Santos Limited – Half year report – 30 June 2017

Industry: oil and gas

3.4 IMPAIRMENT OF NON-CURRENT ASSETS

The carrying amounts of the Group’s oil and gas assets are reviewed at each reporting date to determine whether there is any indication of impairment. Where an indicator of impairment exists, a formal estimate of the recoverable amount is made.

The expected future cash flow estimation is based on a number of factors, variables and assumptions, the most important of which are estimates of reserves, future production profiles, third party supply, commodity prices, costs and foreign exchange rates. In most cases, the present value of future cash flows is most sensitive to estimates of future oil price, discount rates and production.

Estimates of future commodity prices have been updated from the previous reporting date.

Future prices (US$/bbl) used were:

The future estimated foreign exchange rate applied is A$/US$0.70 in 2017, and A$/US$0.75 in all subsequent years.

The discount rates applied to the future forecast cash flows are based on the Group’s weighted average cost of capital, adjusted for risks where appropriate. The range of pre-tax discount rates that have been applied to noncurrent assets is between 10.3% and 16.2%.

In the event that future circumstances vary from these assumptions, the recoverable amount of the Group’s oil and gas assets could change materially and result in impairment losses or the reversal of previous impairment losses.

Due to the interrelated nature of the assumptions, movements in any one variable can have an indirect impact on others and individual variables rarely change in isolation. Additionally, management can be expected to respond to some movements, to mitigate downsides and take advantage of upsides, as circumstances allow. Consequently, it is impracticable to estimate the indirect impact that a change in one assumption has on other variables and hence, on the likelihood, or extent, of impairments or reversals of impairments under different sets of assumptions in subsequent reporting periods.

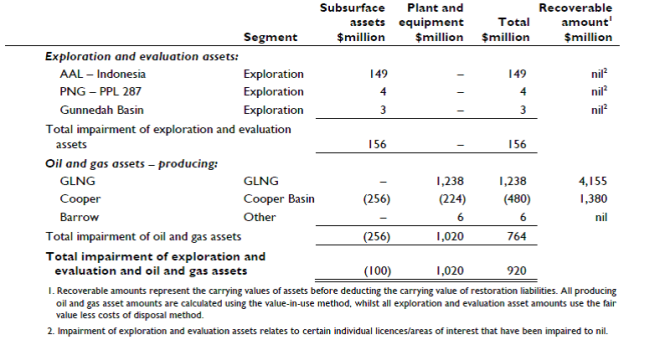

Recoverable amounts and resulting impairment write-downs/(reversals) recognised for the half year ended 30 June 2017 are:

Exploration and evaluation assets

The impairment of AAL has arisen mainly from the impact of lower oil prices.

Oil and gas assets

GLNG

Since the last carrying value assessment at 31 December 2016 there have been a number of changes to relevant assumptions, principally lower US$ oil prices, that have impacted the recoverable amount. Additionally, the Australian government has introduced regulations relating to the Australian Domestic Gas Security Mechanism since 31 December 2016. The impact on recoverable amount of the lower oil price assumption, combined with a higher discount rate and lower assumed volumes of third party gas, has been partially offset by higher assumed equity gas volumes resulting from positive upstream performance and lower costs.

Cooper Basin

Whilst the Cooper Basin has been impacted by lower US$ oil price assumptions, this has been more than offset by lower forecast development costs combined with increased drilling activity and production, resulting in a reversal of impairment.

Sensitivity

To the extent the oil and gas cash generating units have been written down to their respective recoverable amounts in the current and prior years, any change in key assumptions on which the valuations are based would further impact asset carrying values. When modelled in isolation, it is estimated that changes in the key assumptions would result in the following additional impairment/lower impairment reversal: