British American Tobacco p.l.c. – Annual report – 31 December 2025

Industry: tobacco

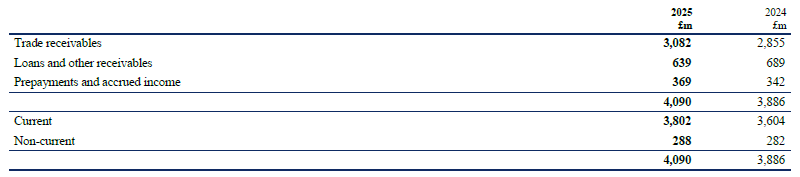

17 Trade and other receivables (extract)

Trade receivables

The majority of receivables are held in order to collect contractual cash flows, in accordance with the Group’s business model for managing financial assets, and hence are measured at amortised cost. In certain countries, however, the Group has entered into factoring arrangements and periodically sells certain trade receivables to banks and other financial institutions, without recourse, for cash. These trade receivables have been derecognised from the balance sheet to reflect the transfer by the Group of substantially all of the risks and rewards of the receivables, including credit risk. Consequently, the cash inflows have been recognised within operating cash flows. Typically in these arrangements, the Group also acts as a collection agent for the bank. At 31 December 2025, the value of trade receivables derecognised through the factoring arrangements where the Group acts as a collection agent was £629 million (2024: £535 million) and where the Group does not act as a collection agent was £14 million (2024: £7 million). Included in trade receivables above is £76 million (2024: £213 million) of trade debtor balances which were available for factoring under these arrangements. In addition, the Group participates in certain supply chain finance programmes utilised by its customers allowing the Group to receive payment for invoices earlier than the agreed due date at a discounted value. At 31 December 2025, the value of trade receivables derecognised through these arrangements was £226 million (2024: £172 million).

A number of Group companies have entered into arrangements with certain customers. Under these agreements the Group enters into an agreement with a financial institution and/or a customer. The agreement allows the customer to obtain finance from the financial institution in order to pay invoices due to the Group. The customer repays the financial institution based on an agreed maturity date independently agreed between the customer and financial institution. Under these agreements there is normally no recourse to the Group in the event of credit default by customers. However, the Group is subject to various performance obligations under the arrangement including notifying the financial institution of credit default or of changes to, or termination of, the customer supply agreement. The amount derecognised from trade receivables at 31 December 2025 in relation to these arrangements is £10 million (2024: £20 million). The cash flows have been recognised within operating cash flows.

The Group also participates in agreements with customers where the Group can request early payment of invoices at a discount. The discount is recognised as a deduction against revenue. At 31 December, £13 million was received in advance of the invoice due date (2024: £82 million).

26 Financial instruments and risk management (extract)

Liquidity risk (extract)

As part of its working capital management, in certain countries, the Group has entered into factoring arrangements and supply chain financing arrangements. These are explained in further detail in note 17 and note 25.