Roche Holding Ltd – Annual report – 31 December 2025

Industry: pharmaceuticals

28. Leases (extract)

The Group as a lessor

In the Diagnostics Division the Group enters into certain contracts which include placement of diagnostics instruments, supply of reagents and other consumables, and servicing arrangements. Depending upon the term of the agreement, the instrument placement may result in either a finance lease or an operating lease. The Group performs a thorough customer assessment before new leasing agreements are signed. Usually the Group also retains rights to terminate or modify contracts if certain conditions are not met.

Finance leases. Certain assets, mainly diagnostics instruments, are leased to third parties through finance lease arrangements. Such assets are reported as receivables at an amount equal to the net investment in the lease. Income from finance leases is recognised as sales at amounts that represent the fair value of the instrument, which approximates the present value of the minimum lease payments under the arrangement. Finance income for finance lease arrangements longer than twelve months is deferred and subsequently recognised based on a pattern that approximates the use of the effective interest method and recorded in other revenue for diagnostics instruments.

The following amounts were recorded as income in respect of finance leases.

Finance leases: selected items of income in millions of CHF

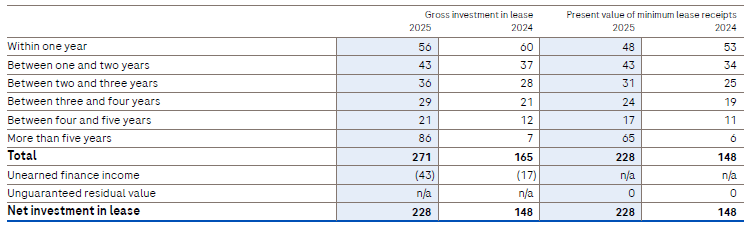

Currently the Group does not have any income from the variable lease payments of finance leases. The carrying amount of the net investment in finance leases reported as receivables was CHF 228 million (2024: CHF 148 million).

Finance leases: future minimum lease receipts under non-cancellable leases in millions of CHF

Operating leases. Certain assets, mainly diagnostics instruments, are leased to third parties through operating lease arrangements. Income from operating leases is recognised as sales on a straight-line basis over the lease term or, when lease revenue is entirely based on variable lease payments and subject to subsequent reagent sales, as the performance obligations for reagents are satisfied.

Lease income in 2025 was CHF 785 million (2024: CHF 792 million) and was included in sales. Of this CHF 622 million (2024: CHF 545 million) relates to variable lease payments not depending upon an index or rate.

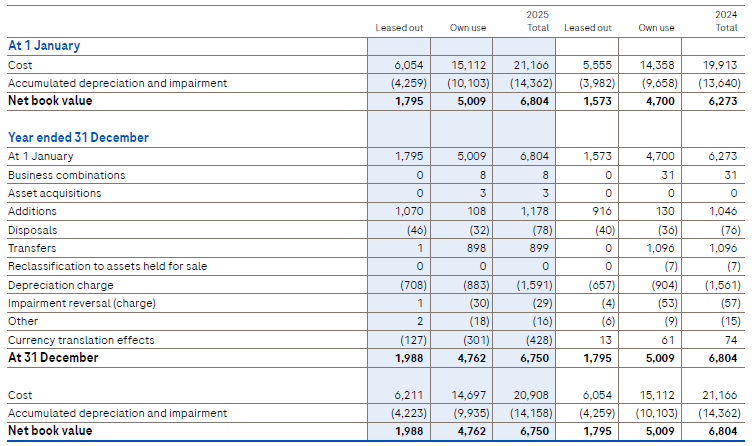

Leased out assets are reported within property, plant and equipment, as shown in the table below.

Machinery and equipment subject to operating leases: movements in carrying value of assets in millions of CHF

The undiscounted amounts expected to be received from non-cancellable operating leases are shown in the table below.

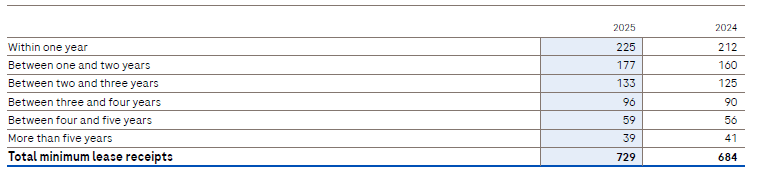

Operating leases: future minimum lease receipts under non-cancellable leases in millions of CHF