International Consolidated Airlines Group, S.A. – Annual report – 31 December 2019

Industry: airline

33 Changes to accounting policies

Change in accounting policy

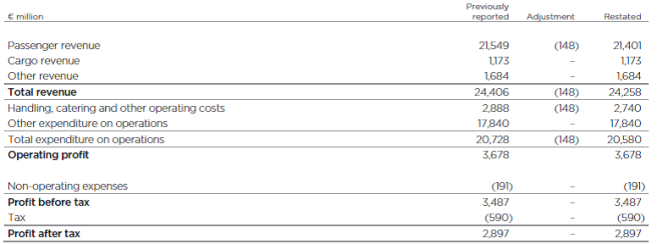

In September 2019, the IFRS Interpretations Committee clarified that under IFRS 15 compensation payments for flight delays and cancellations form compensation for passenger losses and accordingly should be recognised as variable compensation and deducted from revenue. This clarification had led the Group to change its accounting policy, which previously classified this compensation as an operating expense. Accordingly, the Group has restated the comparative period for 2018 to reflect €148 million of compensation costs as a deduction from Passenger revenue and a corresponding reduction within Handling, catering and other operating costs. The following table summarises the impact of the change in accounting policy on the Income statement for the year to December 31, 2018:

Consolidated income statement (extract for the year to December 31, 2018)

There is no impact on profit after tax in the Consolidated Income Statement for 2018, the Consolidated Balance Sheet as at January 1, 2018 or December 31, 2018 or the Consolidated Statement of Changes in Equity as at January 1, 2018 or December 31, 2018.