result in changes to the fair value of property, plant and equipment.

Remaining useful lives and residual values are estimated based on management’s judgement, previous experience and supported by registered valuers. Changes in those estimates affect the carrying value and the depreciation expense in the income statement.

The carrying value of property, plant and equipment and the valuation methodologies and assumptions are disclosed in note 11(a) and note 11(c) respectively.

c) Movements in the carrying value of property, plant and equipment

When revaluations are carried out by independent valuers, the valuer determines a value for individual assets. This may involve allocations to individual assets from projects and allocations to individual assets within a class of assets. The allocations to individual assets may be different to the allocations performed at the time a project was completed or different to the allocations to the individual asset made at the previous asset revaluation. These differences at an asset level may be material and can impact the income statement.

(e) Flood-related insurance matters

On 27 January 2023, Auckland experienced widespread flash flooding caused by record-breaking rainfall. Auckland Airport experienced flooding across the precinct and particularly the international terminal building. Both the domestic and international terminals were closed for short periods starting that evening, with domestic flights resuming at midday on 28 January 2023 and international flights from the morning of 29 January 2023.

Material damage

Auckland Airport suffered flood damage to assets across its precinct. The most significant areas of damage were to check-in, baggage and vertical transportation at the international terminal building. Auckland Airport has material damage, business interruption and construction works insurance policies in place.

The group engaged independent experts to estimate the likely extent of damage and to support the insurance claim process.

Asset impairment and write-off

The repair and replacement of damaged assets is almost complete, save for a critical escalator in the arrivals hall, which is planned to be completed during the 2025 calendar year. Repairs completed during the year ended 30 June 2025 have been recognised as an expense during the period. Assets that have been replaced during the period have been treated as a disposal with the cost of replacement recognised as capital expenditure.

The group has assessed that the building and service class is no longer impaired and no further adjustments were required during the year ended 30 June 2025.

In the prior year ended 30 June 2024, earlier impairments of $21.3 million were reversed, of which $21.0 million was reversed in the property, plant and equipment revaluation reserve through other comprehensive income, and $0.3 million was reversed through the income statement.

Other insurance

In addition to recovery of reconstruction costs, Auckland Airport is able to seek recovery of additional items, including the following:

- Business interruption costs and loss of revenue while the Auckland Airport precinct was closed or affected by the flood;

- Costs of professional advisors assisting the company as a result of the flood; and

- Additional ongoing operating costs as a result of the damage.

The additional expenses were recognised when incurred and any recovery of these items is recognised when recovery is virtually certain.

Insurance recovery income

The group recognises the expected insurance proceeds when they can be reliably estimated and the recovery is virtually certain. The insurers have acknowledged the flood event damage and made progress payments since the January 2023 event. However, agreement on the full costs of remediation is incomplete.

During the year ended 30 June 2025, the insurers agreed to a fourth progress payment of $4.0 million, which the group has recognised as income. In total, the group has recognised $28.0 million as income since the January 2023 event.

The flood-related amounts recognised during the year ended 30 June 2025 in the consolidated income statement and the consolidated statement of comprehensive income are shown in the table below:

1 During the financial year ending 30 June 2024 the group reversed fixed asset impairments of $0.3 million that were previously recognised in flood- related expenses.

2 During the financial year ending 30 June 2024 the group reversed $21.0 million of flood-related fixed asset impairments that were previously recognised through other comprehensive income in the property, plant and equipment revaluation reserve.

(f) Climate change

Judgement is required to determine the extent to which climate change may impact the amounts recognised in these financial statements.

The group has taken climate change into account during the preparation of these financial statements, considering the climate change risk and ensuring consistency between the potential future scenarios outlined within the Climate-Related Disclosure and the assumptions and estimates applied. In particular, the group has considered:

- Useful lives for existing assets that will be replaced as the group transitions to reduce its carbon emissions, in line with the decarbonisation pathway and infrastructure planning that supports future low-emissions technologies;

- Risk of damage to existing assets and operational impacts associated with changing weather patterns and sea level rise, including the expected time frames that existing assets would be affected, informed by physical risk modelling and long-term stormwater strategies;

- Potential changes in customer demand and regulation that may affect the future economic benefits assumed in the carrying value of assets, reflecting transition risks such as evolving policy, stakeholder expectations, and the pace of aviation sector decarbonisation

The independent valuations of property, plant and equipment, and investment property have taken into account the potential impact of climate change in determining their fair value.

The Group continues to mitigate near-term risks associated with extreme weather events through targeted investment in stormwater infrastructure, enhancing the resilience of critical assets against flooding. Auckland Airport is gradually transitioning its precinct infrastructure to electric systems, including food and beverage facilities, and heating, ventilation and air conditioning (HVAC).

Further information on climate-related risks, opportunities, and the Group’s transition planning is available in the Climate-Related Disclosure section of the Annual Report.

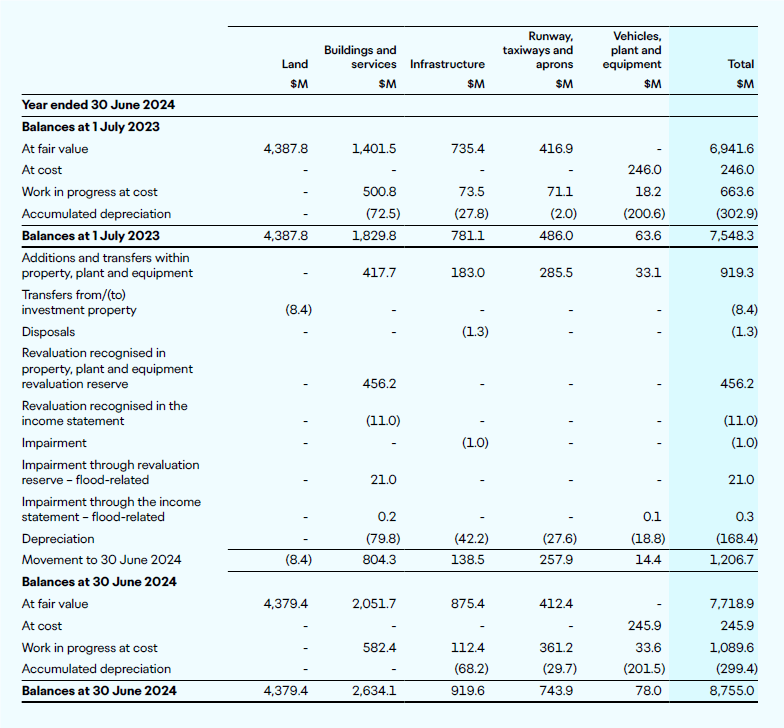

11. Property, plant and equipment

(a) Reconciliation of carrying amounts at the beginning and end of the year

Additions for the year ended 30 June 2025 include capitalised interest of $60.9 million (2024: $45.0 million).

During the year, estimated useful lives were revised for car park facilities and surrounding infrastructure scheduled for redevelopment to accommodate the construction of new regional stands at the domestic terminal. This change in estimate resulted in an increase in depreciation expense of $7.0 million for the year ended 30 June 2025 and an expected additional depreciation of approximately $5.7 million annually over the remaining useful life of these assets.

The group includes leased properties within property, plant and equipment when the properties are held for the purpose of airport operations.

The following categories of property, plant and equipment are leased to tenants:

- Aeronautical land, including land associated with aircraft, freight and terminal use carried at $355.9 million (30 June 2024: $339.7 million);

- Land associated with retail facilities within terminal buildings carried at $1,795.9 million (30 June 2024: $1,664.5 million); and

- Terminal building premises (within buildings and services), being 15% of total floor area and carried at $369.0 million (30 June 2024: 15% of total floor area or $311.7 million).

(b) Carrying amounts measured at historical cost less accumulated depreciation

(c) Revaluation of land, buildings and services, infrastructure, runway, taxiways and aprons

At the end of each reporting period, the group makes an assessment of whether the carrying amounts differ materially from fair value and whether a revaluation is required. The assessment considers movements in the capital goods price index since the previous valuation, mid-year desktop reviews by the previous valuers, and changes in valuations of investment property as an indicator of property, plant and equipment valuation movement.

Valuations are completed in accordance with the company’s asset valuation handbook, which is prepared in accordance with financial reporting and valuation standards. Management reviews the key inputs, assesses valuation movements and holds discussions with the valuers as part of the process. Discussions about the valuation processes and results are held between the group’s management and the Board.

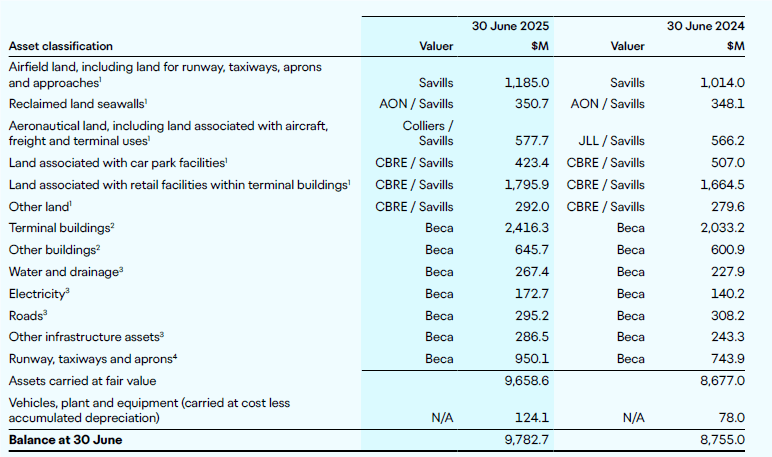

Land assets were independently valued by Savills Limited (Savills), Colliers International (Colliers), CB Richard Ellis Limited (CBRE) and Aon Risk Solutions (AON) as at 30 June 2025.

Buildings and services, infrastructure and runway, taxiways and aprons were not revalued at 30 June 2025. The assessment is that there is not a material difference between the carrying value and the fair value of those asset classes at 30 June 2025.

The valuation approach for buildings and services, infrastructure and runway assets is the optimised depreciated replacement cost method. The assessment of fair value was supported by an independent review of potential changes in the replacement cost for those assets as at 30 June 2025. The independent review considered movements in relevant capital goods price index subcategories.

Building and services assets were independently valued by Beca Projects NZ Limited (Beca) at 30 June 2024.

Infrastructure and Runway, taxiways and aprons assets were independently revalued by Beca as at 30 June 2023.

Impairment and write-offs – flood damage

In the prior year ended 30 June 2024 the group reversed impairments related to the January 2023 flood event. The repair and replacement of damaged assets is almost complete, save for a critical escalator in the arrivals hall, which is planned to be completed during the 2025 calendar year. The group assessed that no further flood-related impairments were required during the year ended 30 June 2025.

Further details are provided in note 3e.

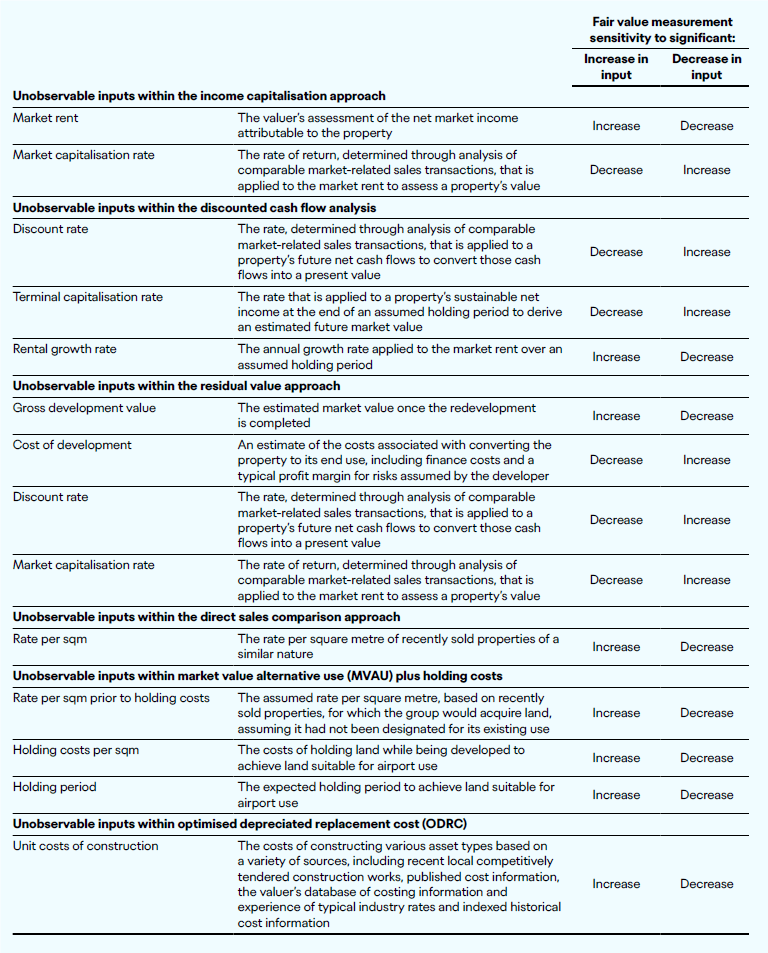

Fair value measurement

The valuers use different approaches for valuing different asset groups. Where the fair value of an asset is able to be determined by reference to market-based evidence, such as sales of comparable assets, the fair value is determined using this information. Where fair value of the asset is not able to be reliably determined using market-based evidence, discounted cash flows or optimised depreciated replacement cost is used to determine fair value. Assets acquired or constructed after the date of the latest revaluation are carried at cost, which approximates fair value.

The group’s land, buildings and services, infrastructure, runway, taxiways and aprons are all categorised as Level 3 in the fair value hierarchy as described in note 2(e). During the year, there were no transfers between the levels of the fair value hierarchy.

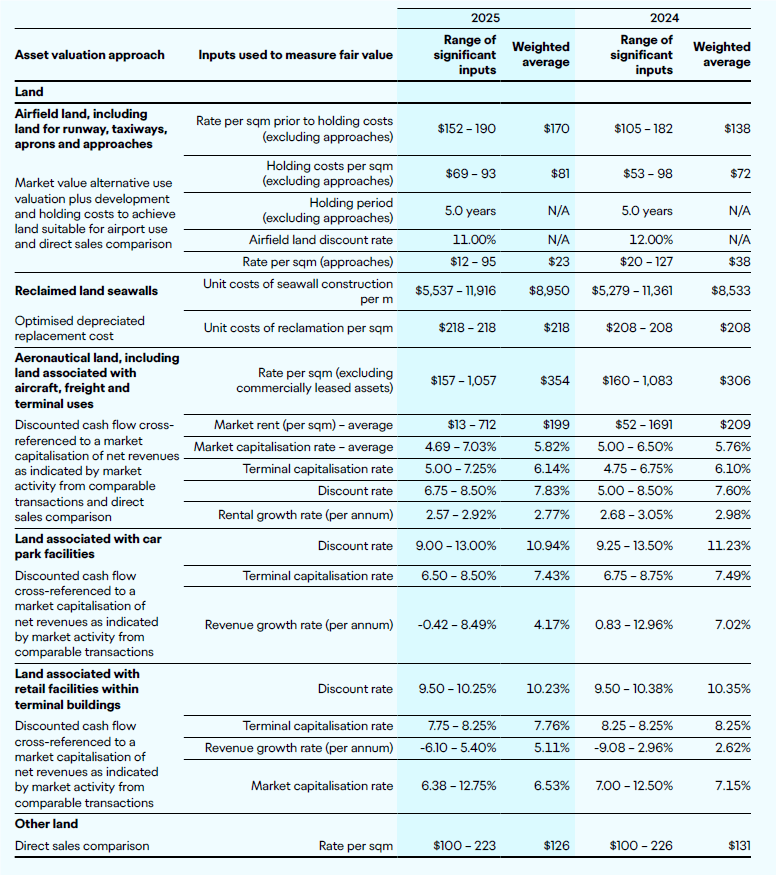

The table below summarises the valuation approach and the principal assumptions used in establishing the fair values:

The valuation inputs for land are from the 2025 valuation, while the prior year’s comparatives are from the 2023 valuation of these assets. The valuation inputs for buildings and services are unchanged from the 2024 valuation. The valuation inputs for infrastructure and runways, taxiways and aprons are unchanged from the 2023 valuation. These asset classes were not revalued in 2025 because the carrying value was not assessed to be materially different from fair value.

The table below includes descriptions of different valuation approaches:

The table below summarises each registered valuer’s valuation of property, plant and equipment:

1 Land assets were revalued at 30 June 2025. This class was last revalued at 30 June 2023.

2 At 30 June 2025, the assessment is there is no material change in the fair value of buildings and services assets compared with carrying values. This class was last revalued at 30 June 2024.

3 At 30 June 2025, the assessment is there is no material change in the fair value of infrastructure assets compared with carrying values. This class was last revalued at 30 June 2023.

4 At 30 June 2025, the assessment is there is no material change in the fair value of runways, taxiways and apron assets compared with carrying values. This class was last revalued at 30 June 2023.

The following table shows the impact on the fair value due to a change in a significant unobservable input: